Tuesday Feb 17, 2026

Tuesday Feb 17, 2026

Monday, 22 June 2020 00:00 - - {{hitsCtrl.values.hits}}

“Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist. Madmen in authority who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back.” – John Maynard Keynes

“… the new world of highly integrated economies, global capital markets, shadow banks, instantaneous cross-border global money flows, the rapid evolution of forms of money, technology-enabled changes like fast trading, block chain payments, online lending, virtual digital currencies, insider credit, proliferating new forms of financial securities and highly liquid financial markets in which they trade, and the accelerating expansion of new global financial institutions … (have made) central banking … an institutional anachronism in the 21st century.” – Jack Rasmus, Central Bankers at the End of Their Rope, USA: Clarity Press Inc., 2017.

The Sri Lankan economy, like several other open economies, is crippled, largely and not solely, because of the pandemic. The threat of a second wave of COVID-19 is sending more tremors to an already shocked and shattered world economic leadership.

Sri Lanka also has a military trained president, who in more than one sense fits the description of a control freak. He has extended his control over almost all branches of the country’s administration and governance. His latest is the interference in the supreme financial institution of the country, the Central Bank. Frustrated by the tardiness of the bank’s role in assisting economic recovery of the nation, President GR did not mince his words, when he summoned CB’s governing body and told them that, “monetary policy has to be formulated by the Central Bank in accordance with the economic policy of the President of the country”. What is crucial here are the words, ‘of the President’, and not of the Prime Minister or his cabinet. Of course, there is no legislature even to discuss his policies. Economic policy making has thus become the monopoly of one person.

Therefore, its success or failure should be laid solely at the doors of the president.

Surely, there must be a few ‘defunct’ economists or ‘academic scribblers’ backing the ‘practical’ president, who must have advised him that Central Bank should also be turned into a political tool rather than remain and act as an independent monitor and guardian of the economy. The forced retirement of two members of CB’s Monetary Board, before their term ended, and the appointment of two of President’s favourites indicate that politicisation of that institution has already set in motion.

To be fair by the President, it should be stated that this supreme monetary institution, like its counterparts elsewhere, is a product of a different world and is losing its relevance in a fast changing, highly financialised and tightly integrated global economy, in which money itself has lost is original definition. If one does not know what money is how can one control its supply? This is why it is being called ‘an institutional anachronism’.

Central Bank’s conventional tools of monetary management such as, interest rates, reserve ratio and open market operations have lost their sharpness, and today’s moneyed class has too much influence over governments and banking and credit institutions that it could easily escape Central Banks’ monetary surveillance. This is why there are too many irregularities in the world of banking and finance, and those irregularities and malpractices take their toll on the economy and ultimately on investors and businesses.

|

The multi-ethnic, multi-religious and multi-cultural Sri Lanka is deeply divided, and increased militarisation of the polity and administration under GR’s Presidency is not increasing but decreasing GNH

|

In this context, the three-member committee appointed by the Governor of Central Bank to investigate and report within a couple of weeks on irregularities in financing leasing businesses can only scratch the surface. The malaise is much deeper and needs thorough investigation into the country’s financial sector, by an independent body of experts.

Therefore, President GR has a case when he demands that CB should come out of its monetary conservatism and engage more robustly through a development oriented monetary policy so that he could implement his economic policy. In response, CB has slashed interest rates.

That alone is no guarantee that investment will increase, because what matters for an entrepreneur is not the cost of capital per se but profitability of his/her investment. If the market does not look promising who is going to borrow and invest? Also, if interest rates are slashed that will affect the income of pensioners and elderly, who depend on the return from their deposits with banks and other financial institutions.

Besides, the President has not yet detailed what his economic policies are, except when he said once that he wanted an economy appropriate to Sri Lanka. He has not elaborated on it since then. His ultimate objective however, is to achieve ‘prosperity and splendour’, by creating a ‘secure, disciplined, virtuous and lawful’ society. How he is going to achieve that is nowhere stated.

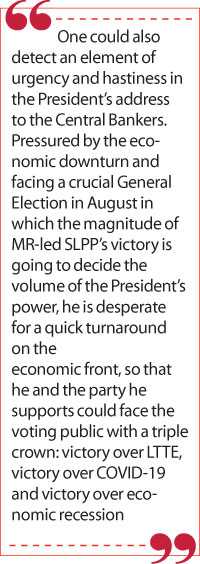

One could also detect an element of urgency and hastiness in the President’s address to the Central Bankers.

Pressured by the economic downturn and facing a crucial General Election in August in which the magnitude of MR-led SLPP’s victory is going to decide the volume of the President’s power, he is desperate for a quick turnaround on the economic front, so that he and the party he supports could face the voting public with a triple crown: victory over LTTE, victory over COVID-19 and victory over economic recession.

The first was solid and comprehensive; second is qualified success, (the fact that the country is an island like New Zealand and Australia is a natural advantage, where the government can shut the borders and stop diseases entering from outside); and the third is illusive and not possible in the immediate short term and certainly not before the election. Sri Lanka’s economic recovery is closely tied to the recovery of world economy, and more importantly with the recovery of the country’s trading partners. They are all facing a dismal future, at least for the next couple of years. However, there are certain areas like food production and small and medium scale consumer industries that can be revived and domestic demand could be satisfied. This is not to create a closed economy, but to gain independence in certain vital economic areas, which could help Sri Lanka to immunise itself from future global economic turbulence.

To achieve that, public peace, democratic freedom and national unity, which are not strictly economic variables, are absolutely essential.

In the final analysis, economic development is for the people and by the people, a fact commonly ignored by economic experts who treat the economy as some sort of an artificial creation run by mathematical models with robotic technology. Without the willing cooperation of the people no economy can survive and thrive. What matters ultimately, is not the growth of Gross National Product (GNP) but Gross National Happiness (GNH).

The multi-ethnic, multi-religious and multi-cultural Sri Lanka is deeply divided, and increased militarisation of the polity and administration under GR’s Presidency is not increasing but decreasing GNH. The Central Bank does not have a magic wand to produce economic miracles.

The crippled economy needs collective effort to recover. That effort will not be forthcoming when communities are trampled under parochial and ultra-nationalistic policies and practices. It is good to dream about ‘prosperity and splendour’, but end should not justify means.

(The writer is attached to the School of Business and Governance, Murdoch University, Western Australia.)