Thursday Feb 26, 2026

Thursday Feb 26, 2026

Wednesday, 11 November 2020 00:00 - - {{hitsCtrl.values.hits}}

|

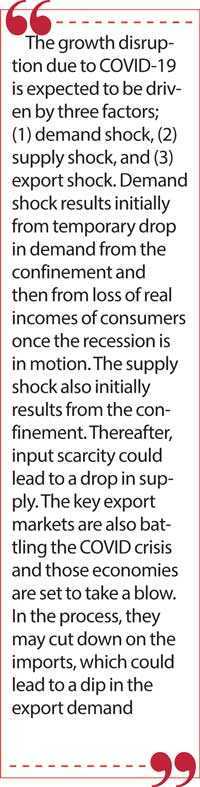

Across the financial sector, several measures have been undertaken to ease the burden on corporate sector businesses and individuals arising from the outbreak and containment measures – Pic by Shehan Gunasekara

|

The corporate sector is a part of the economy made up by companies which include the primary sector – producing raw materials, the secondary sector – manufacturing, and the tertiary sector – trading and services.

It is a subset of the local economy excluding the economic activities of general government, of private households, and of non-profit organisations servicing individuals. The corporate sector has been steering the economy of the country towards the development and better prospects in the international market invariably. As such considering the substantial contribution as the major drive of the economy, the sector has to be reinforced by all means particularly at the strenuous times due to the COVID-19 pandemic.

The global economy is currently encountering its worst recession since the Great Depression of the 1930s. Several advanced economies such as the United States, the United Kingdom, the Eurozone, and Japan will experience contractions during 2020. Other key trading partners of Sri Lanka, including China and India, are also projected to experience a notable slowdown. Across the globe, the World Trade Organization (WTO) forecasts that global merchandise trade can decline by as much as 32% in 2020.

COVID-19 business support – Helping hand in times of trouble

The COVID-19 outbreak is having a huge impact on our lives, families and communities and businesses. The Government’s support schemes are important measures to help businesses, secure jobs and secure Sri Lankan economy during this turbulent period.

Across the financial sector, several measures have been undertaken to ease the burden on corporate sector businesses and individuals arising from the outbreak and containment measures. A wide-ranging debt moratorium has been announced for the tourism, plantation, IT and apparel sectors, related logistics providers and small and medium scale enterprises. These businesses are also to receive working capital loans and investment purpose loans at concessional rates.

Other key initiatives that were undertaken include the introduction of the ‘Saubagya COVID-19 Renaissance Facility’, which provides working capital for adversely affected businesses to revive their activities.

The Central Bank of Sri Lanka surpassed the milestone of Rs. 100 billion loans on 18 August, approving Rs. 100,017 million worth of loans submitted by 36,489 applicants under the above facility. The major State bank, Bank of Ceylon, solely has registered with approximately Rs. 43 billion for affected businesses and individuals island-wide as of 30 September, fulfilling its national duty as the prominent State bank in the country. Out of the disbursed amount approximately Rs. 7.5 billion has been directly pumped to restore the affected corporate segment through the bank’s Corporate and Offshore Banking Division.

Awakening economy before the pandemic

During January-September of 2019, the Sri Lankan economy recorded a subdued growth of 2.6% compared to the growth rate of 3.3% in the corresponding period of 2018. The International Monetary Fund (IMF) expects the real Gross Domestic Product (GDP) growth of Sri Lanka to rebound to 3.5% in 2020 driven by the recovery in the tourism sector.

According to the World Bank, the Sri Lankan economy grew at a rate of 2.7% in FY 18/19 (ended June 2019) indicating Sri Lanka as one of the poorest performing countries in the South Asian region. Bangladesh leads the South Asian region in terms of economic growth by posting 8.1% GDP growth in FY18/19.

Agriculture, forestry and fishing activities registered a moderate growth of 2.1% during Q3 of 2019, compared to the 4.3% growth in the same period of the preceding year.

Industrial activities and service activities also showed soft growth rates of 2.6% and 2.8% during Q3 of 2019 respectively, in comparison to growth rates of 1.8% and 4.4% in the same period of 2018. Growth in industrial activities was primarily driven by the recovery in construction and mining and quarrying activities during the period, while the service sector was largely supported by the expansion in financial services, wholesale and retail trade activities and other personal services activities.

During January-October 2019, a marginal growth of 0.8% was recorded in exports attributing to the growth of industrial exports (accounting for 80% of total exports) which expanded by 2.3% compared to the same period in 2018. Agriculture (-4.4%), Mineral (-6.3%) and all other export segments (-3.6%) recorded negative growth rates during the same period leading to an overall trade deficit in the same period.

|

|

Is the corporate sector of the country at stake?

Yes, indeed. As we commonly struggle to overcome the situation that has arisen with the COVID-19 pandemic, even large stable economies are at stake and our corporate sector has also been victimised due to the bad repercussions of the pandemic. However the most significant factor is the remarkable resilience we have portrayed as a nation, hand in hand with the corporate sector in the economic revival effort.

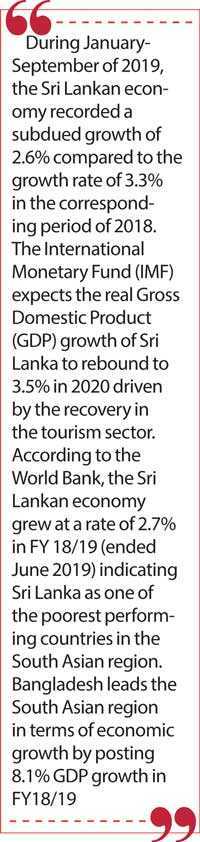

The growth disruption due to COVID-19 is expected to be driven by three factors; (1) demand shock, (2) supply shock, and (3) export shock. Demand shock results initially from temporary drop in demand from the confinement and then from loss of real incomes of consumers once the recession is in motion. The supply shock also initially results from the confinement. Thereafter, input scarcity could lead to a drop in supply. The key export markets are also battling the COVID crisis and those economies are set to take a blow. In the process, they may cut down on the imports, which could lead to a dip in the export demand.

The manufacturing and the export related businesses are the key industries of the industrial sector. It has broadly performed well during 2018/19 amidst the recovery of the agricultural production. The apparel and textile industry which is a major source of foreign exchange revenue relies on the demand coming from the EU and US markets. Furthermore, most manufacturing and export oriented industries largely depend on imported raw materials for their value addition process. A great number of export-oriented and manufacturing industries in Sri Lanka have been, affected due to operational and supply chain disruptions.

The impact on the textile and apparel sector is going to be particularly considerable. This together with the slowdown/cancellation of export orders from the key export markets, would exacerbate the impact on export oriented businesses. Since these industries are largely dependent on the overseas export markets, the recovery of this sector will take relatively longer time as most overseas markets have been adversely affected from the same. The ability of the Sri Lankan economy to recover to a greater degree depends on how soon the trading partners can recover.

Take-off of corporate sector with novel navigation

Diversification of production and exploring diversified markets

The Sri Lankan corporate sector has to be optimistic in exploring beyond its traditional export markets. Exports to the American and Eurozone have accounted for over half of Sri Lankan total exports, backed by favourable entrance to some extent including GSP concessions, low tariff, etc. However through the lessons of the pandemic situation, Sri Lanka should gradually shift its focus towards exporting to emerging Asia and other non-traditional markets.

In addition to the diversification of merchandise exports, the corporate sector needs to focus on further improving services exports. In addition to the already earmarked services sectors such as tourism and IT-BPO, measures should also be taken to improve exports of other important services such as logistics and financial services. The sector can be enriched with more foreign exchange once the Colombo Commercial and Financial Hub is in operation. It is vital that Sri Lanka needs to form strategic economic partnerships with other nations, particularly the regional countries, to promote its exports and maximise benefits from the movement of capital and human resources.

Reformation of business environment and relaxation of rigid policy frameworks

It is admitted that a well-developed and relaxed policy framework of a country underpinned by a conducive environment to conduct business enables the corporate sector to move ahead in terms of attracting investments, thereby boosting overall performance. As all of us are aware that investors’ perspective is of paramount importance for corporate business to thrive. As such establishing a promising and relaxed business environment to attract enormous investment is nothing left to discuss, but to be well-established.

As per Doing Business 2020, Sri Lanka holds the 99th position out of 190 economies for Ease of Doing Business, remaining below its regional peers. India managed to raise its ranking through streamlining its reform strategies giving priority to the Doing Business indicators. Countries like Vietnam have upgraded their information technology infrastructure to make it easy to pay taxes.

Recently Sri Lanka too made a few efforts to upgrade information technology infrastructure by introducing online systems for filing taxes, processing constructions permits and business registration. The relatively poor score of Sri Lanka on the Ease of Doing Business indicates that there is an ample room for further improvement as a host country for investments for the corporate sector.

Untapped areas yet rewarding

Sri Lanka’s merchandise export strategy needs to be revolutionised by diversifying to the differential exports and among them, IT export, which is currently less tapped as other evolving markets like Bangladesh, Vietnam in the Asian region have been benefited more from IT exports to the economic development of their respective countries.

The garment trade that began in Bangladesh in the 1970s is now a $ 30 billion industry. But the economy is diversifying. The services sector – including microfinance and computing – makes up 53% of the country’s GDP.

The success of the IT industry is central to the digital transformation and ongoing economic growth of Bangladesh. It exports nearly $ 1 billion of technology products every year – a figure that the Government expects to increase to $ 5 billion by 2021. The country also has 600,000 IT freelancers.

It is worth noting that exports and FDI have been key drivers of growth in many successful economies in Asia. However, Sri Lanka’s progress in terms of exports and FDI has been lower compared to its regional counterparts. Sri Lanka has not been able to diversify exports and its share in global trade has declined over time, unlike its East Asian neighbours, and its exports structure has not evolved to the next level beyond apparel, tea and rubber products since the early 1990s. Anti-export bias, lack of private domestic and foreign investment in the tradable, particularly industry sector, lack of innovation and research and development (R&D) have further deepened the woes of the export sector.

Commercialisation of agriculture and investment opportunities in related activities

This sector neglected at corporate level for many years which should be promoted as commercialised agriculture in order to face challenges in restriction of imports of agricultural items, generate new employment opportunities and changing mindset of the upper level of the urban people to use local agricultural products.

Way forward: Commercialising agriculture

Establish agriculture banks with soft loan schemes. Commercial banks are not capable enough to cater to agricultural needs

Construction of warehousing facilities

Provisions of irrigation facilities

Promotion of commercialised culture

Emulation of modern agriculture facilities

Coordinating of institution like irrigation and water resource, agriculture, agriculture banks and marketing agents and Government policy changes, bureaucracy

Constraints in commercialisation of agriculture

The lack of corporate investment due to uncertain policy limits of the expansion of the sector

Frequently every year, natural disasters such as floods, droughts, wild animals challenges. Such natural events and disasters can be devastated to farmers and their families

The biggest impediment to agriculture development is not at policy level, the Government comes up with sustainable policies.

The weak functioning of research and development programs which are confined to labs and do not adequately reach the purposes

The participation of farmer organisations and the private sector in agriculture development are essential for equity based development

Reforms are needed to transform of traditional agriculture to commercial agriculture to face global

challenge

The potential development of the corporate sector could be optimised when there is a genuinely symbiotic relationship between the Government’s initiatives and the contribution of the players in corporate sector.

The corporate sector has its responsibility and accountability to assure the end use of funds and the effective approaches to attain the ultimate results of the business plan and such approaches should also be recognised that there is a large amount of developmental activities that companies have undertaken as part of their core operations: the Government needs to recognise the same and harness the segment.

As the backbone of the economy, the corporate sector needs to be reinforced by all means with the objective of optimising the real gain to the economy. As such considering the above factors, robust strategies are required to be put in place, enriched in a coordinated, coherent and strategic manner.

[The writer is currently steering the Corporate and Offshore Banking Division of Bank of Ceylon as the Deputy General Manager (Corporate and Offshore Banking). He is a senior banker with three decades of experience in both local and international banking arenas. Surawimala holds a Bachelor’s (Special) Degree in Public Administration and Master of Science (M.Sc) in Management specialising in Banking and Finance, both from the University of Sri Jayewardenepura, Sri Lanka. He is an Associate Member of the Institute of Bankers of Sri Lanka.]