Monday Feb 16, 2026

Monday Feb 16, 2026

Friday, 2 September 2016 00:01 - - {{hitsCtrl.values.hits}}

Housing sector development and reform

Housing sector development and reform

The housing sector is a strong catalyst of growth and prosperity of any country. However, rapid urbanisation, increasing cost of construction and high land prices have made decent housing a far-reaching goal for many.

The average amount spent on housing, household equipment, maintenance, water, gas, electricity, etc., across all households, has increased sharply in the last 10 years from 15% of the households’ total consumption expenditure to over 17.5%. (CBSL Annual Reports 2004-2014). Across all non-food expenditure, housing cost represents 19.1% of households’ monthly expenditure. (Income & Expenditure Survey 2011/12)

Nevertheless, Sri Lanka has been successful in managing the national housing shortfall compared to our regional counterparts, due to the several initiatives commenced by late President Premadasa in 1978. Additionally, financial sector reforms and development which commenced in 1977, further fuelled this achievement to the present high. As a result, almost 99% of the households have either owned or rented or encroached housing of diverse quality standards.

New policy focus

The next phase of the national housing agenda should facilitate people realising the dream of quality and decent housing that meet the changing lifestyle needs in a growing economy. According to the Census of 2012, it is only 82.9% of households living in owned housing and 16% of households are occupying rented/leased, rent free or encroached housing. These households are dreaming of owning a home and upgrading their housing conditions.

Meanwhile there are over 900,000 units in excess of overall housing requirements in the country. In the Western Province, an estimated 15% of houses are excess or vacant housing. Investment housing market is rising and becoming one of the main driver of the housing sector, particularly in the Western Province. Investment housing fuels land prices and cost of construction materials noticeably.

The growing investment housing market mounts the pressure of housing stress among the below average income earning families, particularly those engaging in informal economic activities. While facilitating low income housing, the Government should play an enabling role for the rest of the people in realising their housing dream in the changing lifestyle environment. A well-focused housing finance system can fuel this transformation while underpinning inclusive growth in the economy.

Significance of housing in the economy.

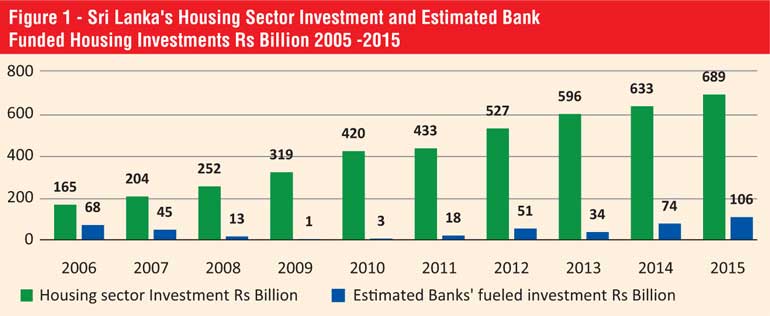

As per the Central Bank records, housing sector capital investment and housing related services drive about 18% of the country’s GDP at market price. Over the last four years, Sri Lanka has spent around Rs. 600 billion per annum on residential capital investment, which alone has driven about 6.7% of the GDP. Households’ savings, informal borrowings, microfinance and direct Government investments have financed almost 90% of this investment and estimated the banking system’s contribution is only 10% (Figure 1).

Enhancement of the bank-fuelled housing investment by formulating appropriate growth supportive policy can leverage the housing sector largely whilst contributing towards more inclusive development in the economy. A well-functioning housing finance system supports savings and provincial resources mobilisation and alleviates inequality in income distribution while improving people’s living standards.

Meanwhile, housing related services such as furnishing, household equipment and routine maintenance of housing, gas, electricity and other fuel, etc. drive about 11.30% of GDP at market price. These housing related services account for around 17% of total consumption expenditure.

Housing finance system in the country

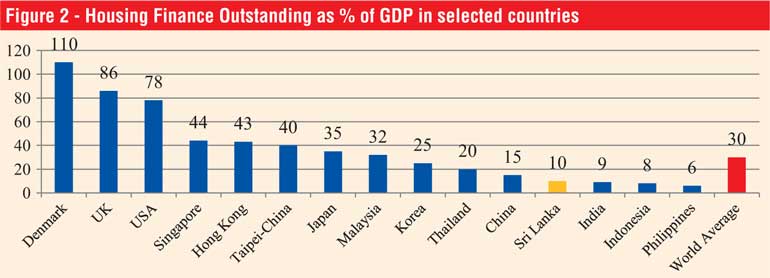

The formal housing finance system has followed organic growth over the last 30 years and present estimation is about Rs. 517 billion represents around 10% of the country’s GDP. Housing finance outstanding to GDP world average is about 30% as tabulated.

Mortgage outstanding to GDP ratio in Thailand is 20%, Korea 25%, Singapore 44% and USA 78%. (Figure-2). This mirrors the vast potential for the banking system participation in housing sector development, assisting every family to own a decent house and economic growth and prosperity.

The housing finance market has maintained an annual average growth of 15% over the last 10 years. Housing loan outstanding in the commercial banking sector is Rs. 370 billion and that of specialised banking sector is around Rs. 147 billion as at 2015.

While ‘average income families and above’ are well served by the commercial banking sector with diversified product ranges available at bargained interest rates, the ‘lower average income housing finance industry’ that is mainly driven by the licensed specialised banks, faces a great challenge of maintaining affordability and sustainability as an industry, swayed by associated higher risk profiles.

Lack of proper and adequate collateral, income proof documents, affordable long-term funding and rigid regulatory controls are the key constraints in the growth of the lower and middle income housing finance sector.

In this market, customers are mainly from the informal economic sectors flourishing from the increasing activities in a growing economy. Their affordability for market finance funded loan products is narrow. This emerging market will represent the largest share of the potential housing finance market of the country in the next two decades.

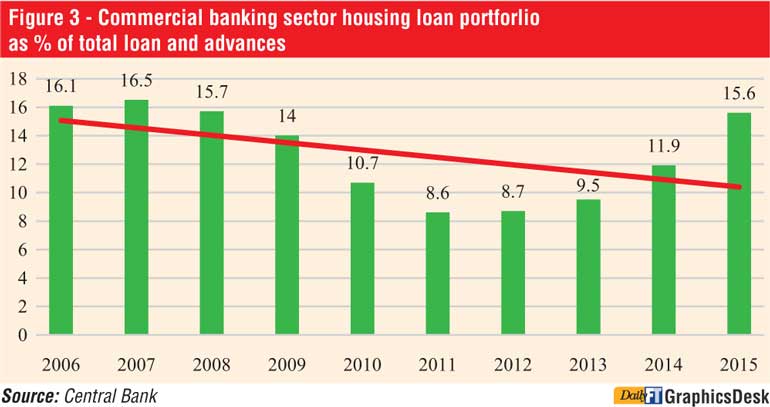

Housing finance has accounted for 15.6% of loan book of the commercial banking sector as at 2015, which has escalated substantially from the recorded last 10 years’ lowest level of 8.6% in 2011. Over the last 10 years market analysis reveals that the commercial banking sector too has not executed constant focus on housing finance influenced by the long-term funding constraint and interest rate mismatches. (Figure-3).

Housing finance policy

In the next phase of housing sector development, a broad-based housing finance policy could play a vital role. The policy should focus both on supply and demand side of housing finance. Governments since 1978 have implemented several demand supportive policies but supply side supportive policies have been neglected

Lack of long-term matching funds at market competitive interest rates is one of the main impediments for housing finance industry growth. Long-term capital funds is prerequisite for maintaining affordability of housing finance. In housing finance, tenure extension is the widely-applied strategy of leveraging affordability of housing cost within the disposable income of the customers in a sharp escalating cost environment. But financing customers for long-term with market available short-term capital funds affects stability not only of the lending institution but also of financial system in broad.

The country’s long-term capital sources such as EPF and ETF funds and life insurance funds should mainly focus on long-term investments such as infrastructure development and housing. Presently over 85% of these funds are invested in Government securities and most of them are with short maturities. The country’s housing finance policy should be focused for effective utilisation of these long-term funds to drive the system constantly and sustainably while stimulating the housing sector as a strong catalyst of economic growth and prosperity.

(The writer, MBA, BSc, FCA, FCMA, is Chief Finance Officer of HDFC Bank of Sri Lanka. The sources of estimates and figures in this article unless otherwise mentioned are as per the industry research and analysis of the author and the views here do not necessarily represent that of HDFC Bank of Sri Lanka.)