Saturday Feb 21, 2026

Saturday Feb 21, 2026

Tuesday, 13 February 2024 00:53 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

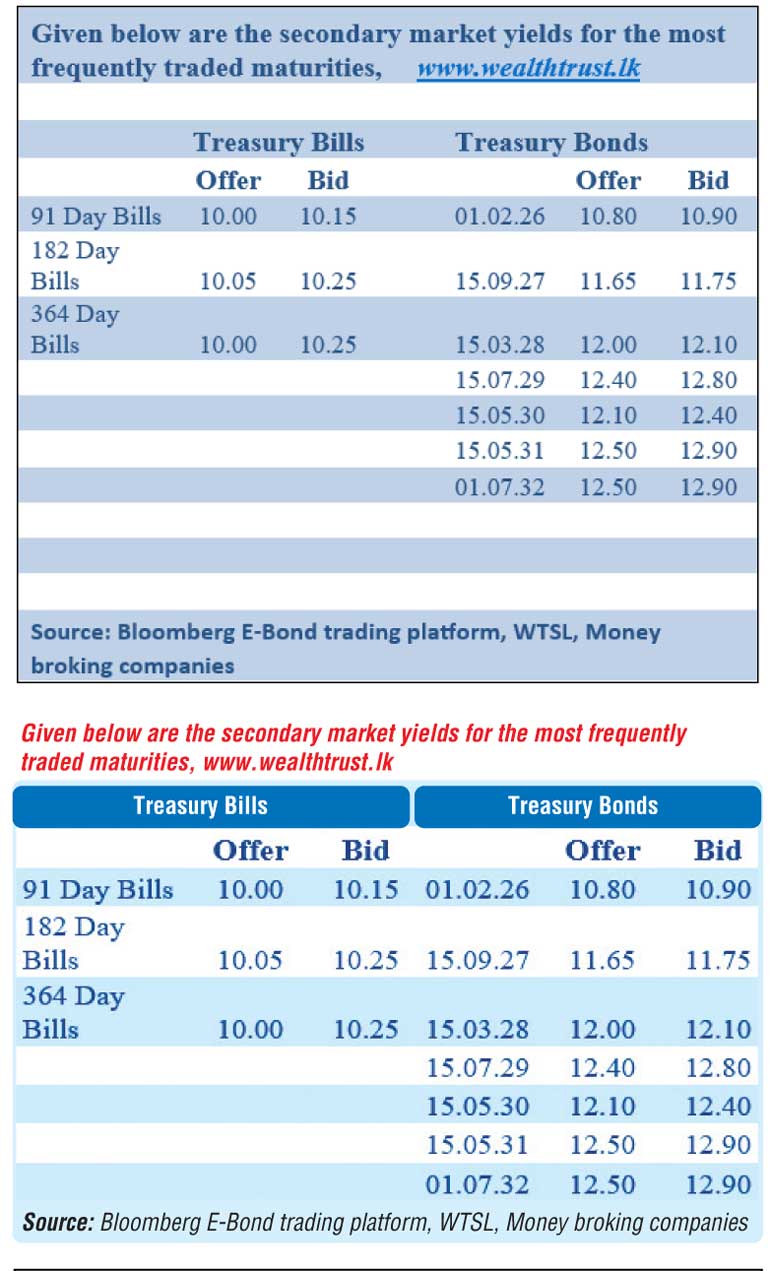

The secondary bond market commenced the week with a moderation in activity and volumes traded while yields held broadly steady, in comparison to last week. This is ahead of today’s Treasury bond auctions. However, some concentrated interest on selected 2025 durations saw yields dip down with considerable volumes transacted. Trading continued to be predominantly on the short end of the yield curve. Trades were observed on the maturities of the 2025’s (01.06.25 and 01.07.25), 2026’s (01.02.26, 15.12.26), 15.09.27, 01.07.28 and 15.05.30 within the ranges of 11.00% and 10.55%, 11.00% to 10.85%, 11.78% to 11.70% and 12.35% to 12.26% respectively.

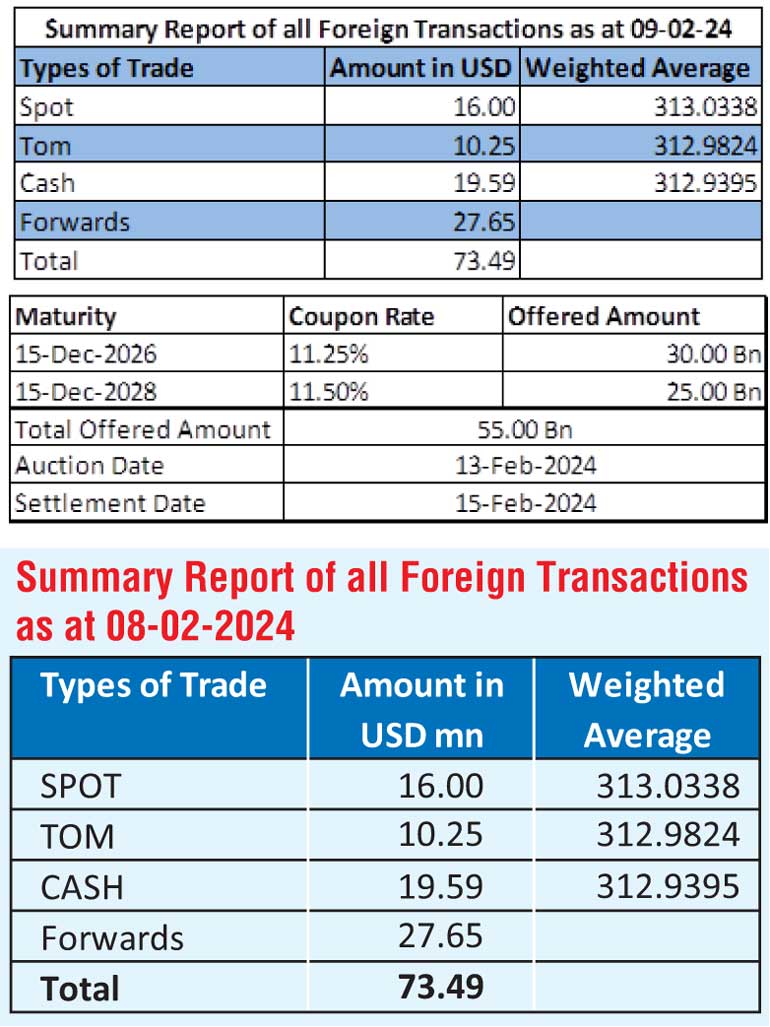

Today’s round of Treasury bond auctions will have on offer a total of Rs. 55 billion. This is comprised of Rs. 30.00 billion from a maturity of 15 December 2026 with a coupon rate of 11.25% and Rs. 25.00 billion from a maturity of 15 December 2028 with a coupon of 11.50%.

Given below are the details of the auction,

For context at the previous round of auctions conducted on the 30 January, where the exact same two maturities were offered, the entire offered amount of Rs. 40 billion on the 2026 and 2028 durations were fully taken up. The total bids received exceeded the total offered amount by a staggering 4.46 times. The 15.12.2026 maturity recorded a weighted average rate of 13.08%, while the 15.12.2028 recorded a weighted average rate of 13.65%.

Meanwhile in secondary market bill transactions, April (approximately 3 months) and July/August (approximately 6 months) 2024 maturities were seen changing hands at levels of 10.35% and 10.35% to 10.10% with sizeable volumes transacted. This was significantly below last week’s auction weighted average levels of 10.96% and 11.07% on the 3 months and 6 months tenors, respectively.

The total secondary market Treasury bond/bill transacted volume for 9 February was Rs. 12.06 billion.

In money markets, the weighted average rates on overnight call money and Repo stood at 9.13% and 9.60% respectively. The DOD (Domestic Operations Department) of Central Bank injected liquidity by way of an overnight and 7-day reverse repo auction for Rs. 35.50 billion and Rs. 40.00 billion at the weighted average rates of 9.55% and 10.00% respectively.

The net liquidity surplus stood at Rs. 22.27 billion yesterday as an amount of Rs. 12.71 billion was withdrawn from Central Banks SLFR (Standard Lending Facility Rate) of 10.00% against an amount of Rs. 110.47 billion deposited at Central Banks SDFR (Standard Deposit Facility Rate) of 9.00%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts closed the day broadly steady at Rs. 313.45/313.75 against its previous day’s closing level of Rs. 313.00/313.10.

The total USD/LKR traded volume for 09th February was $ 73.49 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking

companies)