Tuesday Feb 24, 2026

Tuesday Feb 24, 2026

Monday, 25 October 2021 04:00 - - {{hitsCtrl.values.hits}}

By Nisthar Cassim

|

| Expolanka Holdings Founder, shareholder and Group MD Hanif Yusoof

|

Relatively young Expolanka Holdings PLC added another feather to its corporate cap by becoming the first Sri Lankan company to be worth over $ 2 billion in a short span of time apart from being the country’s most profitable.

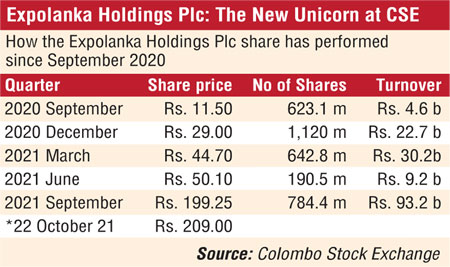

The tag of “first $ 2 billion” company was achieved on Friday when Expolanka’s share price closed at Rs. 209 up by 3.7% or Rs. 7.50 on Thursday. On Friday it had garnered a market value of Rs. 408.58 billion or $ 2.01 billion. For the week it gained by 13.25% and touched an intra-week high of Rs. 209.75. When Expolanka became the most valuable listed entity on 23 August its price was Rs. 122.50 and market capitalisation was Rs. 240 billion. It ended 2020 with a market capitalisation of only Rs. 57 billion and was ranked at number 13.

Between September 2020 closing and to last Friday, Expo share price reflects a whopping 1,717% gain. From the end June-2020 closing, the last week’s price is a whopping 6,431%. Expolanka Holdings Founder, shareholder and Group Managing Director Hanif Yusoof, when contacted by the Daily FT on reaching the $ 2 billion company milestone, said the beneficiaries of the company’s growth have been shareholders, customers, partners and employees apart from Sri Lanka itself and the Colombo stock market.

“After listing Expolanka, the aspiration was to be among the Top 10 but the universe has to date given Expolanka more than what we imagined,” said the low profile and unassuming Hanif.

Japan’s SG Holdings Global Ltd. owns 75.6% stake in Expolanka Holdings while Hanif Yusoof owns 7.5%. In tandem with its upsurge, Expolanka has seen the public shareholder base increasing by nearly 4,500 since FY20 to 13,719 by June 2021 whilst the public float is 16.6%.

COVID-induced opportunities saw Expolanka end FY21 with a hefty net profit of Rs. 14.8 billion as opposed to a loss of Rs. 438 million in FY20. Group revenue rose by 111% to Rs. 218.7 billion. In the first quarter of FY22, it saw a 259% YoY growth in Group Profit After Tax to Rs. 6.3 billion and a 165% YoY increase in Group revenue to Rs. 95.7 billion.

To bolster its business, Expo did several strategic acquisitions, a route it is likely to pursue further. In the past six months, Expolanka has made three acquisitions investing $ 18 million. Latest was in early September acquiring 100% stake in US-based bonded container freight station and trucking services Completre Transport System LLC for $ 6.1 million.

In August it acquired Central American firm IDEA Logistics LLC and its group of companies for $ 9.7 million. In March Expolanka bought 100% of US Seville Container Freight Station Inc. and related companies for $ 2.2 million.

Nation Lanka Equities (NLE) in a research report last week said Expo growth evolved in four stages. First was the restructuring in 2013/2017 which enabled the Company to redirect resources and focus on its core business.

Second was the purchase of a majority of the shares by Japan based SG Holdings in 2014/2016, which helped Expolanka to realign its strategies further.

NLE also said Expo’s focus on consolidation and its ambitious growth plan during the 2017/2019 period helped it to expand its global footprint and develop service capabilities.

The fourth phase was Expo laying the foundation way back in the 2017/19 period helping EXPO to navigate successfully especially during this pandemic period.

It said Expo’s base case scenario suggests 100%YoY upside in profits for FY 2021/22.

NLE arrived at a base case scenario when deriving profits for Expo. “We have assumed a considerable jump in volumes specially ahead of the festive season underpinned by elevated rates for FY 2021/22 and have adjusted the profits up to Rs. 29.5 billion from the recent update.”

Beyond FY22 NLE has assumed a moderate pickup in volumes aided by expansions, however adjusted the freight rates which may settle with likely shocks on virus-related uncertainties cooling off.

In its bull case scenario however NLE has assumed the rates to remain high while volumes pick up rapidly on the back of major acquisitions.

“Our bear case scenario conversely assumes volume pick up in mid to high teen levels and a gradual drop in rates,” NLE said.

In its opinion Expo warrants to trade at global peer multiples after transforming to a truly global company. “EXPO has transformed into a leading player in the global logistics sphere during the past few years becoming the 19th largest in the non-vessel operating companies in the world,” said NLE.

Its restructuring process by aligning the strategies to core business verticals and expanding its global footprint has successfully paid off during these trying times helped further by elevated yields. The near-medium term performance will be based on aggressive acquisition drive of EXPO which would further help cement EXPO’s position by locking up and attracting existing clients whilst also acquiring new customers through a range of peripheral services.

Given EXPO’s solid global footprint and its foreign currency earning capacity, NLE firmly believes that EXPO should now trade on par with global peer multiples. Even after conservatively taking a 15.5x-16.2x earnings multiple on FY 21/22E earnings, which is still a 26%-30% discount to the average trading global peer multiple, EXPO should trade at Rs. 234.00-246.00 levels, a 12%-18% upside to the current market price.

“However, if we take a more optimistic approach, and consider the bear market scenario, the counter has the capacity to even trade at a 40% premium to the current market price. Thus, given this scenario we maintain our recommendation BUY,” NLE added.

Capital Trust Securities in its latest research on Expolanka released over the weekend put the stock’s fair value at Rs. 307.25.

It said Expolanka is currently trading at a PE of 10.97x FY22F and a PE of 9.77x FY23F respectively.

“We expect the counter to record strong earnings growth given elevated freight rates, growth in volumes ahead of US peak season, enhanced service offerings and expansion of reach through several acquisitions,” Capital Trust said adding: “With over 93% of Revenue in foreign currency including 63% from US, the Stock provides a natural hedge for investors against the LKR depreciation.”

Capital Trust expects the counter to trade at a premium to the broader market PE as it provides investors protection against the performance of the Sri Lankan Economy, exposure to the US economy and a global multinational with robust earnings growth.

“Considering the Peer Average PE of 20.25x Forward earnings and Market PE of 12.02x on a 50%: 50% basis, we expect the Stock to trade at a PE of 16.13x FY22F and a Fair Value of Rs. 307.25,” Capital Trust added.

Expolanka clarifiesIn reference to the article titled “Expolanka elevates to first with $2 b market cap.”, published on Monday 25 October, the Company clarified that Expolanka does not provide earnings guidance or forecast to investors nor comments on the estimates or valuations provided by brokers. We regret the error. |