Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Monday, 3 January 2022 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The bearish-to-negative sentiment that prevailed in the bond market during the beginning of the week ending 31 December 2021 was seen reversing to a positive sentiment towards the latter part of the week on the back of an unanticipated outcome at the Treasury bond auctions, where all bids received for the 01.08.2025 and 15.06.2027 maturities were rejected, while the 15.01.2033 maturity was accepted at a weighted average rate of 12.06%.

unanticipated outcome at the Treasury bond auctions, where all bids received for the 01.08.2025 and 15.06.2027 maturities were rejected, while the 15.01.2033 maturity was accepted at a weighted average rate of 12.06%.

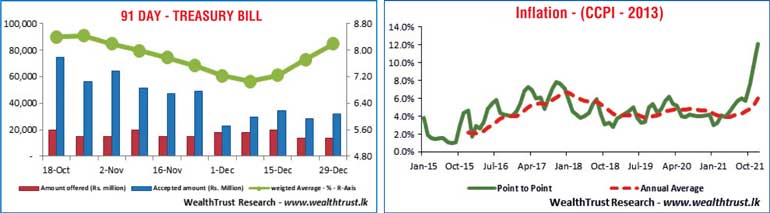

However, the weighted average rates of the weekly Treasury bill auction continued to increase with the total accepted amount falling short of the total offered amount for a third consecutive week.

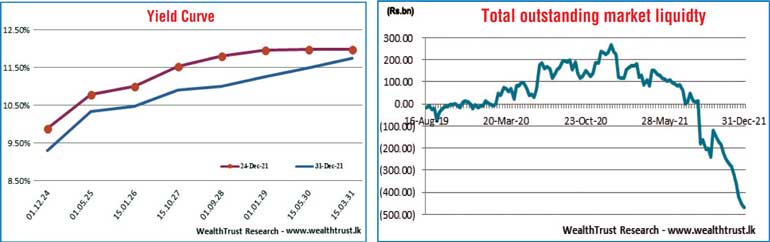

Activity in the secondary bond market see-sawed during the week as it initially moderated prior to the bond auction outcomes as yields increased on the maturities of 2025’s (i.e., 15.03.25, 01.05.25 and 01.08.25) to highs of 11.20% each and 11.45% respectively.

Subsequently, following the auction outcomes, yields on the maturities of 01.12.24, 01.05.25, 15.10.27, 01.09.28 and 15.05.30 were seen decreasing sharply to lows of 9.26%, 10.30%, 10.98%, 11.27% and 11.83% respectively on the back of aggressive buying interest as activity increased towards the later part of the week, reflecting a downward shift of the overall yield curve for the first time in three consecutive week.

Meanwhile, the Colombo Consumer Price Index (CCPI; Base 2013=100) for the month of December increased sharply to its all-time high of 12.1% on the point-to-point, when compared against its previous month’s figure of 9.9%, along with the annual average increasing as well to 6% from 5.3%.

The foreign holding in rupee bonds remained steady at Rs. 1.75 billion for the week ending 29 December 2021, while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 8.80 billion.

In money markets, the net liquidity shortfall increased to Rs. 466.25 billion against its previous weeks Rs. 455.55 billion, while CBSL’s holding of Government Security’s increased as well to Rs. 1,416.75 billion against its previous weeks of Rs. 1,362.76 billion. The weighted average rates on overnight call money and repo averaged 5.94% and 5.99% respectively for the week.

USD/LKR

In the Forex market, the USD/LKR rate on spot contracts continued to trade within the range of Rs. 202.97 to Rs. 203 during the week while overall activity remained moderate.

The daily USD/LKR average traded volume for the first four trading days of the week stood at US $ 32.20 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)