Tuesday Feb 17, 2026

Tuesday Feb 17, 2026

Tuesday, 11 July 2017 00:13 - - {{hitsCtrl.values.hits}}

In his presentation the Budget Speech for 2016, the Minister of Finance proposed to introduce a New Income Tax Law on the following lines: “Existing tax laws in the country are cumbersome, complex and based on traditional British concepts. The complexity of the tax laws has been identified as an impediment for the effective implementation of tax policy in Sri Lanka. It has led to various complications thereby hampering the effective implementation of the tax policy. Therefore, we need to redraft the tax laws to bring about necessary improvements to the legal framework to ensure clarity, consistency and simplicity towards reflecting the features of modern tax systems which will help taxpayers to understand the system easily and eliminate loopholes that have been created by the ambiguities in laws while strengthening tax administration. For this purpose, we will receive technical assistance from IMF and I propose to complete the project/process by end 2016.”

In keeping in line with the pronouncement, the proposed Inland Revenue Act (“new Bill”) has been published by gazette dated 16 June and was issued on 19 June. According to the new Bill the effective date of the proposed Inland Revenue Act is expected to be for any year of assessment commencing 1 April and will thereby have the effect of repealing the Inland Revenue Act No. 10 of 2006 (as amended). However, as per the Section 203 (2) of the new Bill, the current law (i.e. the Inland Revenue Act No. 10 of 2006 (as amended)) will continue to apply in respect of events occurring prior to the date of commencement of this new Inland Revenue Act.

Upon analysis of the past two decades of Sri Lanka with regard to Income Tax laws, the proposed Act will be the third Inland Revenue Act since the year 2000. However, the new Bill is structurally different to the laws we have been conversant with historically. For instance, the terminology is different and the new law deviates from the previous taxability provisions. The concept of statutory income has been removed.

What does the new

Bill entail?

At a high level, it is clear that the income tax exemptions are limited and the tax rates are streamlined. The key changes as enlisted below.

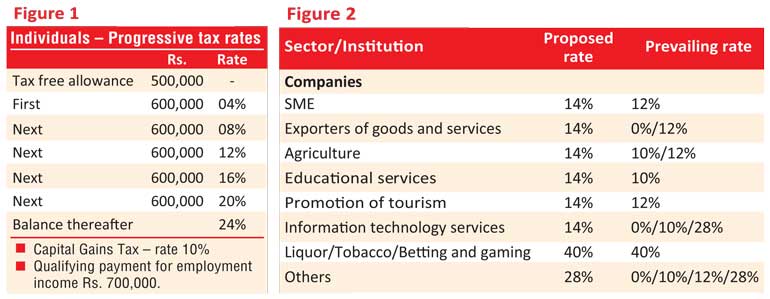

Individuals and non-corporates

Companies

Administration

A key observation is the term “solely” in the context of invoking the 14% concessionary rate, the wording of the law is that it is granted for instance “in the case of a company solely conducting a business of exporting goods and services” and so on. This is a very restrictive concession as the term “solely” appears in all instances where the 14% rate has been afforded (except for SMEs). This will be very challenging to the tax payers when there is any other business income along with the specified business activity. Since sectors such as export, agriculture, educational, promotion of tourism and information technology are key drivers to the economic growth, the policymakers should accommodate some flexibility in order to encourage and develop them.

While the new Bill keeps in line with the policy pronouncement and these changes are done to simplify the tax framework, broadbase the tax network and ease collection in a bid to generate more tax revenue for the growth and betterment of the country. It is worrying that the effective date of this Act is proposed to be 1 April 2017. The Inland Revenue Department in April, issued a notice to taxpayers to continue with the present law until further notice. We are already a quarter into the year of assessment 2017/2018 most of the taxpayers comply with their monthly statutory tax payments such as PAYE and WHT under the Inland Revenue Act No. 10 of 2006. As such, introducing the proposed Act with retrospective effect should not leave room to penalise them such taxpayers subsequently and it must be clarified by the Department of Inland Revenue. In the alternative, the effective date should be a future date allowing taxpayers to work with certainty of tax policies. Also, it would be meritorious if that the Minister of Finance reintroduces the office of Tax Ombudsman as proposed in the budget for the year 2017 as this will enhance the taxpayer’s confidence in exercise of their rights.

(The writer is Director – Tax Services, BDO Partners.)