Monday Jun 15, 2026

Monday Jun 15, 2026

Thursday, 1 June 2017 00:00 - - {{hitsCtrl.values.hits}}

Colombo Stock Exchange Manager Compliance Lankesha Molligoda, Colombo Stock Exchange CEO Rajeeva Bandaranaike, Ernst & Young Former Head Asite Talwatte, Securities and Exchange Commission former Chairman Dr. Dayanath Jayasuriya, Acuity Stockbrokers Executive Director and Deputy Chairman Deva Ellepola and Securities and Exchange Commission Former Director General Malik Cader

Former Chairman and Director General Dr. Dayanath Jayasuriya last week called for a revisiting of the proposed amendments to both the Securities and Exchange Commission (SEC) Act and the listing rules of the Colombo Stock Exchange (CSE).

A host of concerns on the proposed amendments were highlighted by Dr. Jayasuriya, who one time served separately as SEC Chairman and Director General, at the seminar organised by Asian Pathfinder Legal Consultancy Services.

Dr. Jayasuriya was also former Chairman, President’s Committee of the International Organisation of Securities Commission (IOSCO) and Insurance Board of Sri Lanka.

Having made a thorough critique on changes to listing rules, Dr. Jayasuriya said: “CSE proposals need to be seriously reconsidered.”

He queried whether the Sri Lankan capital market was overregulated or under-regulated and whether the market was not performing well due to CSE rules or SEC rules or implementation issues with one or both. He also inquired whether the macro economic climate was not in congruence with the risk appetite for market development.

“Will not piecemeal reforms to CSE rules, such as those proposed now, be counterproductive and seriously erode market confidence resulting in more de-listings or in reluctance to list?” he posed at the seminar. The seminar extensively dealt with pros and cons of the proposed Watch List as against the existing Default Board.

Dr. Jayasuriya also questioned whether the proposed amendments to SEC Act were market friendly or not and whether they provided for a strong, robust and independent Secretariat and Commission.

A change proposed in the office of Director General of the SEC is that one of the grounds for the removal of the DG is “the likelihood of any conflict between the interests of the Commission and the DG”.

This is against the current provision that the Director-General shall, subject to the general direction and control of the Commission, be charged with the direction of the affairs and transactions of the Commission, the exercise, discharge and performance of its powers, functions and duties, and the administration and control of the employees of the Commission.

He said this change is not desirable since there could always be differences of opinion between the Commissioners and the Director-General. If this amendment goes through no one will want to be the DG of SEC, claimed Dr. Jayasuriya.

Dr. Jayasuriya said many progressive capital market regulators were revisiting regulatory requirements to provide for a disclosure-based market friendly regime moving away from a strict rule-based regime.

According to him, the New Zealand Stock Exchange 2017 CG code states as follows:

The NZX Code is structured around eight principles:

Code of ethical behaviour – directors should set high standards of ethical behaviour, model this behaviour and hold management accountable for these standards being followed throughout the organisation.

Board composition and performance – to ensure an effective board, there should be a balance of independence, skills, knowledge, experience and perspectives.

Board committees – the Board should use committees where this will enhance its effectiveness in key areas, while still retaining board responsibility.

Reporting and disclosure – the Board should demand integrity in financial and non-financial reporting and in the timeliness and balance of corporate disclosures.

Remuneration – the remuneration of directors and executives should be transparent, fair and reasonable.

Risk management – directors should have a sound understanding of the material risks faced by the issuer and how to manage them. The Board should regularly verify that the issuer has appropriate processes that identify and manage potential and material risks.

Auditors – the Board should ensure the quality and independence of the external audit process.

Shareholder rights and relations – the Board should respect the rights of shareholders and foster relationships with shareholders that encourage them to engage with the issuer

The NZX Code outlines recommendations under each principle recommending areas of good practice.

If a particular recommendation is not appropriate for an issuer given its size or stage of development, the issuer can explain why it has chosen not to adopt the recommendation and the alternative measures it has in place.

The NZX Code therefore seeks to balance a desire to promote strong corporate governance while remaining flexible so that boards and issuers can determine the appropriate corporate governance practices for their businesses.

Issuers should be continuously reviewing their corporate governance practices and seeking to improve these over time. NZX encourages issuers to think about disclosure on a continuous basis and not simply as an annual event.

The recommendations have been drafted with the intention of allowing flexibility between disclosure in an Annual Report or on an issuer’s website. NZX also notes the value of independence on boards.

Former SEC Director General Malik Cader said new SEC Act is a “brilliant piece of legislation” from an academic point of view but questioned whether the Sri Lanka’s capital market, currently with a market capitalisation of $ 20 billion, is ready for it. He noted that regulators need to take cognizance of the fact that Sri Lanka’s capital market is still evolving and said that IOSCO does recognise two categories of markets - developed and developing and Sri Lanka falls on to the latter.

“We need to “mother the market” than “father the market”,” he said adding “Sri Lanka must ensure capital markets grow before bringing “Rolls-Royce” regulation. “ In that context he opined disclosure based regulatory regime is better.

With regard to amendments on the office of DG, Cader said at present SEC Commissioners are Non-Executive and DG is executive and the proposed change may dilute this position.

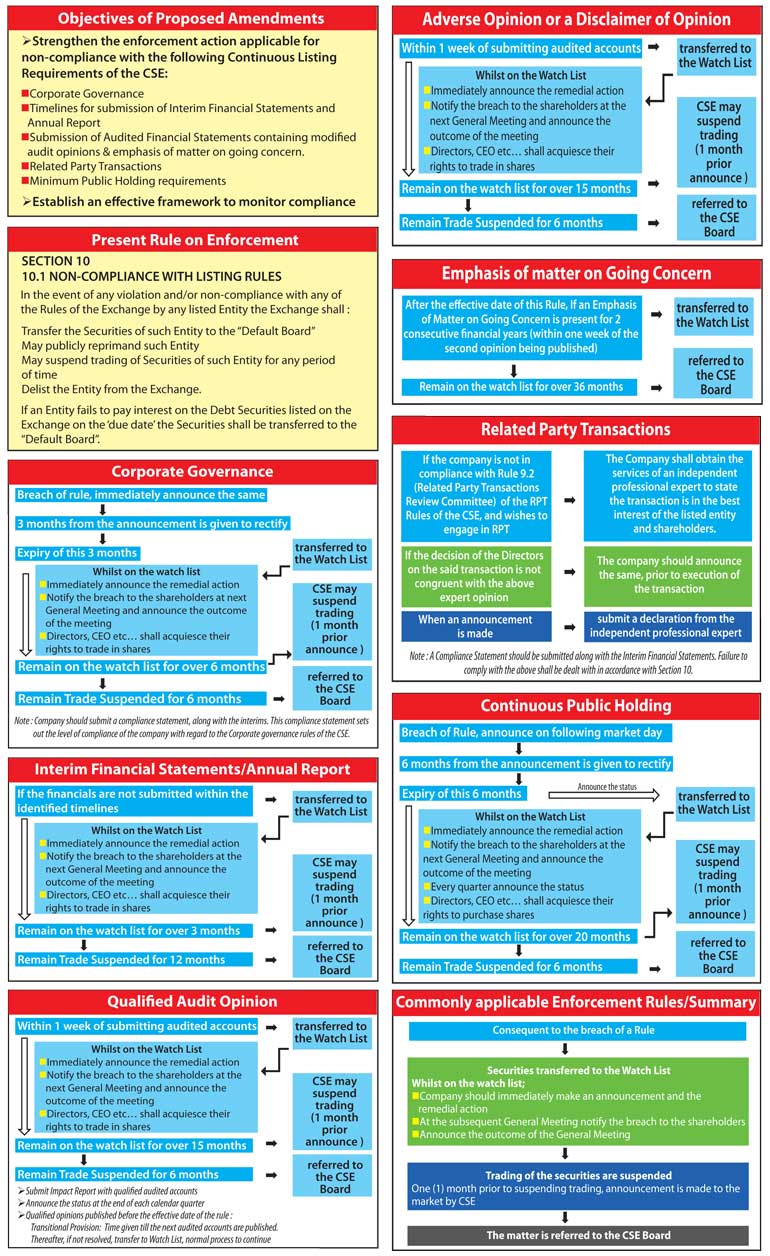

10 major changes

In his presentation, Dr. Jayasuriya focused on 10 major changes proposed by the CSE and the SEC.

Explaining the rational for the major change – moving away from Default Board to Watch List, he said the public might think an entity on the Default Board is actually in default of payment. He also quoted the NASADQ Definition: A list of securities selected for special surveillance by a brokerage, exchange, or regulatory organisation; firms on the list are often takeover targets, companies planning to issue new securities, or stocks showing unusual activity

The proposed Rule 10.2.1 in listing rules provides for the CSE to inform entity of the non-compliance and the transfer. “However there is no right of appeal/representation prior to transfer provided,” cautioned Dr. Jayasuriya adding that determinations of board of exchange are final and binding on listed entity.

Changes have also been proposed in terms of corporate governance disclosures in the new listing rules by way of Additional rules 7.10.7 and 7.10.8. The current Rules (7.10.1; 7.10.2(a); 7.10.5(a) & 7.10.6(a)

Specify composition of non-executive directors on the board; independent directors; remuneration committee; and audit committee.

Proposed Rule 7.10.7 states that at the time of submission of interim financial statements submit compliance statement on level of compliance-format is in appendix 7c and to be signed by two directors

Appendix 7c covers related party transaction review committee as well.

Commenting on the proposed rule 7.10.7, Dr. Jayasuriya said if Related Party Transaction Committee (RPTC) is to be included in appendix 7c, the new rule must specifically mention section 9 of the listing rules dealing with related party transaction. The total number of non-ex directors on the board is calculated on the number as at the conclusion of the immediately preceding AGM (Rule 7.10.1)- hence at the time of filing interim financial statements the ratio may be different to the prescribed formula.

“Is the difference to be regarded as being in ‘compliance’ or ‘not in compliance’?” queried Dr. Jayasuriya.

In terms of Proposed rule 7.10.8-b, he asked what happens if not rectified within three months. It appears that the CSE will automatically transfer the securities to the Watch List.

Highlighting a bizarre consequence, Dr. Jayasuriya said the Directors and the Chief Executive Officer of the Entity, their Close Family Members and any entity, other than Listed Entities, in which a Director, the Chief Executive Officer or their Close Family Members hold fifty per centum (50%) or more of the voting rights shall Acquiesce their rights to transact, directly or indirectly, in the Securities of the Entity whilst such Securities are on the Watch List, unless prior approval is obtained from the SEC.

“No Guidelines as to situations where SEC will grant prior approval,” he added.

What does “Acquiesce” mean? To accept something without arguing, even if you do not really agree with it. Property rights? According to Black’s Law Dictionary: Acquiesce is to accept tacitly or passively; to give implied consent to (an act). For example “in the event all the partners acquiesced in the settlement”.

He said the CSE must clarify the distinction between Acquiesce and Shall Not Transact.

Then is the issue of who are close family members. It is stated that ‘Close Family Member’ shall mean and include the spouse and a child below eighteen (18) years and any of the following persons provided that they are financially dependent and/or acting in concert:

A) child above 18 years;

B) Grandparents;

C) Parents;

D) Brothers;

E) Sisters;

F) Grandchildren; and

G) Spouse of the persons referred to above

‘Acting in Concert’ shall have the same meaning as defined in the Takeovers and Mergers Code.

Commenting on the transfer of securities to Watch List, he said announcement to the market on remedial action taken or proposed must be made. Any deviation to be notified within one market day after Board approval. If after six months there is failure to complete remedial action the trading of such securities of the listed entity may be suspended by the CSE. If trading suspension continues beyond 6 months what is the non-compliance which leads to all these serious actions queried Dr. Jayasuriya. He also said it is only about the composition of board, Audit Committee, Remuneration Committee, RPTC and the definition about independent directors. It is only a matter of the ratio of representation.

Case study

At the seminar, Dr. Jayasuriya presented the following case study:

John is an independent non-exec. Director of XYZ Company and one of the two non-exec. Members of the Remuneration Committee (RC) which has only one additional member. The company declared a profit of Rs. 650 after tax.

John resigned from RC which meets only twice a year.

Chairman says no hurry to fill vacancy as RC will not meet for another five months.

Both Company Secretary and Compliance Officer disagree.

If vacancy on RC is not filled immediately, an immediate announcement must be made to the market via exchange. If after three months vacancy still remains XYZ Company will be on ‘Watch List’.

Directors’ appointments and/or resignations – notifying market is fine but need RC vacancy also to be similarly announced?

Panic selling can lead to systemic risk.

Focusing on the changes proposed to submission of interim financial statement and Annual Report, Dr. Jayasuriya said consequences are that if not submitted within time-limit, securities will be transferred to ‘Watch List’. On failure to take remedial measures trading will be suspended. Furthermore directors, CEO, close family members, etc., must acquiesce their rights.

In terms of modified audit opinion and emphasis of matter on going concern, he said new areas not covered at present include qualified audit opinion in the independent auditor’s report; Listed entity must give to CSE for public release an “impact report” as part of the statement of directors’ responsibility in the audited financial statement/annual report of the entity.

The Impact Report shall at a minimum contain cumulative impact on profit or loss, net assets, total assets, turnover/total income, earnings per share and any other financial item(s) which may be impacted due to qualified audit opinion.

The Securities of the Listed Entity shall be transferred to the Watch List. Such transfer shall be made on or before the expiry of one week from the date of receipt of the Audited Financial Statements of the Entity by the Exchange.

Where the Listed Entity is a parent entity, the Audit Opinion referred to in this Rule shall include the Audit Opinion on the financial statements of the Group and the Entity.

On submission of the Audited Financial Statements/annual report containing a qualified audit opinion, the Listed Entity must announce to the market remedial action. If after 15 months not remedied trading will be suspended.

Directors, etc. must acquiesce their rights to transact without prior approval of SEC. Subsequently even delisting can take place.

Adverse opinion or a disclaimer of opinion also will lead securities to be moved to ‘Watch List’. Announcement to the market via CSE with remedial action to be mentioned. If not remedied trading will be suspended and directors etc., cannot trade.

On “Emphasis on matter of going concern”, he said comment after two consecutive years will be transferred to ‘watch list’. After 36 months CSE Board to make determination which shall be informed to the SEC. Dr. Jayasuriya said it is unclear whether it relates to identical comment.

On changes to related party transactions, he said if RPTC has not deliberated must obtain the services of an independent professional expert on whether proposed transaction is in the best interest of listed entity and its shareholders, if the decision by the board of directors is not congruent with the independent opinion announcement to the market prior to transaction.

The Listed Entity shall, whether the decision of the Board of Directors of the Entity is congruent with the independent opinion or not, submit to the Exchange at the time of making the announcement to the market, a declaration from the independent professional expert that;

(i) The said party is neither a related party of the Listed Entity as defined in the Sri Lanka Accounting Standards nor has a significant interest in or financial connection to the Listed Entity and/or the Group;

(ii) The said party is a member of good standing of a professional association relevant to the service undertaken and has the necessary skills and resources available at his disposal to arrive at a competent independent opinion; and,

(iii) The party has evaluated all assumptions and made all the inquiries that he believes are desirable and appropriate in order to arrive at a competent independent opinion.

An affidavit is not required and non-compliance treated as a violation Dr. Jayasuriya said and inquired whether the SEC Code of Best Practice on related party transactions of December 2013 had been ignored or considered in developing these changes.

On changes to minimum public holding, he said guidelines needed for provision for waiver.

Dr. Jayasuriya welcomed the definition of non-executive director as per the proposed rules. Non-Executive Director’ shall mean a member of the Board of Directors of an Entity, who is not employed by the Entity and does not, directly or indirectly, engage in the operational and/or managerial functions of the Entity.

The changes on «continuing listing requirements and audited financial statements» are “A Listed Entity shall ensure that the annual report is issued to the Entity’s shareholders and given to the Exchange within a period not exceeding five (05) months from the close of the financial year of the Listed Entity. The Audited Financial Statements shall be prepared in accordance with the Sri Lanka Accounting Standards, audited in accordance with Sri Lanka Auditing Standards and shall comply with any other applicable regulatory requirements.”

Other observations made by Dr. Jayasuriya were:

Watch List: Provided however, the above Rules 10.2.1 to 10.2.4 shall not be applicable in instances where specific enforcement action have been set out in these Rules, including the following;

(a) Rule 7.5 (C) – non-compliance with the rules on modified audit opinions (qualified, adverse or disclaimer of opinions) and emphasis of matter on going concern of a listed entity

B) Rules 7.4 (C) and 7.5 (D) - non-submission of interim financial statements and annual reports (financial statements)

C) Rule 7.10.8 - non-compliance with the rules on corporate governance

D) Rule 7.13.2 - non-compliance with the minimum public holding requirement

Change 10: Suspension

Notwithstanding the procedure set out in Rule 10.2 above, the Exchange may, at any time, suspend the trading of Securities of a Listed Entity, if in the Exchange’s opinion any of the following applies:

(i) The Entity is unable or unwilling to comply with, or violates, a Listing Rule

(ii) The Exchange’s Rules require the suspension

(iii) By operation of law

The SEC may at its sole discretion direct the Exchange to suspend the Securities of any Listed Entity.

Pix by Upul Abayasekara

Colombo Stock Exchange CEO Rajeeva Bandaranaike said amendments to listing rules are still in draft stages with public views sought before finalising.

He said the revision aims to achieve several objectives including good governance. Following is based on Bandaranaike’s presentation.