Saturday Mar 14, 2026

Saturday Mar 14, 2026

Monday, 14 March 2022 00:20 - - {{hitsCtrl.values.hits}}

Replacing promised commission with a council

President Gotabaya Rajapaksa has appointed an Economic Council some 26 months after being sworn in as the President of the Republic. The Terms of Reference of the Economic Council is not available in the public domain which does not go well with the democratic governance system that he had promised to establish.

which does not go well with the democratic governance system that he had promised to establish.

In his manifesto, titled, Vistas of Prosperity and Splendour, he had promised to establish an all-powerful economic commission, ‘National Policy, Planning, and Implementation Commission’ under the chairmanship of the President to steer the ailing economy. Pledging to disband the existing National Economic Council established by the former President Maithripala Sirisena and the Strategic Enterprise Management Agency established by his elder brother Mahinda Rajapaksa, the new commission was to undertake a vast array of work relating to the economy.

Its job was to formulate national policies and plans, determine public investment, formulate national development strategies, monitor the procurement process, and undertake project analysis and management. All these works were central to the national development process. The establishment of the commission, it was held, would ensure transparency in economic policy formulation and implementation.

India’s commissions are run by professional economists

The title of this commission implied that it was like the Planning Commission of India which functioned till 2014 when it was dissolved by the Modi Government. It was staffed by top class economists who had been drawn from both inside and outside India and its main function was to formulate, implement, and progress-monitor the five-year plans introduced as rolling plans. Considering the changing global economic environment, it was replaced by a new venture called National Institution for Transforming India or NITI Aayog.

It is to function not as an authority but as a public policy think tank that would advise the Government on the measures it should take to transform India to meet the challenges of the 21st century. Among many initiatives it has made so far include a 15-year Road Map, and 7-year vision strategy, and action plan. It is run by professional economists. A close counterpart in Sri Lanka to NITI could be the Institute of Policy Studies or IPS which has not received the due recognition from all the governments that had been in power ever since it was set up in late 1980s.

A council sans economics inputs: Use IPS as advisor

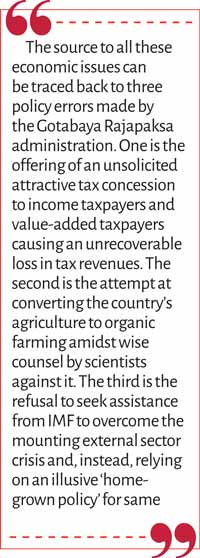

It is not clear where the newly established Economic Council will stand among these diverse models. Surely, it is not a commission as was promised. Nor is it a think tank of the Government since it is made up of top-level politicians whose competencies are not in economic policymaking but in other areas. The four outside members on the Council are not trained economists but those competent in other professions like public administration or accounting.

not a commission as was promised. Nor is it a think tank of the Government since it is made up of top-level politicians whose competencies are not in economic policymaking but in other areas. The four outside members on the Council are not trained economists but those competent in other professions like public administration or accounting.

Hence, it can be categorised as a Cabinet Sub-committee on Economic Affairs like the Cabinet Committee on Economic Management that functioned under Prime Minister Ranil Wickremesinghe in the previous Yahapalana Government. Hence, to feed it with the necessary economics input, it is advisable that the Council relies on a think tank like IPS which is independent, objective, and staffed with top-class economists. Without this input, the Council is likely to run into the problem of making erroneous decisions as pronounced by the 19th century French Economist, Frederic Bastiat.

He distinguished a good economist from a bad economist by referring to his ability to see things to be foreseen in addition to what can be seen; a bad economist just sees only what can be seen and does not have a view on the long-term consequences of a policy. What this means is that if the Council is to make good decisions it should be aware of all the subsequent consequences of its policy actions, both favourable and adverse. If this is not done, like the conversion of Sri Lanka’s agriculture to organic farming overnight, the economic costs of the policy actions of the Council will be enormous and irrecoverable.

Worst economic catastrophe in post-independence history

At present, Sri Lanka is undergoing the worst economic catastrophe in its post-independence history. The real economy is shrinking with a negative or a near zero economic growth, inflation is rising its ugly head with food inflation running at 25%, foreign reserves are a pittance forcing the country to seek hand-outs from countries like Bangladesh, rupee is under pressure for a mega depreciation, the insane attempt by the Central Bank to fix it artificially without reserves at 230 per dollar has given rise to a lucrative black market, and all essential items like fuel are in short supply making long queues for them a daily occurrence.

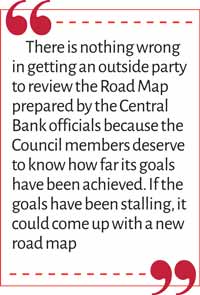

The source to all these economic issues can be traced back to three policy errors made by the Gotabaya Rajapaksa administration. One is the offering of an unsolicited attractive tax concession to income taxpayers and value-added taxpayers causing an unrecoverable loss in tax revenues. The second is the attempt at converting the country’s agriculture to organic farming amidst wise counsel by scientists against it. The third is the refusal to seek assistance from the IMF to overcome the mounting external sector crisis and, instead, relying on an illusive ‘home-grown policy’ for the same.

Treasurer to Parakramabahu I: ‘Your Majesty, your Treasury is empty’

It may be useful for the Council to look at the tax issue closely and identify how the Government's top policymakers have misled the President. A good example can be found from Sri Lanka’s history. According to Chulavamsa, when Parakramabahu, the First, became the overlord of the Dhakshina Desha, the enterprising young king wanted to bring the whole island under one rule. He had asked the Treasurer of the Dhakshina Desha, the counterpart of the head of modern treasury in Sri Lanka, whether he had enough resources to wage war against other overlords.

have misled the President. A good example can be found from Sri Lanka’s history. According to Chulavamsa, when Parakramabahu, the First, became the overlord of the Dhakshina Desha, the enterprising young king wanted to bring the whole island under one rule. He had asked the Treasurer of the Dhakshina Desha, the counterpart of the head of modern treasury in Sri Lanka, whether he had enough resources to wage war against other overlords.

That Treasurer had been an honest man when it came to economic advice unlike those who advise the President today. The Treasurer had opened the Treasury and showed the young king and said that it was empty. Chulavamsa says the king acquired the necessary resources not by taxing people but by boosting international trade by setting up, perhaps the first ever in Lanka, a special export processing zone called the Antharanga Dhura.

This wise counsel was not given to President Gotabaya Rajapaksa by his economic advisors. They would have told him that his Treasury was empty with a Consolidated Fund running at a massive deficit of Rs. 438 billion at end-2019, up from Rs. 304 billion a year ago. Because of the shortfall in revenue due to tax concessions, the shortfall in the Consolidated Fund shot up to Rs. 636 billion in 2020. The Contingency Fund for meeting emergency expenditure programs was just another pittance at Rs. 500 million. The Government had been financing itself on a day-to-day basis by raising a massive overdraft from the two state banks amounting to Rs. 194 billion. In 2020, this also increased to Rs. 463 billion.

These overdrafts were outside the Government's normal borrowing program. Hence, what was necessary was not to offer tax cuts but to increase taxes. The misled Gotabaya Rajapaksa introduced this tax cut to his own peril. The dip in the tax revenue was more than Rs. 500 billion a year. As a result, the tax revenue fell from 12% of GDP to 9% in 2020 and it is continuing at that level since then.

Illogical following of MMT

Then, there was a second error made by his policy advisors. The Central Bank Governor whom he appointed was an academic who had believed throughout his academic career that undertaking expenditure programs through money printing by the Government could deliver miracles to an economy. This was supported by a breakaway group of monetary theorists who proclaimed that they were following an ideology called the Modern Monetary Theory or MMT. Accordingly, money supply was allowed to increase without a break mainly by accommodating the voracious demand for money by the Government.

During the 25-month period beginning from January 2020, the country’s money supply, designated by the Central Bank as M2b, has increased by Rs. 3 trillion or 40%. The main contributor to this phenomenal growth in the money stock was the Government's borrowings from the Central Bank and commercial banks. The net credit which the Government enjoyed from these two sources, that is, after deducting the deposits it was holding with them, amounted to Rs. 4.2 trillion marking an increase of 173%.

Any macroeconomics student would know that this is fertile ground for domestic inflation on one side and depreciation of the exchange rate on the other. Inflation began to pick up and is now rising at 17% according to the latest data released by the Census and Statistics Department. Rupee was falling in the forex markets, but the Central Bank had been keeping it artificially at 230 per dollar giving rise to a lucrative black market at which it is traded with a sizable premium over this rate. Anybody who wants dollars today must patronise this market rather than using the formal channels.

Releasing the rupee from the tight grip

It is now reported that the Central Bank has now stopped holding onto the artificial cap on the dollar at 230 per dollar. As a result, the market quotes have risen above the cap rate to a level of Rs. 240-55 per dollar. This move by the Bank is a good sign but the market clearing rate for the rupee is somewhat higher than this. Once the country reaches that level, the Council should know that the black market in foreign exchange with high premia will automatically disappear. When the black market is subdued, the Council as well as the Central Bank will regain their power to direct the economy. This is because the existence of black or parallel markets reduces the powers of regulators when they seek to direct the economy.

Avoid firefighting at any cost

One of the pitfalls to which the Council might fall is the possibility of spending its time for fire fighting in the economy rather than coming up with a plan to direct the economy toward the goal of prosperity and splendour. This weakness was evident in the case of the National Economic Council set up under the leadership of the former President Maithripala Sirisena. That council was expected to present a medium to long-term economic strategy-plan. Instead, it was continuously handling such micro issues like whether the fertiliser subsidy should be delivered to farmers in the form of a cash grant, or in quantity form.

These are surely not issues to be tackled by an economic council but by the responsible line ministries. In the present case, given the background and the specialty of the ministers serving on the Council, it is very likely that they would spend time resolving these mundane issues rather than presenting a medium to long-term economic strategic plan. This can be avoided if and only if it engages a professional think-tank like IPS as its advisors.

present case, given the background and the specialty of the ministers serving on the Council, it is very likely that they would spend time resolving these mundane issues rather than presenting a medium to long-term economic strategic plan. This can be avoided if and only if it engages a professional think-tank like IPS as its advisors.

Go to IMF

The top priority of the Council should be to make the choice – and it should be done fast – as to whether Sri Lanka should seek assistance from the IMF to get over its present chronic and acute foreign exchange problem. Though the previous Governor and the present Governor have been talking about an alternative economic plan or a home-grown economic plan, there are no details of what those plans should contain. Even the Six-Month Road Map presented by the present Governor in October last year does not provide any clue about this home-grown plan.

Since the Council is to listen to these officials again and again, it is advisable that the Council get outside experts to examine and review the goals of the Road Map to ascertain its workability and efficacy to resolve the country’s forex issue. The former President J.R. Jayewardene did a similar thing when he was advised that the country should seek assistance from the IMF and the World Bank. To convince himself of this strategy, in 1980, JR engaged the reputed Singaporean economist and Deputy Prime Minister Dr. Goh Keng Swee to examine the proposal and report back to him. In a 27-page report, Dr. Goh had recommended to JR that Sri Lanka should seek IMF and the World Bank support to resolve acute problems faced by the country.

There is nothing wrong in getting an outside party to review the Road Map prepared by the Central Bank officials because the Council members deserve to know how far its goals have been achieved. If the goals have been stalling, it could come up with a new road map.

SL hit by double whammy due to Russia-Ukraine war

Sri Lanka has just begun to recover from one of the devastating external shocks that was delivered to it in the form of COVID-19 pandemic. Now, another devastating shock has been delivered by the economic sanctions imposed by the Western world on Russia consequent on its invasion of Ukraine. As a result, energy, gas, and wheat prices have begun to rise in the world markets. Sri Lanka is 100% dependent on imports for these three essential items. In this respect, Sri Lanka is hit by two whammies. One is the non-availability of foreign exchange to import them. The other is the escalation of their costs in the international markets exacerbated by the fall in the value of the rupee.

What this means is that Sri Lanka cannot think of neither prosperity nor splendour in the future. Immediate action should be taken by the Council to prioritise the use of these items by industry so that there will not be a drop in production or foreign exchange earnings. In this respect, the Council should look at the future rather than savouring in the past. As Nishan de Mel of Verité Research has said, Sri Lanka should look through the front windscreen rather than looking at the rear-view mirror. This is the biggest challenge faced by the Economic Council.

The appointment of an Economic Council by President Gotabaya Rajapaksa is a salutary development though it has been done at this late stage. However, since this Council is not made up of professional economists, it is advisable that it engages an economic think tank like IPS to guide it.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected].)