Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Wednesday, 13 May 2015 01:30 - - {{hitsCtrl.values.hits}}

By Ceylon Tea Brokers Plc

The Sri Lankan Tea Industry’s first quarter was not as resilient as the same period in 2014 due to global politics and subsequent economic downturns. However, the industry hopes to recover some of its lost momentum in the second half of the year due to the current stabilisation of the rouble and the shifts in foreign policies in the Middle East.

The Quarterly Auction Averages were further affected by the appreciation in the dollar against global currencies, which subsequently affected the purchasing power of our biggest export destinations of Russia and the Middle East. Additionally, the decrease in revenue from the oil trade has further impacted the buying power and consequently the importation of tea from these nations.

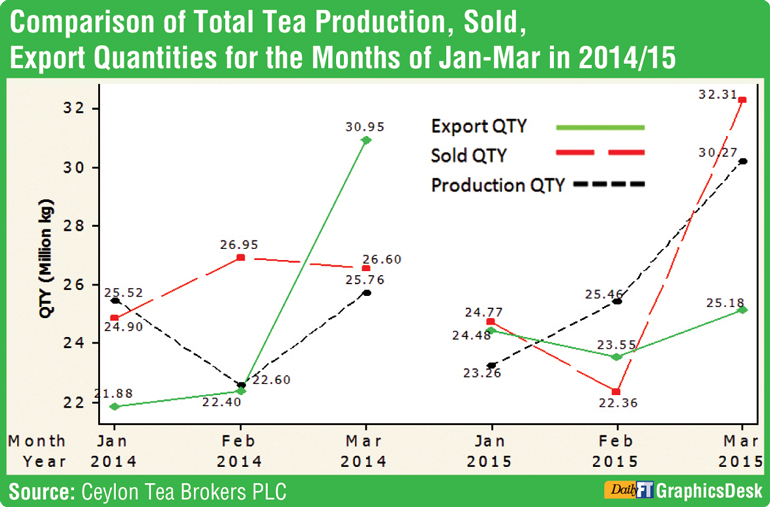

Sri Lanka’s total tea production for the first quarter of 2015 was recorded as 79.08 million Kgs in comparison to 73.87 million Kgs (+5.21 million Kgs) for the same period last year. The YOY higher production has also created an excess supply in the market, which has not been offset due to a decline in exports. The quality of teas during the Western Season was somewhat compromised due to climatic change which affected production of seasonal quality teas.

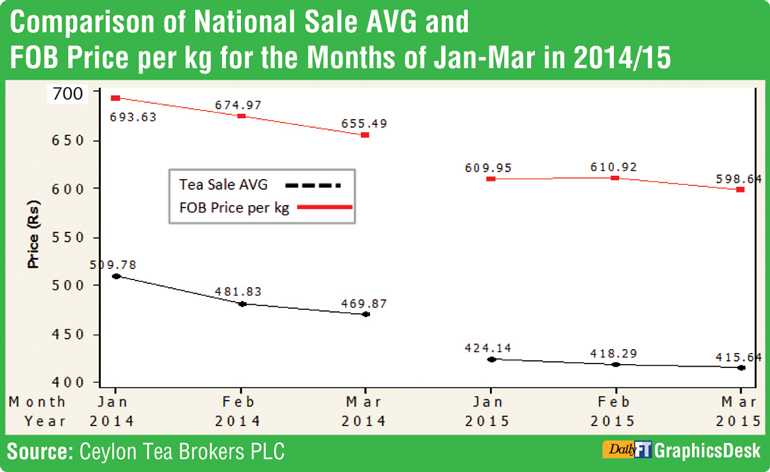

The total national average of teas sold for the first quarter of 2015 was Rs. 419.04 in comparison to Rs. 486.65 (-Rs. 67.61) for the same period last year. The rupee and the US dollar equivalent average for the first quarter of 2015 shows a decline from the corresponding averages of 2014 as well as 2013. Low Growns, having the largest market share with 65% of production, recorded the sharpest decline at -Rs. 83.93, with Mid Growns recording a decrease of -Rs 46.86 and High Growns seeing the least reduction of -Rs 37.57 YOY. Low Growns averaged Rs. 430.71, Mid Growns recorded Rs. 384.93 and High Growns Rs. 405.79 for the cumulative period from January to March 2015.

Sri Lanka Tea Exports for the first quarter of 2015 amounted to 73.21 kg million, a decline of 2.2 kg million from the same period last year. The FOB average price per kilo for this period stood at Rs. 606.37 in contrast to Rs. 672.38 (-Rs 66.01) YOY for the same period. The export of tea bags fared more favourably than packeted teas with bulk teas being the most adversely affected.

The total revenue realised for the first quarter of 2015 from tea exports was Rs. 44.39 billion. A sharp decline from Rs. 50.58 billion (-Rs. 6.19 billion) recorded last year. Russia, formerly the largest buyer of Sri Lankan tea, lost its place to Turkey as a result of it being affected by the sharp devaluation of the rouble, which had an impact on its imports. Iraq increased its purchase volume considerably, while a slight decline was seen in Iran’s buying quantity. Though not being a major player in the Sri Lankan tea trade in the past, India has shown a notable increase with an 88% augmentation in exports YOY. The United Arab Emirates emerging as a regional trading hub has almost doubled its imports for the quarter YOY.

Russia, due to the current stabilisation of the rouble and the steady appreciation in oil revenue, is likely to see an increase in the purchase of tea from Sri Lanka. However, Russia’s current increases in purchasing the lower cost teas from other origins could adversely affect the possibility of our exports regaining its former market share.

Turkey, though currently the market leader due to Russia’s decline in tea Imports from Sri Lanka, has in fact marginally decreased its purchases for the first quarter compared with 2014.

Iran, after the potential lifting of the embargo by the P5+1 countries at the end of June, could see a significant change in its economic potential, especially in the oil sector, which in turn could enhance its purchasing power. This could potentially be beneficial to the Sri Lanka’s Tea Industry.

Despite the current situation in Iraq there has recently been a significant increase in their purchase of Sri Lankan tea. As the Iraqi import of Sri Lankan tea appears to be unaffected by its political climate, the steady increase in purchases should continue.

Syria and Libya have shown a decline in their purchases compared to 2014. There may be expectations of a revival in demand from these two important markets as the year progresses.

The United Arab Emirates has since recently established itself as a hub for tea. The UAE has almost doubled its presence since 2014, currently making it the fourth largest export destinations of tea from Sri Lanka. With its infrastructure in transport and industrial development as well as its ability to offer business incentives for foreign trade, the UAE is expected to be a significant contender in increasing its market presence in the Sri Lankan tea industry.

Among the emerging markets China and India appear to be increasing their market share in Sri Lankan tea imports which could provide future benefit to the Sri Lankan tea Industry.

Summarising the above factors, significant changes in the auction averages are not to be expected in the short term. However, an anticipated depreciation of the rupee against the US dollar could have a beneficial impact on rupee prices. A possible rise in oil prices, with the potential lifting of the embargo in Iran and the stabilisation of the rouble, should have a positive impact on the auction averages during the second half of 2015.

We are therefore cautiously optimistic for the rest of the year, although the first quarter performance in 2015 has been disappointing compared to the corresponding period in 2014.