Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Monday, 7 November 2016 00:05 - - {{hitsCtrl.values.hits}}

COPE recommendation: Investigate EPF fully

The COPE report on the bond scam in the Central Bank from February 2015 to May 2016 has come up with, among others things, a very strong recommendation relating to EPF.

It has recommended in both the main report and the dissenting report with footnotes that the activities of EPF from around 2010 until May 2016 should be fully investigated to ascertain irregularities in investments, improprieties, malpractices and losses to members.

EPF’s buying at high prices in the secondary market

The focus of the main report has been on an observation by the Auditor General that EPF, overlooking its duty to buy government bonds from the primary market at a price beneficial to its members, has bought such bonds on a number of occasions from the secondary market at higher prices.

The implication has been the failure to earn the maximum income for members since the primary market price of those securities had been pretty much lower than the price at which it had bought them in the secondary market.

The implication has been the failure to earn the maximum income for members since the primary market price of those securities had been pretty much lower than the price at which it had bought them in the secondary market.

In fact, the leaked onsite examination report of the Central Bank on the primary dealer Perpetual Treasuries had documented one such instance that had taken place in January 2016.

Revelation by the leaked onsite examination report

This is what the leaked onsite examination report has said: “Analysis of the capital gains by PTL [Perpetual Treasuries Limited] through dealings with EPF during the month of January 2016 it was observed that PTL has sold LKB02541A016 Bond, purchased at the primary auctions held on 08.01.2016 (settlement date 11.01.2016) and from Pan Asia Banking Corporation PLC on the settlement date of the auction at a substantially lower yield to EPF within 14 days from the auction date. We may recommend the Monetary Board to inquire the rational (sic) for EPF to purchase the security from the secondary market within a short period of time after the primary auction when the EPF has the ability to bid at the Primary Auction.”

EPF being a collaborator of pumping and dumping

The reference here is to a 25 year Treasury bond maturing on 1 January 2041. The Central Bank web says that this bond carries a fixed or coupon interest rate of 12% p a.

According to the table given in the onsite examination report, PTL has bought this bond at an average price of Rs. 98 and sold to EPF within 14 days at an average price of Rs. 111.

But subsequently, according to the data published by the Central Bank, the selling price of this bond in the secondary market had fallen continuously. Within a week, it had fallen to Rs. 108, within a month to Rs. 101 and within two months, to the level at which PTL had bought it at the primary auction. Since then, its market price has remained at that level and but by end October, the price had fallen to Rs. 97.

Obviously, PTL has made a massive capital gain out of this transaction. However, with the declining market prices, EPF continues to make capital losses and as at end October, 2016, its capital loss has been more than the capital gain of PTL since the bond’s market price is now slightly below the primary auction price.

Obviously, PTL has made a massive capital gain out of this transaction. However, with the declining market prices, EPF continues to make capital losses and as at end October, 2016, its capital loss has been more than the capital gain of PTL since the bond’s market price is now slightly below the primary auction price.

If the same price will prevail at the end of the year, marking the EPF portfolio to market price as required by accounting standards would result in a substantial capital loss which the Monetary Board would not be able to explain.

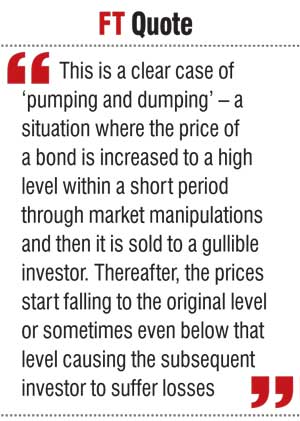

This is a clear case of ‘pumping and dumping’ – a situation where the price of a bond is increased to a high level within a short period through market manipulations and then it is sold to a gullible investor. Thereafter, the prices start falling to the original level or sometimes even below that level causing the subsequent investor to suffer losses.

Hence, the investment rationale of the EPF’s front office in this particular transaction needs to be fully investigated.

Unanimity in both the main COPE report and the dissenting report

Footnotes 26 and 29 in the COPE report, approved only by 9 dissenting members of UNP, have reopened the need for inquiring into EPF’s investment strategy as well as practices in the past.

Footnote 26 refers to an observation of the Auditor General in his report relating to the first bond scam of February 2015 as reproduced in the main COPE report.

An English rendering of the reproduction reads as follows: “While bids had been called for Rs. 1 billion [by the Central Bank], it is very abnormal on the part of Perpetual Treasuries to submit bids amounting to Rs. 15 billion, 15 times of the amount on offer, by submitting bids for Rs. 2 billion directly and a further Rs. 13 billion through Bank of Ceylon.”

The dissenting group has not refuted this observation. But it has added further flavour to it by bringing the possible involvement of EPF in the scam. The relevant footnote, translated into English, reads as follows: “Perpetual Treasuries has earned this huge profit by selling the bonds, purchased in the primary market, in the secondary market. It is the opinion of the Committee that investigations should be conducted to ascertain the complicity of state owned funds like EPF in helping them to make such a huge profit and if so, the rationale behind such investment decisions. It is necessary to examine why EPF which could buy these bonds in the primary market did buy them in the secondary market.”

This suspicion of the dissenting group has been confirmed in the leaked onsite examination report, as mentioned above, with respect to EPF’s investments in 2016. The dissenting group has suggested that the examination of EPF activities should be taken backward to cover even the first bond scam.

Dissenting report: investigate EPF from 2010

Footnote 29 also pertains to an observation made by Auditor General in his report as reproduced in the main COPE report.

The relevant observation had remarked that EPF which could buy bonds in the primary market had earned financial losses by buying them in the secondary market at a higher price. This has led to a questionable investment practice, according to the Auditor General, since EPF is under the management of the Monetary Board of the Central Bank.

The dissenting group has not refuted this observation of the Auditor General since they themselves had presented it previously in footnote No. 26. They have strengthened it by remarking that EPF has made such imprudent investments during the last six-year period.

The issue for the dissenting group is the apparent repetition of this practice even today. Hence, they have argued in the footnote that, since EPF has been holding the savings of the country’s workers, made in terms of law, for their old age security, special provisions should be made regarding the safe and prudent investment of EPF funds.

During 2010-13, says the footnote, criticisms had been made by some members of COPE about these imprudent investments made by EPF. Hence, the footnote recommends that “it is the view of the Committee that these investments should also be examined.”

Need for appointing a special select committee of Parliament

Thus, both the main report and the dissenting report have made a single recommendation with respect to EPF. That is, the investment practices adopted by EPF since 2010 should be fully investigated. Since EPF comes under purview of the Committee on Public Accounts or COPA and not COPE, if it is done through the existing Parliamentary Committee System, this task devolves to COPA.

However, COPA is already overburdened with a massive amount of work involving Government departments and ministries. Hence, if it is to be examined by Parliament, it is necessary to appoint a special select committee suitably assisted by experienced investment analysts.

Freaky EPF organisational structure

EPF was placed under the care of the Monetary Board of the Central Bank in 1958 when the Fund was established, despite mounting objections for doing so. These objections were from within as well as from outside the Central Bank.

Sir Arthur Ranasinghe, Governor of the Bank at that time, mentions in his autobiography, Memories and Musings, that he informed Premier S.W.R.D Bandaranaike that the Central Bank could not undertake this function because it involved a conflict of interest. Then, one time Governor of the Bank, N.U. Jayawardena, and then a Senator, made a plea to the Government that it should not reduce the Central Bank to the status of a Government department by assigning jobs which the Central Bank could not do.

But the Government overruled all these objections and created a freaky organisational structure for EPF which could not be found in any part of the world. The freaky structure was the creation of a dual responsibility system for EPF.

In this system, the enforcement of the EPF Act was assigned to the Commissioner of Labour, a department in the Central Government, and the management and the custodianship of the fund to the Central Bank, the country’s monetary authority that was required to decide on the country’s interest rate policy free from any conflicting interests.

The explanation given by the Prime Minister was that he could not find any other Government body to which the responsibility of managing the fund safely could be assigned. In fact, according to reports, he had promised his own Senator, N.U. Jayawardena, that that was only a temporary arrangement and could be changed shortly. That temporary arrangement has now become a permanent arrangement and EPF has come to stay within the Central Bank as a permanent resident.

Monetary Board’s difficult task

Hence, the Monetary Board had to perform a difficult task in terms of the new resident it had been forced to accept.

On one side, it has to adopt monetary policy without being influenced by any interest it holds in the system. This was the reason for introducing specific provisions in the Monetary Law Act that the Board should not own any private business or bank or a financial institution.

On the other, it has to generate the highest rate of return for members of EPF. Hence, when investments are made for EPF, the Monetary Board had to necessarily ignore this statutory restriction placed on it.

This was not an issue in 1958 because at that time, the only available investment was the government securities. But today, there is a vibrant share market, corporate bond and debenture market and commercial paper market outside the government securities market. Investment in these ventures obviously entailed a conflict of interest.

Self-restraints imposed on itself by the Monetary Board

To overcome this problem, the Monetary Board took a number of actions when it performed its statutory duty for EPF.

It created a Chinese wall between its monetary policy and EPF investment policy. When it invested in private companies, it imposed a self-restraint on itself. One restriction was that EPF would not invest in the company shares more than 5% of their issued share capital so that it would not participate in the management of those companies. Hence, it was only to be a passive investor. The other was that EPF would not buy shares of any financial institution supervised by the Monetary Board.

The reason was that the Monetary Board had access to inside information in those financial institutions and if it invested in them, it would give a wrong signal to other market participants.

For instance, if EPF invested in a financial institution, the market would make the wrong judgment that it did so by referring to inside information which was not available to other investors. Similarly, if EPF exited any financial institution, that too would give the wrong signal in the opposite way. That is, EPF did so because it knew of some adverse development taking place in that particular financial institution.

Furthermore, the Board did not want another regulator, namely, the Securities and Exchange Commission, to accuse it one day that it did its investments because it had inside information relating to those financial institutions.

Nationalising private banks through EPF

These sacred rules were broken by the Monetary Board after 2010 by investing more than 5% of shares in private companies and choosing banks and financial institutions for investment up to the maximum amount permissible so that it could manage those institutions.

Accordingly, by using other public sector funds like ETF and Insurance Corporation, the Monetary Board has collaborated with the then Government to effectively nationalise private banks and financial institutions.

Thus, the Monetary Board, together with the Ministry of Finance, commenced managing leading private banks, appointing directors and nominating chairpersons. This was against the Monetary Board’s governance principles as well as its statutory obligations. This is a matter which should be fully investigated to ascertain why the Board decided to break its own rules and venture into running banks in the country.

This writer in a previous article in this series, published immediately after the new Yahapalana Government was formed, advised it that EPF should exit private banks promptly and allow them to manage their affairs by themselves (available at: http://www.ft.lk/article/387913/EPF-should-exit-banking-sector-and-Central-Bank-should-leave-private-banks-in-private-hands).

But what the new Yahapalana Government did was to appoint their own representatives to those positions after unseating those who had been appointed by the previous Government.

EPF should exit private banks immediately

Hence, while investigating the investments made by EPF after 2010, immediate action should be taken for EPF to exit the financial sector promptly.

(W.A. Wijewardena, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected]). `