Monday Feb 16, 2026

Monday Feb 16, 2026

Monday, 28 September 2020 00:30 - - {{hitsCtrl.values.hits}}

Once open banking is fully in operation, banks can share credit information among themselves. It would obviate the necessity for having a third-party bureau like CRIB to collect, collate and supply credit information to member institutions

CRIB at the receiving end

The Credit Information Bureau of Sri Lanka, known more popularly in its acronym CRIB, has become the villain in the eyes of bank borrowers, politicians and media today. Bank borrowers dislike CRIB and  would be more comfortable if it is abolished. In their view, CRIB has become a stumbling block when they seek loan facilities from banks. Politicians dislike CRIB because they come under the influence of the lobbying groups that want it dismantled.

would be more comfortable if it is abolished. In their view, CRIB has become a stumbling block when they seek loan facilities from banks. Politicians dislike CRIB because they come under the influence of the lobbying groups that want it dismantled.

Media have sought to augment their readership or viewership by creating sensational stories about CRIB’s operations. Yet, when CRIB was declared open in a soft opening in August 1990, the then Prime Minister and Minister of Finance, D.B. Wijetunga, expressed confidence that it would continue to serve both banks and good borrowers. Banks by providing them with timely information to assess loan applications. Good borrowers by speeding up loan processing work in banks. Wijetunga did not mention about bad borrowers but it was well understood that they had to go through a hurdle before they became eligible for loans. That hurdle was to become good borrowers first by settling their outstanding loans to banks. In a nutshell, CRIB has helped banks to screen loan applicants and give priority to those good borrowers in their assessments. Naturally, bad borrowers should develop a grumble about the work of CRIB.

I will argue in this article that CRIB is necessary right now but would be redundant once Sri Lanka goes for open banking.

CRIB has multiple meanings

The acronym CRIB has a double meaning, according to the man who coined it, Central Bank’s Deputy Governor Dr. S.T.G. Fernando who became the first Chairman of the Bureau. One meaning was the sleeping cot of a baby and it connoted a safe place for growth. The other was copying without authority, known as plagiarism. This second meaning, according to Fernando, will put CRIB on alert: copy information but do it with authority. What Fernando meant by authority was not the legal powers which CRIB had got from Parliament. It was the other meaning of authority, expertness, which CRIB had to demonstrate when it handled credit data in its hand.

CRIB was just a pointer and should be friend of politicians

CRIB was never intended to be a stumbling block for borrowers. Instead, it sought to fill an information gap between lending institutions and borrowers. Borrowers knew everything about themselves, but the lending institutions knew only what the borrowers had disclosed to them. This is known as asymmetry in information. Taking advantage of this information asymmetry, borrowers would disclose only what is favourable to them. It is to their advantage to hide information that would go against them.

Hence, information on their past borrowing records, especially those relating to default of loans, would not be disclosed to the lending bank when they apply for a loan. But, to assess the credit risk of the borrower, the lending bank should know this information. To get it from other banks is also not effective since banks normally do not disclose that information to their rival banks. In these circumstances, bad borrowers were used to shifting from bank to bank and defaulting all loans in the process. When this happens regularly, banks would end up with loans that are not paid back, a situation known as the existence of non-performing loans.

When the non-performing loan portfolio is high in the entire banking industry, the stability of the industry is at high stakes. When banks fail, they have to be rescued by governments to protect the depositors and ensure the continuation of the financial system. Hence, it is in the interests of politicians to keep the financial system stable and CRIB is one institution that helps them to achieve that objective. Therefore, all good-minded politicians should regard CRIB as a friend rather than an enemy.

Operation of CRIB

CRIB collects information on all borrowers – good as well as bad – from its member institutions. Borrowers here are defined to include those who have borrowed for themselves as well as those who have guaranteed loans for others to borrow. In the case of companies, in addition to the name of the company, the names of the directors of the company are also reported. These data are then collated and stored in its computers for release to member banks.

When a member of public, say Punchi Singho, goes to a bank for a loan, it is now customary for the bank to check with CRIB on Punchi Singho’s borrowing history from all banks. CRIB reports back whether Punchi Singho was a regular borrower (good borrower) or an irregular borrower (bad  borrower).

borrower).

Regular borrowers are those who have been repaying their loans on time without running into arrears. Irregular borrowers are those who have not paid back their loan instalments for three months or more. Regular or good borrowers go through the loan processing speedily like those passengers with all the necessary documents could pass the immigration counters at an airport without a hurdle. In contrast, irregular or bad borrowers have to wait before a decision on their loan applications is made known.

Defaults can happen due to many reasons

CRIB does not make this distinction, but a borrower could have become bad due to several reasons. In the first place, they could be wilful defaulters who have borrowed from banks with the sole objective of defaulting the loans. They are the ones on whom a lending bank should have a close watch. Then, there could be borrowers who have become bad not because of their intention but because of compelling circumstances beyond their control.

This could happen due to global changes, loss of markets, natural calamities, and epidemics or pandemics of global proportions. For instance, the COVID-19 pandemic which crippled the entire global economy has beaten Sri Lanka’s businesses very badly. Some examples of very badly beaten industries are the travel, hospitality and export industries. Without a regular cash inflow into the business, these firms have become unwitting defaulters. CRIB does not flag them on this count, and it is the duty of the lending banks to do so.

Thirdly, there are those second or third-party defaulters. They are those who have guaranteed loans for others who have defaulted their loans, on one side, and those who serve as non-executive directors in companies which have defaulted their loans, on the other. When a loan application is entertained from any one of them, it is necessary for lending banks to consider them with a different flag attached to them. Perhaps, a different colour code can be used from light red to mild red to hot red to denote the level of risk involved.

Of late, CRIB has introduced a credit score system

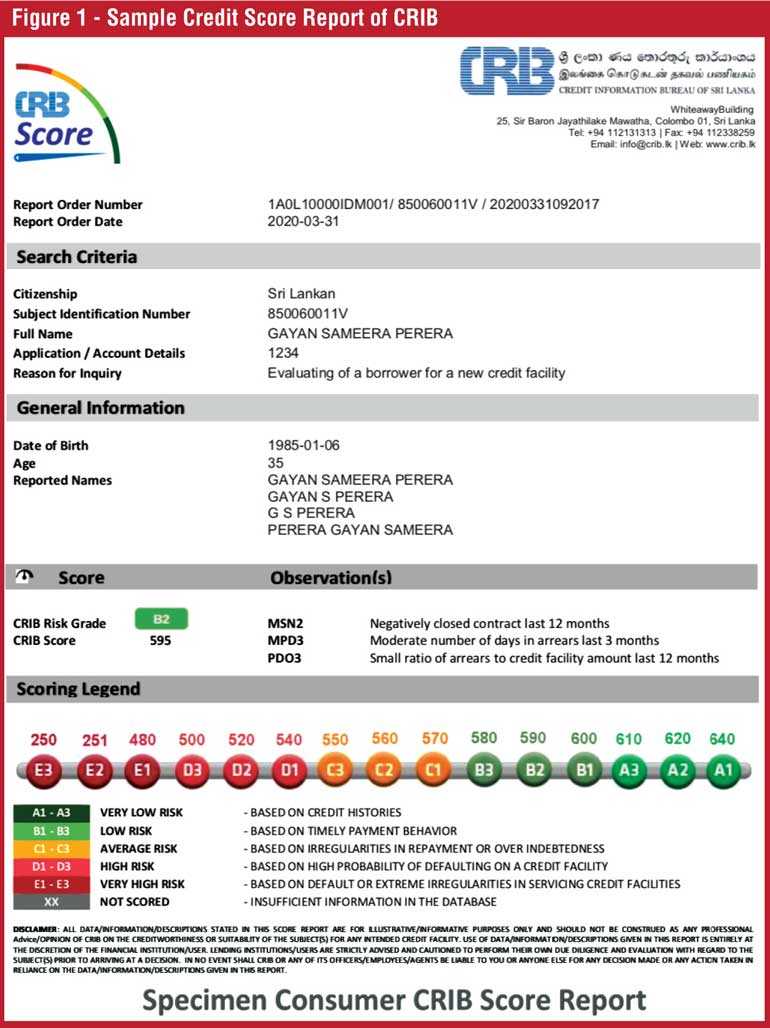

Since banks and other financial institutions have not been able to do it with consensus, CRIB has stepped into flagging the borrowers. But this it has done after 30 years of its existence. Beginning from 2020, CRIB has started to work out a credit score for each borrower in its data base. When member banks ask for credit information, they are also supplied with a credit score that gives a rating grade flagged with colour codes. The colour code ‘grey’ has been used to denote non-scored borrowers. The others are categorised into five risk categories, very high, high, average, low and very low risk.

A sample credit risk score report for a hypothetical borrower is provided in Figure 1. The calculation of the credit score is a machine exercise that uses a built-in algorithm for the purpose. It uses for its calculation the past performance of a borrower under different permutations and combinations. This algorithmic calculation is accurate based on the data fed to the system. As a result, borrowers who are dissatisfied with the score assigned to them should take it up with his bank and see whether there have been errors in reporting. If there are, once they are corrected, the credit score too changes automatically.

High risk borrowers should be charged a high-risk premium

Does it mean that those who have got a credit score of C1 or less should be denied a loan facility. Not at all. The credit score reported to banks gives them some background information to put their loan applicants into different buckets and deal with them accordingly. If it is a good lending bank, the applicants who have got a score depicting average risk to high risks should be further investigated to ascertain whether they have been habitual defaulters or those who have just become defaulters due to factors beyond their control.

Once this ascertainment is made, the lending bank should offer a higher lending rate to such borrowers to take care of the risks involved. For instance, the best customers of banks, categorised as prime customers, are given loans at relatively low interest rates. At present, in Sri Lanka’s banking system, these customers are offered loans at average interest rates between 6 and 7%. A margin could be added to this depending on the colour code which a prospective borrower has been assigned by CRIB. Thus, credit risk is tackled not by denying a loan to a customer but by getting him to pay more for his loan. It gives him an incentive to improve his credit record as well.

CRIB in a high-tech era

CRIB was created at a time when the technology used in banks was not so advanced as it is today. At that time, internet or email was unknown and the first credit report was issued by CRIB in 1990 by using the latest communication technology available at that time, namely, the fax machine now in disuse (available at: https://www.colombotelegraph.com/index.php/crib-at-25-brings-new-challenges/ ). At that time, banks had just been venturing into digital banking and their entry to the full digital world commenced as late as the end of the last century.

According to the Australian futurist Bret King, banks have since then gone through four stages of digital banking: between 1998-2002, Digital Bank 1.0 involving E-banking, between 2003-8, Digital Bank 2.0 with multichannel integration, between 2009-15, Digital Bank 3.0 using omnichannel and since 2015, Digital Bank 4.0 taking advantage of Internet of Everything. His argument was that banks have been blessed with a massive data base about their customers and they should not just sit on them without using them for the benefit of the industry.

Open banking is the future of banking

These data bases, also known as big data, help an individual bank to profit from sharing them among different branches within a bank. For instance, the behaviour of the savings account customers, known only to those in the savings account department, will be helpful for the new product teams to design new products and marketing teams to promote the same. But it is a single entity use and it dissuades competition and innovation, a must for the sustained existence of the financial services industry. Thus, governments in many countries have forced banks to share such information among themselves in an initiative known as ‘open banking’. This is a more recent development that has started from around 2015 in the Digital Bank 4.0 era.

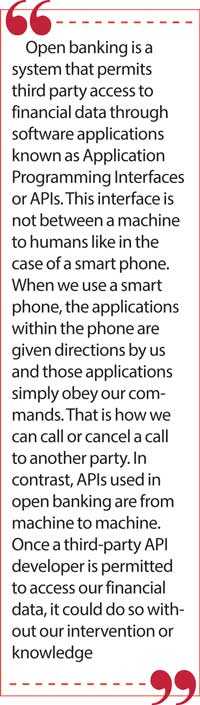

Third-party API developers

Open banking is a system that permits third party access to financial data through software applications known as Application Programming Interfaces or APIs. This interface is not between a machine to humans like in the case of a smart phone. When we use a smart phone, the applications within the phone are given directions by us and those applications simply obey our commands. That is how we can call or cancel a call to another party. In contrast, APIs used in open banking are from machine to machine. Once a third-party API developer is permitted to access our financial data, it could do so without our intervention or knowledge.

Similar APIs are in our smart phones too. When the camera roll is permitted to download photos and videos sent to us through WhatsApp, and Google Photos or OneDrive Photos are permitted to download those photos or videos from the camera roll, it happens automatically using the limited data quota given to us by our internet service provider under different packages. That is why some smart phone users find that their data quota is consumed too quickly though they have not done it by themselves. The solution to this is simply to disable the access and through that action, we prove that we are the masters of smart phones.

Early entrants to open banking

Open banking has already been introduced to the European Union and the United Kingdom. Beyond these countries, the others which have already introduced open banking or in the process of introducing the same are as follows: Australia, Canada, Hong Kong, Japan, Israel, Mexico, New Zealand and Singapore (available at: https://bbvaopen4u.com/en/actualidad/open-banking-beyond-europes-borders). Recently, India too has shown interest in introducing open banking to its financial system.

In an open banking era, CRIB becomes unnecessary

Once open banking is fully in operation, banks can share credit information among themselves. It would obviate the necessity for having a third-party bureau like CRIB to collect, collate and supply credit information to member institutions. Since credit information should be used by banks when assessing the credit risks of their potential customers, the information sharing work will continue whether there is a CRIB or not. But until such time, CRIB cannot be dismantled.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, was the founding General Manager of CRIB. He can be reached at [email protected].)