Sunday Feb 22, 2026

Sunday Feb 22, 2026

Thursday, 18 August 2016 00:00 - - {{hitsCtrl.values.hits}}

Industry veteran and Ceylon Tea Brokers Plc Chairman Chrisantha Perera in the company’s 2015/16 Annual Report has come out with a compelling case for urgent and right actions to give much needed boost for the struggling tea sector. His review well encapsulates the status of the tea industry, some of the causes, challenges ahead and the way forward. Given its relevance, the Daily FT reproduces excerpts from Chairman Chrisantha Perera’s review in Ceylon Tea Brokers Plc 2015/16 Annual Report:

As a company, we continue to be a standalone tea broker with the connected services associated with this function. Therefore, the performance of the Sri Lankan tea industry in particular and the global tea market in general is directly related to the success of our company. I would therefore like to share some important facts and thoughts for consideration by all concerned.

The year under review proved even more challenging for the company than 2014/15. The decline in tea prices following the unsettled global economic conditions as well as volatility in the Middle East Region coupled with the sharp decline in oil prices which affected the main export markets for ‘Ceylon Tea’ had an adverse impact on tea prices.

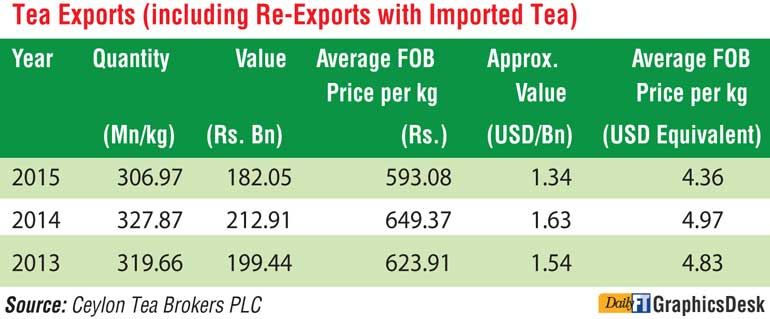

Tea export earnings at approximately $ 1.34 billion accounted for 12.8% of total exports and about 1.63% of the GDP in 2015 compared with $ 1.63 billion representing 14.60% of total exports and around 2.03% of GDP in the previous year.

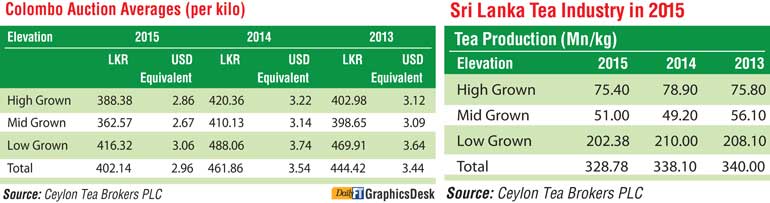

Tea production was lower by almost 10 million kilos compared to 2014 following adverse weather conditions which affected the Low Grown segment in particular, which accounts for the highest volume. An encouraging feature was the slight increase in the Medium Grown production at 51 million kilos compared with 49.2 million kilos in 2014.

The table clearly reflects the sharp decline in Colombo Auction averages in 2015 compared with the previous two years with 2014 being the all time high. The drop in the USD equivalent figure was even greater reflecting the depreciation of the SLR vis-à-vis the USD over the past two years. At the time of compiling this report, there is some hope for cautious optimism that tea prices at the Colombo auctions could strengthen during the second half of the year on the expectation of more settled conditions in the Middle East, lifting of sanctions in Iran and a pickup in oil prices which could also help the Russian economy, currently the largest tea importer globally.

The drop in quantity coupled with the lower prices has resulted in a substantial decline in tea export earnings. From the all-time high of 327.87 million kilos generating Rs. 212.91 billion in export earnings amounting to approximately $ 1.63 billion in 2014, 2015 has realised a total value of only Rs. 182.05 billion on an export of 306.97 million kilos amounting to an approximate Dollar value of $ 1.34 billion. In fact, it is noteworthy to point out that earnings expressed in USD terms in 2015 are the lowest in five years, which is indeed disappointing.

Sri Lanka, in our view, cannot operate in isolation without accepting the importance of integrating with the global trend. To demonstrate this position, we set out below some information we have gathered from a publication put out by the International Trade Center giving export values generated from tea in 2015 from selected countries:

We must point out that five countries in the above table, i.e. UAE, Germany, Poland, UK and the USA are non tea producing countries. A further significant fact is that for the first time in the last decade or more, Sri Lanka has lost its established position as the highest value exporter. It will be noted that China with a total value of approximately $ 1.38 billion has surpassed the export value of tea from Sri Lanka of $ 1.34 billion. This is indicative of the position that we have lost out on the so-called value addition that Sri Lanka enjoyed in the past which generated greater export earnings, even though the volume of exports was lower than some of the larger tea producing countries such as China and Kenya.

It is important to analyse why this should be so. In our view, the above table probably demonstrates the developing trend in the global market whereby non tea producer countries appear to be establishing themselves as value added destinations not only for their domestic consumption, but more importantly for re-exports.

Dubai, since establishing itself as a tea hub, continues to be one of the biggest importers of Sri Lanka tea. The majority of tea imports have been in bulk form with the major component being utilised for blending and re-exports.

Sri Lanka, whilst being a top category tea exporter in the world, does not appear to have the ability to penetrate into new markets effectively. China, Kenya and India have seen an upturn in their export earnings from tea in 2015 compared with 2014, whilst Sri Lanka has reversed their export earnings fairly substantially, which is reflected in the table set out below.

It is important to realise that the oil rich Middle East Region and Russia which dominated our tea market in the past, may no longer be a factor to the same extent in the future. We therefore need to widen our market horizons including new emerging possibilities such as China. It must be stressed that out of the five leading tea importing countries, namely Russia, Pakistan, UK, USA and Egypt, we have a significant presence only in Russia.

According to reports, the global export value of tea in 2015 amounted to around $ 7 billion. 68.7% of this value originated from Asia, with Europe accounting for 15.2% and Africa for around 11.7%. The fastest growing tea exporting countries including re exports since 2011 are United Arab Emirates 82.6%, the United States 49.5%, China 43.3% and Japan 42.4%. Whilst non producer countries seem to accelerate their re export marketing drive, India, Kenya, China and probably most of the other tea producer countries appear to follow suit.

In fact, India so far this year has out-placed Sri Lanka as the largest supplier of tea to Russia with 11.67 metric tons during the first quarter of 2016 compared with 9.1 metric tons from Sri Lanka. India also appears to be leveraging on trade ties with Iran. Iran, India and Afghanistan are reported to have agreed to revive a project to build a trading corridor that would connect Afghanistan to the Indian Ocean via Iran.

In this emerging global scenario, it is important that the Sri Lanka Tea Industry needs to look at pragmatic solutions and implement decisions to make our presence felt in the ever expanding global Tea market. Solutions and opportunities are out there, but our ability to step out of our comfort zone and create constructive change by facilitating tangible expansion in export markets as well as taking proactive decisions are still to be seen.

In this respect, as mentioned in our review last year, we would once again stress that we should urgently examine the hotly debated topic of making Sri Lanka a Tea Hub without compromising the inherent value of marketing Pure Ceylon Tea. We are confident that we could have the best of both worlds if the industry can work together to make this a reality.

We believe all segments of this great industry should consider the priorities in the following order:

1. How is the global market performing?

2. What is best for the country?

3. What is best for the industry in general?

4. How do we adopt these priorities to the sector we are associated with?

5. How can our company maximise these benefits?

As mentioned earlier, the reported total global value of exports in 2015 amounted to approximately $ 7 billion. The total retail value, including sales in tea producer countries could amount to around 10 times this figure. We should appreciate that marketing of tea has moved from a mere commodity to a beverage, with new innovations such as Ready to Drink Teas (RTDs) etc. continuing to grow substantially.

Therefore, if Sri Lanka opens up its borders and have the correct policies with the necessary regulations and controls in place, as well as encourage investment opportunities in tea companies and brands overseas, given our inherent strengths, we could achieve around 10% share of the global retail value within the next decade. Optimistic, but not impossible.