Wednesday Feb 11, 2026

Wednesday Feb 11, 2026

Friday, 8 July 2016 00:00 - - {{hitsCtrl.values.hits}}

History of CSR

The notion of Corporate Social Responsibility (CSR) was initially introduced by William Bowen in the publication ‘Social Responsibilities of the Businessman’ in 1953. Since then many globally recognised organisations such as OECD and individuals such as Morell Heald, have voiced their opinion on CSR.

In the late ’80s and ’90s, CSR was highlighted from the stakeholders and the ‘societal’ perspective as a means of stimulating economic growth, smoothing out social inequities and countering poverty in the society. CSR in the ’90s and the early millennium was perceived as a moral obligation towards the society.

In the late ’80s and ’90s, CSR was highlighted from the stakeholders and the ‘societal’ perspective as a means of stimulating economic growth, smoothing out social inequities and countering poverty in the society. CSR in the ’90s and the early millennium was perceived as a moral obligation towards the society.

Modern-day CSR

CSR in the contemporary world has demonstrated its exigency, not only as a moral obligation by companies towards the society, but also going beyond the given peripheries of the society, forcing companies and the Multinational Corporations (MNCs) to walk the ‘extra mile’ in the home country as well as the host nation. Research has revealed that the general public possesses a better perception of MNCs’ in the long term, when such companies walk the extra mile and actively support the societies in their host nations. For instance, the restoration of the Christ the Redeemer statue in Brazil in 2010 was sponsored by many multinational companies in Brazil such as media company Rede Globo and oil company Shell Do Brasil.

Considering the ruthless competition between organisations in the world today, and the way corporates and the multinationals strive only to strengthen the bottom line and to maximise their wealth, the bitter truth is that these companies ignore all accepted ethics in business, humane values and even the health concerns of the society, in order to achieve their objectives. A well-known example of this is the case of a large multinational company which sold contaminated milk food to underdeveloped African nations at a concessionary price and then distributed medicine through the company’s own pharmaceutical arm to those who fell ill from the contaminated milk food.

Thus, such corporate entities and multinationals have a definite moral obligation towards the society, as the society is one of the key stakeholders for a company under stakeholder mapping. Therefore, when companies get engaged in CSR the following has to be contemplated.

The success and performance of companies depend wholly on the Society and the environment, as they include all stakeholder groups and the resources used by these organisations. Therefore companies should give something back to the society in good faith as their corporate responsibility, in exchange for the use of such resources.

As CSR is a voluntary compliance of social responsibility of companies with a long term continuity plan, this compliance does not end with one CSR activity. Due to this reason, many modern companies include CSR activities at the strategy formulation level involving the top management with a specific plan for at least two to three years. Similar to Risk Compliance or Audit Compliance, CSR Voluntary Compliance should also have a continuation process. CSR should be incorporated into the DNA of the future corporate world which is the envisaged notion of many modern day MNCs.

However, from the Sri Lankan perspective, the reality is that the majority of these local companies do not have separate divisions for CSR and Sustainability. Most of the CSR activities in Sri Lankan companies are carried out at the whims and fancies of the Top Management without proper planning. In fact CSR and Sustainability are not incorporated into the long term strategy of the company. Companies in Sri Lanka engage in CSR activities either for the sake of performing some CSR activities, or with a hidden marketing agenda, in order to gain more than the amount expended for the noble cause.

While there are many types of acknowledgments and awards for the CSR activities carried out by companies, unfortunately the local bodies that bestow such awards are ignorant of the fundamentals of CSR and the underlying motives of the activities carried out by such companies. Instead they merely rely on the CSR and Sustainability Reports in the Annual Financial Statements. Activities such as distributing free soft drinks in the canteen for employees, or distributing educational books for the members of the employees’ families, are often categorised as CSR projects in the Annual Reports. However these are merely welfare activities or donations and cannot be truly considered as CSR activities.

The CSR Code which was introduced in India in 2013 clearly defines CSR as a pure social activity where the contributions and the benevolence of CSR should be quantifiable. Further its impact should be measureable in turn from the society. It also says that there should be a separate division for CSR in the organisation, similar to the other functional divisions such as Business Development, Strategic Planning, Human Resources, Information Technology and Finance. In addition, every CSR activity should carry a Board Resolution of the company with the date specifically stated and every CSR activity should be a ‘project’ of the company. Needless to say, if it is a project there should be a definite beginning and a specific end with clear cut and meticulously framed objectives.

In addition the CSR code (in India) further states that CSR activities should be considered as a project, and has to be assigned to a recognised NGO, which should in turn be registered within the country as a Non-Profit Organisation, have served the nation for a minimum of 10 years, and should have financial statements audited by a reputed audit firm. The purpose of assigning such CSR activities to NGOs is that the staff or the employees of the company concerned do not have adequate time to fully get involved for two to three years considering the work volumes and other involvements in their day to day office activities.

At the Global CSR Awards held in Mumbai, India this year, at which this author was present, Dr. Bakshar Chatterjee, Director and the CEO of the Indian Institute of Corporate Affairs, stated that out of approximately 11 million companies registered in India, only 16,237 companies genuinely carry out CSR activities that fall within these parameters. His statement was met with much astonishment of all the leading Indian businessmen who were present at the event.

This amply demonstrates not only the reality of CSR in India, but also how many companies in India are just carrying out CSR activities for the pure sake of adding pictures to their annual reports. In Sri Lanka too, out of the many hundreds of large companies carrying out CSR activities, not even 20 would qualify as carrying out true CSR activities as per the Code. This is a huge challenge for corporate entities.

Sustainability

While companies were paying attention firstly towards profitability, and secondly, the society, a visible and up-surging necessity emerged from the scientists, researchers and the environmentalists to pay greater concern towards ecological factors, due to continuous carbon emission, deforestation, global warming and declining energy sources.

The ‘Triple Bottom Line’ (TBL) concept was first introduced by John Elkington in 1994 (upon introduction of the Concept of Sustainable Development at the UN Conference in Rio De Janiro in 1992), argued that the three ‘Ps,’ namely Profits, Planet and the People of the Triple Bottom Line (TBL), should aim to measure the financial, social and environmental performance of a company over a period of time ascertaining the full cost involved in performing business. Therefore, CSR which was initially focused on the societal aspects, has now transformed to focus on CSR and sustainability.

Sustainability can be defined in simple terms as the ability to utilise the resources required to carry out business operations without jeopardising the potential of these resources for the people of the future generations. Though one should not use CSR and sustainability interchangeably, sustainability entails the broader and unfathomable expectations of the society and the planet. Hence, the overarching objectives of any social responsibility agenda or programme should be to add value and to contribute to sustainability. As such, the envisaged and futuristic approach to CSR activities, which formerly focused mainly on ‘Society’ would most likely be embedded as a part of sustainability.

Based on this approach, some of the Millennium Goals of the UN initiative focus on achieving higher standards of CSR, solving human rights issues and health issues, poverty alleviation, higher labour standards and establishing anti-corruption measures across the member nations. Such activities fall under the ‘societal’ or the ‘People’ (P) under sustainability. These are some of the overlapping arenas between CSR and sustainability.

Economic sustainability

Economic sustainability is to formulate strategies to utilise existing resources to the optimal level where beneficial and responsible balance can be maintained over the long term. From the commercial perspective, this is to make use of assets of the company effectively to allow the company to function in a profitable manner continuously.

As the modern day companies strive to maximise the economic sustainability under whatever the circumstances, this article does not intend to elaborate as to how the profitability can be sustained and the common aspects engulfing ‘profitability’. However the article contemplates ‘challenges’ from the sustainability perspective.

Companies should maximise their profitability while striving to minimise the usage of resources (human or non-human) which should be quantified in monetary terms and otherwise using appropriate measuring techniques. Declaring the year-on-year profit growth as a percentage at least for the last three years is more prudent compared to indicating the profit growth merely as a percentage against the previous year. The challenge is to declare the net profit growth after deducting the average inflation rate for the corresponding year.

Economic sustainability does not exist in companies if the profitability reflects widely fluctuating ‘peaks and valleys’ over a period of time. It is also observed, that few companies which win awards in a particular year do not even get selected for the same award in the ensuing year. This is an indication of either the competitors in the industry have overtaken that company or their sustainability is in jeopardy.

More importantly, companies have to be ethical, without deviating and manipulating from the accepted norms and standards especially when the profits decline. This is another challenge. This is fundamentally ethics vs. sustainability.

Social sustainability

Despite the ever-increasing emphasis on CSR and sustainability across the world, the fact remains that the attention paid by companies to such aspects is grossly inadequate, especially considering the exigency of the situation with regards to income inequality, ecological destruction and rising poverty levels. In Sri Lanka it is reported that more than 6% of the population earn less than $2 per day while the economy strives to exceed a much larger per capita income. Another example is that based on the very concept of Sustainability, the country should have an intelligent, educated and non-dependent society for the next generation. However doing away with the pension scheme by the corporate giants in Sri Lanka in order to strengthen the bottom line creates a scenario where the ageing population would become dependent on society. Which corporate will commence/recommence the pension scheme for their employees under societal sustainability? This is a challenge.

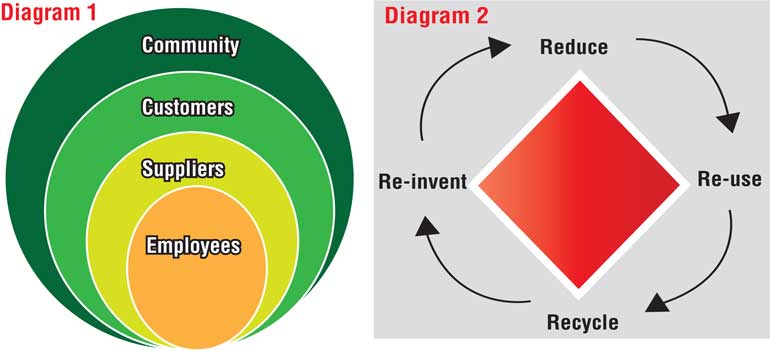

Diagram 1 depicts the four layers of social sustainability. Based on the graphical illustration, one can argue that if a company does not treat their employees properly under labour regulations, equality, diversity and human rights, how can that company treat the community under social justice? Examples of acts of social sustainability are protecting human rights, moral labour practices, health, safety and wellness policies to avoid health hazards within the organisation etc. The external factors companies should focus on are enhancing social capital, upholding social justice, and enhancing community resilience.

Companies must take the leadership to create societies similar to the Mondragon Cooperation of Spain, where a series of consumer cooperatives which assist and aid each other was created to help the citizens of the Mondragon Village in Spain survive the post-World War II era. Some possibilities from the social sustainability perspective are taking the leadership and the initiative to eradicate the Dengue menace, drug menace and educating the non-school going children in Sri Lanka. As such, the basis for societal sustainability is twofold, namely, ‘Do no harm’ and ‘Make a visible positive impact’ to the society.

Ecological sustainability

From the ecological perspective, many companies hesitate to spend on Research and Development even as ‘Syndicated Research’ to explore the possibility of generating new energy sources, improve water management, garbage re-cycling, reduction of carbon emission and energy saving activities, as such research does not contribute directly to company performance or the bottom line. The cardinal objectives of ecological sustainability is not only to reduce the volume of carbon emissions, avoid nuclear testing and contamination and prevent catastrophes such as the British Petroleum Oil spill in the Gulf of Mexico, but also to protect and conserve the existing natural resources and the ecology, in order to hand over a “safe and secure” planet to the future generations.

Several leading companies in Sri Lanka have adopted ecologically sustainable and quantifiable measures with appropriate metrology by benchmarking their parent companies in developed nations. This should be appreciated and admired. Perusal of these annual reports of such companies reveals a marked difference compared to other local firms. However, the majority of the companies in Sri Lanka are yet to take visible and significant measures under this facet and must walk the talk and engage in sustainable activities instead of simply restricting them only to the official website and the ‘camouflaged’ Annual Reports.

Auditors have a prime duty to inspect all CSR and Sustainability projects, and ascertain the impact and quantify the positive contributions made using appropriate metrology and measurement techniques before the audited accounts are certified. Sustainability must be practised at all levels, and not just on the surface. A prime example of this in Sri Lanka is the Smoke Certificate, where the importance of the Smoke Certificate for private motor vehicles is emphasised continuously; no such benchmark is assigned to public transport vehicles such as buses and train engines in Sri Lanka, which emit a larger quantum of noxious black smoke. Some of the possible actions which can be implemented by the corporate entities are given below:

Conclusion and directions

A study covering over 30 large corporations for sustainability initiatives revealed that Sustainability is a mother lode of organisational and technological innovations that yield both bottom-line and top-line returns. Becoming eco-friendly lowers costs, the processes generate additional revenues from better products as companies end up reducing the inputs they use. In fact, because those are the goals of corporate innovation, the smart companies now treat sustainability as innovation’s new frontier.

Indeed, the quest for sustainability is already starting to transform the competitive landscape, where early movers will develop competencies that rivals will be hard-pressed to match. That competitive advantage will stand them in good stead, as sustainability will always be an integral part of development. Some of the directions for the companies for sustainable compliance on step by step basis are depicted below.

Step 1: View compliance as an opportunity

Step 2: Make value chains of the organisation sustainable

Step 3: Design sustainable products and services

Step 4: Develop new business models

Step 5: Create next-practice platforms

It is a matter of overcoming ‘cognitive and perceptual barriers,’ the task which will not be a simple one for organisations. But most of the companies have embarked on the ‘5 stage’ journey. Mapping the road ahead meticulously and professionally will save companies’ time, and that could be critical, as the clock is ticking.

[Dr. Trevor Mendis, Strategist, Management Consultant, and Academic, is attached to the Postgraduate Institute of Management (PIM) as a Senior Management Consultant. Recipient of two international awards, his expertise expands to six incomparable arenas namely, Strategic Affairs, Corporate Governance, International Trade, Re-engineering of Companies, Banking and Tertiary Education.]