Tuesday Feb 17, 2026

Tuesday Feb 17, 2026

Monday, 19 December 2016 08:46 - - {{hitsCtrl.values.hits}}

Prime Minister wants a more independent Central Bank

Prime Minister Ranil Wickremesinghe, in the economic policy statement he presented to Parliament in November 2015, pledged that his Government would ‘make structural changes in the Central Bank’ enabling it to ‘engage in their work in a more independent manner’. This was a solemn promise. But the Budget speech delivered by his Minister of Finance two weeks later did not mention a word about the Government’s wish to restructure the Central Bank.

The second economic policy statement delivered by the PM almost one year later in October 2016 too kept a mum about the promise that had been made in 2015. The Budget 2017, presented in Parliament in November, too was silent on this aspect of restructuring the Central Bank, though there were many proposals in the Budget falling within the legitimate functions assigned to the Central Bank by Parliament.

The independent analysts, including this writer, saw it as an attempt by the Ministry of Finance to encroach what has been the functions of the Central Bank, assigned to it by law, and thereby erode its independence (available at: http://www.ft.lk/article/580074/Budget-2017:-Significant-improvement-if-not-marred-by-policy-inconsistencies-and-interference-with-the-Monetary-Board).

Harsh tone of the Minister of Finance: An indication of plans to erode Central Bank independence?

In this backdrop, the Minister of Finance is reported to have announced at a public forum on the Budget 2017 that the Central Bank would be restructured to ensure better execution of its responsibilities (available at: http://www.ft.lk/article/580366/Central-Bank-to-undergo-restructuring--Ravi-K).

According to the Minister, ‘The Central Bank has failed miserably on many fronts’ because the bank has deviated from its responsibilities under the law and allowed itself to be politicised. In his view, the Central Bank should confine itself only to its regulatory and monitoring functions without ‘dabbling in how to run the country’.

Many activities done by the Central Bank are undesirable and by implication, they have impeded the action taken by the government to put the economy in the right footing. Hence, along with the restructuring the Central Bank, all other pertinent legislations like the Banking Act and the Payments and Settlement Act would also be ‘revolutionised’. The Minister, without giving further details, has elaborated that the restructuring process would be spearheaded by both the President and the Prime Minister, implying that it is an action initiated by the very top of the Government.

The tone of the Minister implied that the Government was to reduce the independence of the Central Bank and make it another department in the Ministry of Finance. If done, this would be a disaster and would go against the accepted principles of central banking. The loser at the end would be the Government and the people of the country.

‘Legal Eye’ takes issue with the Minister of Finance

A reader writing under the penname Legal Eye had taken issue with the Finance Minister’s claim that the bank has failed on many counts on the ground that it is not an institution coming within the purview of the Ministry of Finance but under the Minister of Economic Affairs of which the portfolio is held by the Prime Minister (available at: http://www.ft.lk/article/581362/Finance-Minister-s-statement-that--Central-Bank-has-failed-miserably-on-many-fronts-). Hence, by implication, the initiative for restructuring the Bank should come from the Minister who is in charge of the Central Bank.

With respect to the allegation that the Central Bank has been politicised, the Legal Eye had quoted an instance where the bank has obviously been guided by political considerations during the reign of the current administration. Hence, if the Minister of Finance has a genuine interest in an apolitical Central Bank, it would not just be an exercise in which the bank is depoliticised of the previous government elements and repoliticised with the new government elements.

That is not what society expects of a central bank; it desires to have a central bank free from political interferences with respect to its key functions, namely, conducting monetary policy to sustain price stability and regulating the banking system to ensure its stability.

Eternal battle between politicians and central banks

However, there is a continuing battle between central banks and political authorities with regard to how central banks should behave in their respective countries. The latest such battle has come to light in the case of the US Federal Reserve Bank. In this case, the President-elect Donald Trump has vowed to fire the Fed Chairperson Janet Yellen because her interest rate policy goes counter to his plan for stimulating the economy with low interest rates (available at: http://qz.com/860763/janet-yellens-plan-to-raise-interest-rates-wednesday-may-re-ignite-trumps-feud-with-the-fed-chair/).

The Trump victory has started to reflate the US economy with all promises of stimulating packages and big government expenditure programmes. When the system gets hotter and the US will have to sacrifice its long term sustainable growth, it is the responsibility of Janet Yellen to put measures to cool it down. But those measures are not admired by politicians who just want to go for only short term objectives. Elsewhere in the world, in Russia, President Vladimir Putin and in Turkey, Recep Tayyip Erdogan, have been noted for bullying their central banks for lowering interest rates when economic realities have been suggesting the opposite.

In India, a few months ago, the independent monetary policy taken by Governor Raghuram Rajan provoked a government party senior politician to question Rajan’s loyalty to India which led to an abrupt termination of his career as a central banker. Hence, true central bankers are not popular among the politicians and Sri Lanka is not an exception.

PM need not reinvent the wheel to reform the Central Bank

On many counts, the Central Bank of Sri Lanka has to be reformed today. In fact, that reform initiative was started during 2000-4 when the bank went through its modernisation phase. A new Central Banking Act was drafted, with technical assistance from IMF, replacing the old Monetary Law Act which had several features that did not go along with modern central banking practices.

The Government of Prime Minister Ranil Wickremesinghe which was in power at that time had accepted that the proposed Central Banking Act should be enacted; not only that, the government had agreed to introduce a new Banking Act too replacing the old Banking Act. There too, IMF supported Sri Lanka to draft a new Banking Act. However, these two legislations could not be enacted since Parliament was dissolved in mid-2004 calling for a general election. At that election, a new government was voted to power. The new government did not think that it was necessary to implement central banking and the banking sector reforms. Accordingly, the two draft legislations were shelved and maybe still dusting at the Central Bank’s archives. Hence, if the Prime Minister and the Finance Minister are interested in reforming the Central Bank and the banking sector, all what they have to do is to retrieve those two draft legislations and update them to reflect the current thinking on the subject.

Global evidence says that independent central banks are better placed to sustain price stability

The Prime Minister has expressed the desire to make the Central Bank independent in his first economic policy statement. It is a laudable goal since that is what society expects of a central bank. Evidence from the rest of the world has shown that when a central bank is independent in its policy making, it is more strongly poised to attain its objective of price stability, the desire of the community.

When a central bank is independent, it can discipline itself by avoiding overprinting of money, the main causal factor for self-feeding high inflation. It could also take timely action to tighten monetary policy by way of increases in interest rates if the money and credit situation is far above what is desired by a well-balanced economy. When people realise that the central bank would take necessary action to curtail inflation without being influenced by those in power, it builds confidence among people in central banks’ action which in turn contribute to lower inflation expectations, a must for long term price stability, as argued by MIT cum IMF economist Stanley Fischer in a recent lecture titled ‘Central Bank Independence’ (available at: https://www.federalreserve.gov/newsevents/speech/fischer20151104a.htm).

The best example is provided by Bank of England, according to Fischer, which was made independent in 1998. In the UK, inflation fell below 2% per annum after independence for making monetary policy was granted to the Bank of England. A similar experience has been encountered by both Australia and New Zealand after the reserve banks in the respective countries were made independent in early 1990s.

The Israel born economist Alex Cukierman, in a paper he published in 2008 in European Journal of Political Economy under the title ‘Central Bank Independence and Monetary Policy Making Institutions: Past, Present and Future’, has remarked that the central bank independence has contributed to price stability in both developing and developed countries. Sri Lanka’s good governance government should not ignore these good global experiences.

Central Bank becoming subservient to the Ministry of Finance in the past should not be used as a precedent

The Central Bank of Sri Lanka has been criticised in the past on the ground that it is subservient to the Ministry of Finance. As such, though it had independence in deciding on monetary policy, critics had charged that its policies had in reality been dictated by top officials in the Ministry of Finance. This has been made possible by the presence of the Secretary to the Ministry of Finance on the Monetary Board, the policy deciding body of the Central Bank, with voting powers.

John Exter, the architect of the present Central Bank, had clarified in the report he submitted to the government on the establishment of a central bank in Ceylon, known as the Exter Report, why this arrangement had been made in the structure of the Central Bank. According to him, it will allow a better coordination between the government and the Central Bank with respect to policy by permitting the Minister to make his views known to the Board through the Secretary to the Ministry of Finance (p 13).

However, he made a qualification that its effectiveness depended on the maturity and experience of the people occupying the high positions in government and in the Central Bank. Thus, the Secretary to the Ministry of Finance was expected to function as a conduit between the Minister and the Monetary Board and not as a super-official steamrolling over its decisions.

But over the years, Exter was defeated by some of the officials who had occupied the topmost position in the Ministry paving the way for critics to justify their charge of having a subservient Central Bank. Hence, any move to make the Central Bank independent should re-examine whether the Secretary to the Ministry of Finance should continue to be a vote-carrying member of the governing board of the Bank.

Hard choice but essential if the country is to become a rich nation within a generation

This is a hard choice which the Government has to make today. It will be difficult for a minister of finance to make up his mind to give full independence to a central bank since he desires to exercise control over it. Yet, an independent central bank would help him to attain long term economic growth by stabilising prices and maintaining macroeconomic stability. Any control over the central bank by the minister is therefore tantamount to sacrificing long term economic growth.

But the goal of the Prime Minister, as presented in the economic policy statements of 2015 and 2016, is to elevate Sri Lanka to the status of a rich country within a single generation. This would require the country to attain, as remarked by the Prime Minister in the second economic policy statement, an average annual economic growth of more than 7% over the next 30 year period.

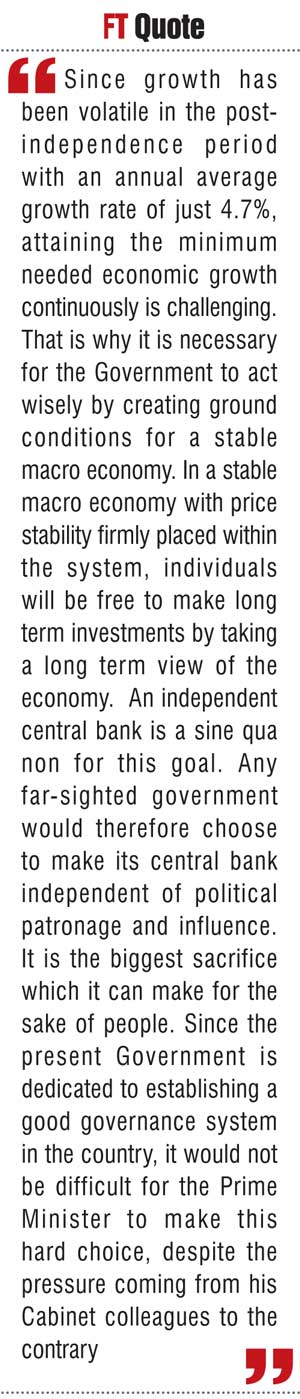

Since growth has been volatile in the post-independence period with an annual average growth rate of just 4.7%, attaining the minimum needed economic growth continuously is challenging. That is why it is necessary for the Government to act wisely by creating ground conditions for a stable macro economy. In a stable macro economy with price stability firmly placed within the system, individuals will be free to make long term investments by taking a long term view of the economy. An independent central bank is a sine qua non for this goal.

A far-sighted approach is a must

Any far-sighted government would therefore choose to make its central bank independent of political patronage and influence. It is the biggest sacrifice which it can make for the sake of people. Since the present Government is dedicated to establishing a good governance system in the country, it would not be difficult for the Prime Minister to make this hard choice, despite the pressure coming from his Cabinet colleagues to the contrary.

(W.A. Wijewardena, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected].)