Saturday Jun 13, 2026

Saturday Jun 13, 2026

Wednesday, 26 September 2018 00:00 - - {{hitsCtrl.values.hits}}

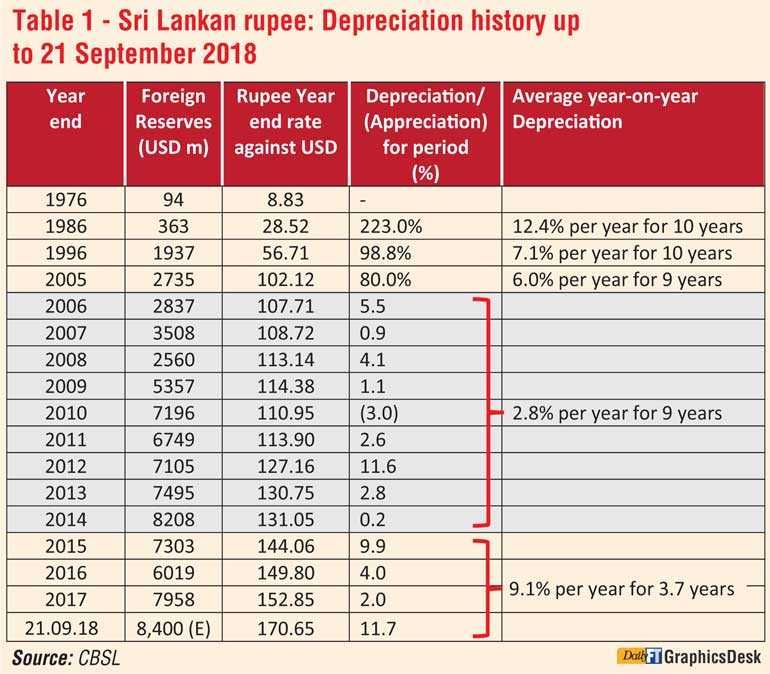

The rupee depreciated by Rs. 29 from 2005 to 2014 and the average year-on-year depreciation of the Sri Lankan rupee was 2.8% per year. Official foreign reserves increased from $ 2.7 billion to $ 8.2 billion over the same period. In stark contrast, the average year-on-year depreciation of the rupee from 1 January 2015 to 21 September 2018 was 9.2% per year.

Official foreign reserves have been almost flat at around $ 8.4 billion when compared to the level at end-2014. Further, reserves are expected to decline rapidly from now onwards with the Central Bank (reportedly) having supplied a staggering $ 60 million (Rs. 10,200 million) to the Forex Market just yesterday, to artificially prop up the crashing rupee.

The Government has claimed that the reason for the rapid depreciation of the rupee is the strengthening of the US economy and with that the US dollar. Many Government MPs rush to explain that all currencies have depreciated against the USD. To support that contention, the Central Bank has carefully selected certain currencies as examples, while neglecting to mention that several have depreciated much less against the US dollar than the Sri Lankan rupee. Knowledgeable analysts know that such contentions are highly amateurish and not tenable, particularly in the context of the Sri Lankan rupee even depreciating against the Bangladeshi, Zimbabwean and Ethiopian currencies.

Caught napping

In any event, all analysts have been fully aware from about a year ago that the US economy has been gradually strengthening and that the USD would be stronger from about mid-2018 onwards. That outcome should have been anticipated by the Sri Lankan Government and the Central Bank as well, and the necessary policy measures should have been implemented well in advance to build up spaces in the Sri Lankan economy in general, and the Central Bank’s Forex Reserves in particular. If the Government and the Central Bank did not prepare for those challenges and were caught napping as they now seem to be indirectly admitting, they have only themselves to blame.

To sidestep the present turmoil and shift blame in his characteristic style, the Prime Minister recently claimed that the rupee had suffered a depreciation of 12% in 2012, even after the Central Bank incurred a large loss of its reserves. In that regard, the Prime Minister needs to be apprised that central banks all over the world carry out such Forex interventions in the interest of economic and price stability and that Sri Lanka is no different.

At the same time, it must also be pointed out to him that the Central Bank reserves actually increased by $ 356 million from $ 6,749 million as at end-2011 to $ 7,105 as at end-2012, and that therefore, contrary to his claim, there was no loss of reserves in that year even after the Forex intervention.

Overall, Central Bank reserves increased from a significantly low level of $ 2,735 million as at end-2005 to a comfortable level of $ 8,208 million by the end of 2014, under the previous Rajapaksa administration. (Please see Table 1). The table also reveals that under Prime Minister Ranil Wickremesinghe, reserves have decreased considerably from the level of $ 8,208 million by end-2014. First to $ 7,303 million by end-2015, then to $ 6,019 million by end-2016 and thereafter to $ 7,958 million by end-2017. Such massive reductions in forex reserves were obviously due to significant interventions by the Central Bank to maintain the value of the rupee.

However, it will be noted that, even with a net dissipation of $ 905 million of reserves in 2015, the rupee depreciated by a substantial Rs. 13.01 per USD (9.9%), while in 2016, with a net dissipation of a staggering $ 1,284 million, the rupee had depreciated by Rs. 5.74 (4.0%) per USD.

Table 1 also shows the level of reserves as well as the depreciation of the Sri Lankan rupee at various time intervals since the liberalisation of the economy in 1977. From that table it can be seen that the Sri Lankan rupee suffered an average year-on-year depreciation of a devastating 12.4% per year for 10 years from 1977 to 1986; an average year-on-year depreciation of a highly detrimental 9.9% per year for 10 years from 1987 to 1996; and an average year-on-year depreciation of an equally damaging 6.0% per year for nine years from 1997 to 2005.

Thereafter, the table shows that from 2006 to 2014, the rupee has enjoyed its most stable era in recent history, with the average year-on-year depreciation recording a manageable 2.9%; with the depreciation of the rupee in 2013 and 2014 (just before the management of the economy passed to the UNP-SLFP combine) being 2.8% and 0.2% respectively.

However, since 2015, reckless policies adopted by the present authorities had seriously jeopardised the stable trend followed by the rupee from 2006 to 2014. Consequently, the currency had assumed an unstable nature, recording frequent patches of volatility, culminating in the current out-of-control phase which is now spelling disaster for the entire economy.

Conflicting signals

This de-stability has been compounded by the fact that confusing signals have been emanating from those in authority, almost daily. Prime Minister Ranil Wickremesinghe claims the “depreciation problem” will be fixed in one month, but warns that the Government may have to curtail imports; Finance Minister Mangala Samaraweera says the Central Bank will not intervene as the reserves have to be safeguarded to settle future debt; economic guru and State Minister Harsha Silva announces that the depreciation of the rupee is “beneficial” to the economy, but requests that high-income people postpone buying luxury cars and delay trips to Alaska; Finance State Minister Eran Wickremaratne proudly asserts the Sri Lankan rupee is the “strongest currency in Asia”; Governor Dr. Indrajith Coomaraswamy proclaims the Central Bank is “ready to prevent excessive volatility”; and Senior Deputy Governor Dr. Nandalal Weerasinghe insists the Central Bank “will intervene aggressively”.

Meanwhile, the IMF cautions that the Central Bank needs to build up further reserves instead of intervening, while currency dealers refuse to speak, citing instructions from the Central Bank. Through all this, President Sirisena keeps silent, perhaps because he has still not seen the newspaper reports about the rupee’s freefall!

All in all, it is clear that this inept Government has dragged the Sri Lankan economy to the brink of disaster, and that a massive hotchpotch of policy contradictions has led to the serious undermining of the Sri Lankan rupee. In that pathetic background, this Government must be firmly told to stop trotting out lame excuses and blaming the previous Government and/or other foreign governments for everything they cannot get right.

The Government has also shown in no uncertain terms that they are totally incapable of dealing with the complex problems of the economy and that they are only good at worsening the crisis by their confusing statements and reckless policies. Therefore, the only sensible option now open to the country is to allow the people to forthwith elect a new government that the people believe will be able to save Sri Lanka from the impending economic disaster that is now very close at hand.