Wednesday May 06, 2026

Wednesday May 06, 2026

Wednesday, 11 May 2016 00:00 - - {{hitsCtrl.values.hits}}

The Budget 2016 is still on the news for variety of positive and negative aspects. Among the proposals to revive the economic condition of Sri Lanka, the proposals on capital markets are of utmost importance due to its sensitive correspondence with the economic performance of the country.

The proposal to establish a bond clearing house is of significant importance which is not spotlighted among much discussed topics. The Government aims to set up a bond clearing house primarily targeting Government securities with the expectation of expanding into other instruments such as corporate debt securities.

The proposal resembles a move towards a Central Counter party system, although the possibility exists that it may form in to a different institutional setup. The Central Bank of Sri Lanka (CBSL) in its 2013 report, captioned ‘Public Debt Management in Sri Lanka, Performance 2013 & Strategies for 2014 and beyond,’ mentioned the intention of CBSL to set up an e-trading platform and Central Counterparty arrangement by the end of 2015.

In another development it was reported that Colombo Stock Exchange (CSE) has called for a Request for Information (RFI) from suppliers with a proven international track record to implement a CCP system. The system which integrates all secondary market transactions in CSE is expected to be initiated during early 2017.

What is a Central Counterparty system?

In general terms, the market participants themselves, of any market, are the counterparties for any possible transaction. For instance consider Bank A purchases a certain number of shares of ABC Company in the secondary market. The seller is Mr. B. Then the counterparties are Bank A and Mr. B. Mr. B should have the confidence that the bank will properly settle the due payment on correct time. The counterparty credit risk and liquidity risk is a fact that is prevalent throughout in this process.

Central Counterparty is an intermediary institution which interposes between counterparties becoming a buyer to every seller and seller to every buyer. The process looks the same as the current prevailing process in Sri Lanka. However, by contrast to the existing process, the CCP guarantees the settlement for counterparties, eliminating counterparty risk and settlement risk for market participants.

In general terms, CCPs are incorporated as separate entities, affiliated to current market regulatory institution with full ownership or majority ownership resting with the current regulatory institution.

Why a CCP system is important

Central Counterparty system can be designated as a market infrastructure institution which guarantees a level playing field for every market participant, irrespective of their size and influence. It is a mechanism with global recognition to alleviation of Counterparty credit risk, liquidity risk and settlement risk, fostering financial system stability.

In the presence of CCP, market participants are released from the burden of worrying on Counterparty exposures, strength and ability of other parties to honour the transaction, effect on non-payment or settlement on the liquidity position of the organisation, etc.

CCP mechanism is recommended and guided through stringent recommendations by the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO) together with Bank for International Settlement (BIS).

From a Sri Lankan viewpoint, it is vital as the initiative will drive the CSE to be aligned with the top stock markets in the world. The compatibility with world standards will encourage foreign investors to invest in Sri Lankan markets. At present CSE is using Automated Trading System (ATS) for trading and Central Depository System (CDS) for Clearing and Settlement functions.

In the current scenario for equity transactions, the delivery phase will take effect immediately upon execution of the trade whereas the payment take effect after three market days (T+3 basis). Under CCP system, delivery vs. payment basis will be applied and securities and funds will be exchanged simultaneously eliminating risk factors of the current system.

The Indian perspective

India, one of the fastest growing economies in the world, has a vast financial industry with a highly-regulated market infrastructure. The market capitalisation of the Bombay Stock Exchange (BSE) is $ 1,580 billion (68.4% of Indian GDP) with 3,000 odd companies listed. Hence the mechanisms such as CCP are well established and tested in Indian markets.

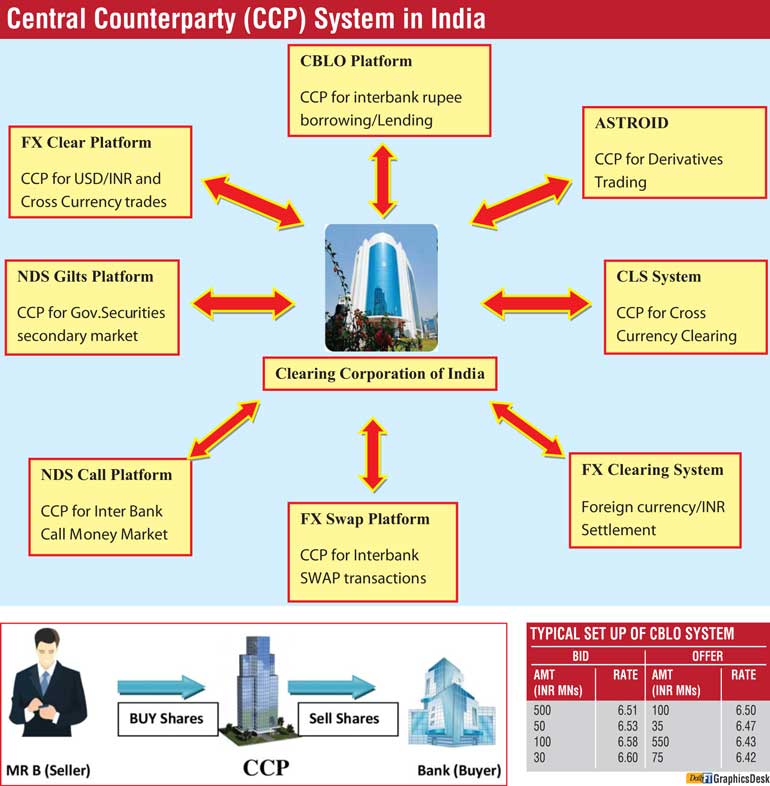

Indian capital market regulator, the Securities and Exchange Board of India (SEBI), has named three institutions as qualifying CCPs. They are National Securities Clearing Company Ltd., Indian Clearing Co Ltd. and MCX-SX Clearing Co Ltd. Apart from the capital markets, Reserve Bank of India (RBI) has recognised Clearing Corporation of India Ltd. (CCIL) as a Central Counter Party.

CCIL provides a classic example for the extent of diversification feasible to a CCP. Established in April 2001, CCIL is the institution facilitating guaranteed clearing and settlement functions for transactions in money, government securities, foreign exchange and derivative markets. CCIL has contributed significantly to enhance efficiency, transparency, liquidity and risk management in the financial markets with much focus on inter-bank transactions.

CCIL acts as an intermediary, guaranteeing clearing and settlement trades in the inter-bank market and government securities secondary market. In this endeavour CCIL has introduced a variety of platforms to facilitate electronic execution of trades. There are six major platforms, namely Collateralised Lending Borrowing Obligation (CBLO), FX Clear, FX SWAPS, NDS Gilts, NDS Call and ASTROID.

CBLO is an infrastructure facilitating interbank borrowing and lending up to a maximum period of one year. It is an anonymous order matching system. (Banks can enter the funds they are able to lend and they required to borrow, to CBLO system. Names of the banks will not appear. The values will appear on best rate order where amounts with same rate will be as a one block.

The borrower or lender can click on the preferred block change the amount to suit their requirement and confirm the trade.) Trades will be executed in Straight Through Processing (STP) mechanism and net of lending and borrowing amounts will be adjusted from the counterparty bank’s account maintained at Reserve Bank of India.

The FX Clear platform of CCIL facilitates Inter-Bank foreign currency transactions in USD/INR and other major currency pairs such as EUR/USD, USD/JPY, GBP/USD, etc. This platform offers two modes of transactions which are order matching mode and negotiated mode.

The settlement aspect of the foreign currency is undertaken by CCIL via its CLS system (system established with CLS Bank; CLS is a specialist US financial institution that provides settlement services to its members in the foreign exchange market) and its local forex clearing system.

NDS (Negotiated Dealing System) Gilts system and NDS Call system facilitates transactions of Government securities of Secondary market and Inter-Bank Call money transactions. FX SWAP system facilitates USD/INR currency SWAP transactions between banks. It is a transparent and anonymous medium for trading which comes as an exception for traditional broker driven market. The derivatives trading platform of CCIL is called as ASTROID. At present it facilitates rupee denominated interest rate SWAPS to banks and primary dealers.

CCP – A no risk alternative

CCP mechanism significantly eliminates the risk factors faced by market participants. However due to the same fact, CCP develops an inherent risk in its set up. CCPs lead to concentration of risks in markets which must be cautiously monitored and appropriately addressed by regulators. Bank for International Settlement (BIS) in their consultative report published on March 2004 put forward the risk factors and recommendations for risk mitigations for CCPs.

Further the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO) on their 2012 publication, ‘The Principles for Financial Market Infrastructure,’ recommended rigorous stress testing for CCPs under different extreme scenarios, to determine financial resources they need to uphold to manage credit and liquidity risks. Due to increased sensitivity of CCP’s exposure, IOSCO initiated a stress testing review process for CCPs in March 2015.

A successful project to establish a Central Counterparty system in Sri Lanka, will be a landmark achievement in the history of financial industry of the country. The Indian financial infrastructure can set a worthy precedent for the developments of regulatory and operational framework for CCP establishment in Sri Lanka. However, it is vital to place proper risk management measures, aiming CCP arrangements, to foster sound and healthy financial environment in Sri Lankan capital market.

(The writer is a Banker and an Associate member of Institute of Bankers, currently based in Chennai Branch of Sri Lankan bank. He can be reached via [email protected].)