Sunday Feb 15, 2026

Sunday Feb 15, 2026

Monday, 10 January 2022 00:00 - - {{hitsCtrl.values.hits}}

It is in the best interest of the country and its citizens for the Government to defer payment on its debt and use its limited foreign reserves to ensure uninterrupted supply of essential imports

The available foreign reserves of the country can be used to either repay foreign creditors or to finance imports of essential goods and services required by its citizens. This is the dilemma facing Sri Lanka today. Repaying the full value of the bond using the limited foreign reserves available would provide a windfall gain to those currently holding these bonds. But it will be at great cost to the citizens of the country who will face shortages of essentials like food, medicine, and fuel.

The available foreign reserves of the country can be used to either repay foreign creditors or to finance imports of essential goods and services required by its citizens. This is the dilemma facing Sri Lanka today. Repaying the full value of the bond using the limited foreign reserves available would provide a windfall gain to those currently holding these bonds. But it will be at great cost to the citizens of the country who will face shortages of essentials like food, medicine, and fuel.

In these circumstances, it is in the best interest of all its citizens, for the Government to defer payment of the $ 500 million International Sovereign Bond (ISB) coming due on 18 January 2022, until the economy can fully recover and rebuild.

Just as an individual with co-morbidities is more vulnerable to develop severe illness if infected with COVID-19 and more likely to require hospitalisation and even treatment in an ICU, Sri Lanka was vulnerable to economic shocks long before COVID-19 struck. The country was already facing several macroeconomic challenges. Muted economic growth. An untenable fiscal position.

Although a tough consolidation program was put in place to bring Government finances to a more sustainable path, sweeping tax changes implemented at the end of 2019 reversed this process, with adverse consequences to Government revenue collection. Weak external sector due to high foreign debt repayments and inadequate foreign reserves to service these debts. COVID-19 only exacerbated these macroeconomic challenges. And like a patient who gets over the worst of COVID-19 has a long road to recovery; the economy of Sri Lanka faces many challenges to get back on track.

The onset of COVID-19 in early 2020, only worsened an already grim macroeconomic situation. The country lost the confidence of international markets, and the ability of the sovereign to rollover its external debt became difficult if not impossible. In these circumstances, there was a solid argument for a sovereign debt restructuring. But the response from the Government and the Central Bank of Sri Lanka (CBSL) was a firm “No”.

The argument was that Sri Lanka never defaulted on its debt and it was not going to do so now. The official position was also that the Government had a ‘plan’ to repay its debt and hence there was no reason to engage in a debt restructuring exercise. However, Sri Lanka faced high debt sustainability risks: the debt to GDP ratio at 110% was one of the highest historically and interest payments to Government revenue at over 70% was one of the highest in the world.

Fast forward to 2022. The country’s foreign reserves declined to $ 3.1 billion. Usable reserves are much lower. CBSL has sold over $ 200 million of the country’s gold reserves to meet its debt obligations. In the first week of 2022, CBSL announced further swap facilities and its commitment to repay the International Sovereign Bond (ISB) of $ 500 million due in January. According to statistics from the Central Bank, in addition to the ISB payment, there are pre-determined outflows from foreign reserves amounting to $ 1.3 billion in the first two months of 2022.

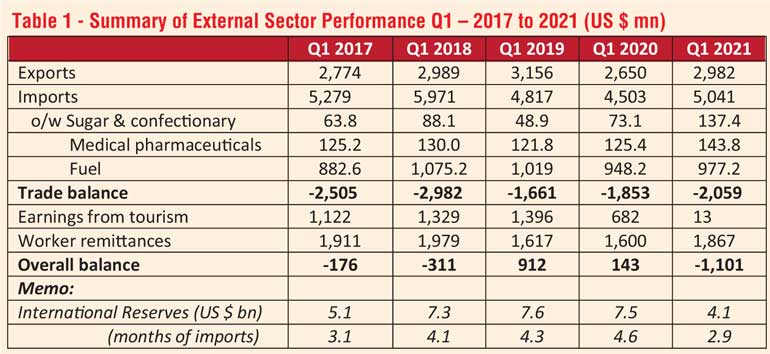

Further, based on trade data for the last five years, the country on average has a trade deficit of around $ 2 billion to finance during the first quarter of the year (see Table 1). With expected inflows from tourism under threat with the onset of the Omicron variant and continuing decline in worker remittances, financing this external current account deficit will add further pressure on available foreign reserves. India which accounted for around 20% of recent tourist arrivals is now requiring returnees to the country to quarantine. This will likely further dampen tourist arrivals.

In this context, the country faces a trade-off between using its limited foreign reserves to repay its debt or utilising it to finance essential imports. $ 500 million is sufficient to finance imports of fuel for five months; or pharmaceuticals for one year; or dairy products for one and a half years; or fertiliser for two years.

Therefore, it is in the best interest of the country and its citizens for the Government to defer payment on its debt and use its limited foreign reserves to ensure uninterrupted supply of essential imports. But this requires a plan. To minimise the cost to the economy, the Government must immediately engage its creditors in a debt restructuring exercise. This will require a debt sustainability analysis (DSA) by a credible agency to identify the resources required for debt relief and the economic adjustment needed to put the country back on a sustainable path. This will be critical to bring creditors to the negotiating table and provide them comfort that the country is able and willing to repay its debt obligations in the future.

The cost of not restructuring is much higher. A non-negotiated default (if and when the country runs out of options to service its debt) would lead to a greater loss of output, loss of access to financing or high cost of future borrowing for the sovereign. It could even spill over to the domestic banking sector, triggering a banking or financial crisis.

The consequences are clear. What will we choose?

(Dr. Roshan Perera is a Senior Research Fellow at the Advocata Institute and the former Director of the Central Bank of Sri Lanka. Dr. Sarath Rajapatirana is the Chair of the Academic Programme at Advocata Institute and the former Economic Adviser at the World Bank. He was the Director and the main author of the 1987 World Development Report on Trade and Industrialisation. The Advocata Institute is an Independent Public Policy Think Tank. Learn more about Advocata’s work at www.advocata.org.)