Saturday Feb 21, 2026

Saturday Feb 21, 2026

Monday, 6 June 2022 00:47 - - {{hitsCtrl.values.hits}}

|

|

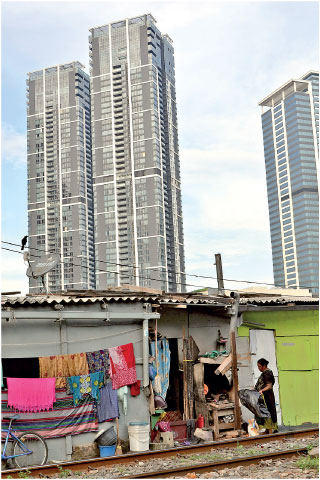

Couldn’t the Government lessen the burden of ‘people who are poorer now’ by collecting a WGT and a WT from ‘people/entities who are richer now’? – Pic by Shehan Gunasekara – |

After giving consistent public warnings that the dire economic circumstances faced by the people of Sri Lanka will get worse in the coming months, the new Prime Minister presented the proposals for tax reforms to be implemented over the immediate and near term (Prime Minister’s Office, Press Release, 2022-05-31). According to news reports (Daily FT, 2022-06-01), the Cabinet has approved the proposals in its entirety, paving the way for enactment by the Parliament.

The Cabinet had no other viable option given the grave situation faced by the Government (and the country). According to the Prime Minister, the Government did not have any other alternative except printing another Rs. 1 trillion just to pay for the committed expenditure. Printing more money, on top of almost Rs. 3 trillion already printed by CBSL since 2019, would have accelerated inflation which is now running at 39.1% (officially) and around 130% (unofficially) a year. The food prices have increased by 57.4% (officially), and about 100% (unofficially) over the last 12 months.

The preamble to the proposals for tax reforms, presented by the Prime Minister tells a grave story: “At present, the situation has aggravated to a very critical level where the General Treasury has to increasingly obtain Central Bank financing (‘money printing’) to make the Government expenditures, including a substantial part of interest, salaries and wages, pensions and Samurdhi payments, etc. This is clearly unsustainable and hence the implementation of a strong fiscal consolidation plan is imperative through revenue enhancement as well as expenditure rationalisation measures in 2022 and beyond to ensure macroeconomic stability to support the medium to long-term economic growth objectives of the country.”

In 2021 the tax revenue of SL dropped to 8.7% of GDP (the average for a low-middle income country being 20%) mainly because of the huge tax cuts granted in December 2019. The Treasury has been losing Rs. 600 billion-Rs. 800 billion a year because of these excessive tax cuts and tax exemptions. The Inland Revenue Department’s total (collected) tax revenues for the years 2020 and 2021 have been just Rs. 523 billion and Rs. 575 billion respectively. It has lost more than 50% of its revenue (Press Release on 2022-05-31, Prime Minister’s Media Division).

The budget deficit in 2021 was 12.2% of GDP. The deficit itself was higher than the total revenue! It is obvious that the shortfall of Government revenue caused by drastic reduction of direct and indirect taxes is one of the main reasons for the huge budget deficit that led to inflationary money printing (FVMP) by the CBSL. The tax reform proposals approved by the Cabinet are not expected to solve the problem fully. However, the proposals, once implemented, are estimated to collect additional Rs. 125 billion during 2022 and thereafter Rs. 292 billion from 2023 onwards (Daily FT, E-Paper, 2022-06-01). Meanwhile, money printing will have to continue to bridge the budget deficit.

Sri Lanka is suffering from a ‘perfect storm’ created by COVID-19, and aggravated by the short-sighted decisions of the Government, and accelerated by the Central Bank and the Treasury. As Sri Lankan and international media have amply demonstrated the folly of these decisions, this article will not revisit them. Moreover, this article will not make any suggestion as to how additional revenue can be raised by the Government by increasing the tax rates, reducing tax thresholds, widening the coverage of existing taxes, and taking unbiased concerted actions to collect unpaid taxes from individuals and entities. The Tax Reform Proposals of the PM and the Treasury have already covered/addressed these to some extent. However, given the social upheaval in SL, wider tax reforms are needed to collect revenue and to deliver social justice to the people.

The two new forms of taxes proposed in this article are a Windfall Gain Tax (WGT) and a Wealth Tax (WT). Several countries in the world are already successfully levying or seriously considering these taxes. Sri Lanka abolished the wealth tax in 1992 and the windfall gain tax is entirely new to the country (https://taxsummaries.pwc.com/sri-lanka). Sri Lanka’s economy and the Government’s coppers are in a much worse condition than these countries and the nation’s desperate demands for social justice are much more profound and loud.

COVID-19 has disrupted economies all over the world including Sri Lanka. However, many countries, including our neighbours, have come out of COVID without much damage to their economies thanks to the prudent decisions of their Governments. However, in Sri Lanka, the economy, society and the political system are in tatters as a direct result of a string of inappropriate decisions made by the Government. The people are now demanding a regime change and a ‘system’ change. The ‘system’ they refer to includes everything. But the main ones highlighted by them are the political, economic, law and order, and education systems.

An important component of a country’s economic system is its taxation system. A taxation system not only collects revenue required for the expenses and investments of the Government, but also serves as a mechanism of redistribution of income and wealth in a socially justifiable manner. Has the SL Government gone far enough in its current proposals to reform the taxation system? Has it utilised the prevailing opportunity for making difficult changes for the benefit of the country? Has it kept up with norms and current trends in the world?

The need and justifications for a Windfall Gain Tax

As the name implies a WGT is based on the ‘super-profits’ of entities and individuals. A WGT is levied by Governments against certain industries, companies/entities when favourable economic or other conditions allow those industries or entities to gain above-average profits. These super-profits are considered as windfall gains (brought by the wind). These super-profits are neither a result of ‘value-adding efforts nor a result of deliberate ‘risk-taking’ on the part of the individual/entities who have profited. In Economics/Finance, gains that are made without exerting efforts or profits that are made without taking risks are ‘unearned’. Taxes on inheritance and lottery winnings can also be considered as windfall taxes. A WGT is a surcharge (surtax) on and above the normal income tax/company tax.

The infamous overnight reduction of import duty on sugar which benefited some ‘unscrupulous’ importers, with or without being privy to ‘insider information’, is a case in point in the context of SL. There may not be a way to legally recover such gains unless there has been fraud. A windfall gain tax would help to recoup some of such windfall gains/abnormal profits from the businesses (entities and individuals) without taking arduous legal actions (which are anyway likely to fail) or tarnishing their names (if they are innocent).

Another example of a windfall gain is when land in a particular area significantly increases due to the actions of the Government (e.g., construction of a major highway or allowing housing projects in an area where such projects had been banned). For example, from 1 July 2023, a WGT will apply to land that has been rezoned by Victoria State Government (Australia) resulting in a value uplift to the land of more than $ 100,000.

The scope of a WGT is much wider than what is apparent from the above examples. A WGT is seen as an ‘efficient and targeted way of capturing’ a fair share of super profits and value increases for the benefit of the community”. It redistributes excess profits of some for the greater social good of all (or selected sections of the community).

The purpose of a WGT is not merely the collection of more income for a Government. In the case of Sri Lanka, collecting more income and reducing the fiscal deficit is also a necessity if the Government is to continue numerous essential services without causing inflation and accumulating more debt (i.e., without printing money or obtaining more loans at excessive interest rates).

As with all taxes there are arguments for and against the WGT. The benefits of a WGT include extra revenue for the Government that can be directly used for funding social programs. As stated before, windfall gains are usually not a result of innovations, extra effort, or efficiency. They are neither the result of genuine risk-taking behaviours of entrepreneurs. Often, they are a result of transfer of income/wealth from other sectors, sections of the society because of extremely favourable economic conditions or Government regulations and subsidies that are favourable to some individuals/businesses.

For example, consider the excessive import duties levied on certain imports to protect domestic products (to promote import substitution industries?). Because of excessive import duties consumers are often compelled to pay higher prices for such products being made locally. Extra taxes charged on windfall profits may encourage the businesses to lower the prices of their products/services and pass the benefit to the consumers as passing the benefit to their customers will be the preferred option. Therefore, it is only fair to collect an extra tax from entities/individuals which have earned excessive/abnormal profits.

Similarly, some companies make excessive profits because of the low or excessive exchange rates, low or excessive interest rates, etc. Some make excessive gains/profits because of sheer luck (e.g., winning a lottery). Therefore, in most cases a windfall tax ‘does not’ hinder the entrepreneurial and risk-taking behaviours of individuals and entities! However, those who are against it keep claiming that windfall taxes will reduce innovations, efforts on minimising waste and inefficiencies, and incentives for taking appropriate risks to earn profits. They also keep arguing that excess profits should be left with the individual/entities to be reinvested to promote innovations/improvements that will benefit the economy and the society.

Financial statements reported by big businesses (particularly banking and financial services, supermarket chains, transport and logistics companies) for the years 2021 and 2022 show remarkable increases in their operating profits and net profits. In some cases, the year-on-year increase is almost 50% and run into billions. For example, this week’s financial press contained reports of several companies which have made multi-billion profits. One financial services company has made a profit before tax of 84 billion.

Would a windfall tax affect investment?

Worthwhile (profitable) Investments (which are likely to earn reasonable returns, measured by Accounting Profit, IRR, NPV, etc.) would continue irrespective of a WGT. The projected returns, by definition, cannot include windfall gains as windfall gains cannot be predicted beforehand.

For example, British Petroleum (BP) has planned to invest £ 18 billion on the UK’s energy system by the end of 2030. After the Government announcement of the WGT, the Chief executive was asked by The Times, on 3 May 2022, which of BP’s planned UK investments would not go ahead if there were a windfall tax. His reply was “there is none that we wouldn’t do.” (https://www.bbc.com/news/business-60295177). Shell Company also plans to invest £ 20-25 billion on UK energy over the next 10 years, irrespective of a WGT.

Wealth tax

A wealth tax (WT) is a tax on a person’s holdings of assets. This includes the total value of personal assets, including cash, bank deposits, real estate, insurance policies and pension plans, ownership of unincorporated businesses, shares and financial securities, and personal trusts. Liabilities are deducted from an individual’s wealth in arriving at the net wealth, hence it is sometimes called a net wealth tax. Some of the countries which had personal wealth tax in 2017 were Switzerland, France, Spain, Netherlands, Italy, Belgium, Norway, Luxembourg, Hungary, Canada, Argentina, and Colombia. Switzerland collected 3.6% of its total tax revenue from wealth tax in 2017. Conceptually, a wealth tax can be charged on an entity’s (e.g., a company’s) net assets too.

In contrast to CGT, which is charged on ‘realised’ capital gains, a wealth tax is applied on the total net wealth. To charge a Capital Gains tax the asset/s need to be sold (disposed). The event/occurrence of sale is not a required precondition for charging a wealth tax.

The need and justifications for a wealth tax

One of the goals of a WT is to reduce the accumulation of disproportionate wealth by individuals. Another aim is to reduce idle capital (e.g., unproductive land). A WT would encourage owners of idle and non-earning assets to dispose of them as there is a cost for holding them. In other words, a wealth tax serves as a negative reinforcer (“use it or lose it”), which incentivises the productive use of assets.

In a widely discussed book entitled ‘Capital in the Twenty-First Century’, French economist Thomas Picketty argues that unequal distribution of wealth (concentration of wealth) causes social and economic instability. He also argues that “inequality is not an accident, but rather a feature of capitalism, and can only be reversed through state interventionism.” He proposes “a system of progressive wealth taxes to help reduce inequality and avoid the trend towards a vast majority of wealth coming under the control of a tiny minority”. He is of the view that unless capitalism is reformed, the very democratic order will be threatened.

The concentration of wealth in Sri Lanka is a problem. In 2020, the top 1% of the people owned 30.7% of the national wealth and earned 20.6% of the national income while the bottom 50% of the people owned just 4.3% of the national wealth and earned only 14.1% of the national income (World Inequality Data Base). Since 2020, the relative and absolute wealth and income of the top 1% of people have obviously increased despite the negative growth of the country and the serious economic problems faced by the ‘average’ person. The steep rises in the share market and the property market (during 2020-21) seem to have further benefited a minority of ‘rich’ people and businesses (Samson Ekanayake, Recent Performance of the Colombo Stock Market, Daily FT, 2021-10-12).

A call for a wealth tax has been gathering momentum across the world. In 2020, a survey found 67% of registered American voters supported a wealth tax on billionaires to reduce inequality. The Social Democratic Party of Germany called for a nationwide wealth tax to be reintroduced in 2019, to bridge the wealth gap between rich and poor in Germany.

There seem to be no Financial Act or enforceable regulations in SL which compel the wealthy individuals to declare their wealth. Members of Parliament are expected to declare their wealth to the Parliament, but most of them habitually avoid doing so. A wealth tax will make it obligatory for all rich individuals (including politicians) to file wealth tax returns annually with the Inland Revenue Department.

Concluding remarks

The literature is abundant with arguments supporting and opposing Windfall gain tax and Wealth tax. In addition to the extreme arguments such as the ‘need to feed the greed’ of the wealthy people to incentivise them to create more wealth, valuation issues and administrative issues also are widely considered as impediments.

As mentioned before, A WGT and a WT will help collect a significant amount of funds for the Government to reduce its budget deficit. These taxes will also help reduce the income and wealth disparity in the country which is bound to cause more social unrest and upheavals. Funds collected can be used to provide extra social security benefits to the underprivileged poor. These taxes will not burden the consumers (unlike the 50% increase in the rate of VAT, from 8% to 12%) and are unlikely to adversely affect the ‘spirit” of businesses and entrepreneurs.

According to the latest poverty indicators published by the Department of Census and Statistics, in 2019, an estimated 3,042,300 individuals (14.3% of the population) lived below the poverty line of Rs. 6,966 (about $ 40 then and $ 20 now) income for a month. A person in poverty is a person who is unable to afford the minimum food requirement (2,030 kcal per day) and other minimum non-food requirements). In other words, 3 million people struggle to afford 3 meals a day! There is no doubt that this number is significantly more now due to the collapse of the SL economy since 2019.

“It is pay-back time even though you are poorer”. This headline of the front-page article in Daily FT on June 1, 2022, aptly captures the irony. The people who are poorer (people below the poverty line and most of the lower-middle and middle-class people) will now have to pay-back in several ways as per the proposed changes to the taxation system, including a 50% increase in VAT. Couldn’t the Government lessen the burden of ‘people who are poorer now’ by collecting a WGT and a WT from ‘people/entities who are richer now’?

The author is a finance professional who values the hugely important, pivotal role of the private sector in creating the wealth of a nation. The fundamental aim of the discipline and practice of finance is to maximise the wealth of the people (owners of capital and businesses) who invest. It is widely accepted that being ‘socially responsible’ helps maximising the wealth of a nation, entity, or an individual. Hence, being socially responsible in business is not contradictory to the aim of wealth maximisation/optimisation ingrained in ‘rational’ entrepreneurs. Successful entrepreneurs are almost always rational individuals. Being socially responsible itself is rational.

(The writer is a former Head of Finance and Financial Planning disciplines of Deakin University, Australia. He has held several senior management positions in academia, commerce, and industry during a career spanning over 40 years. He could be reached via email at [email protected].)

The fundamental aim of the discipline and practice of finance is to maximise the wealth of the people (owners of capital and businesses) who invest. It is widely accepted that being ‘socially responsible’ helps maximising the wealth of a nation, entity, or an individual. Hence, being socially responsible in business is not contradictory to the aim of wealth maximisation/optimisation ingrained in ‘rational’ entrepreneurs. Successful entrepreneurs are almost always rational individuals

The fundamental aim of the discipline and practice of finance is to maximise the wealth of the people (owners of capital and businesses) who invest. It is widely accepted that being ‘socially responsible’ helps maximising the wealth of a nation, entity, or an individual. Hence, being socially responsible in business is not contradictory to the aim of wealth maximisation/optimisation ingrained in ‘rational’ entrepreneurs. Successful entrepreneurs are almost always rational individuals