Sunday Jun 07, 2026

Sunday Jun 07, 2026

Monday, 29 March 2021 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The trading activity in the secondary bond market remained rather moderate during the week ending 26 March as most market participants persisted to be on the side lines ahead of scheduled Treasury bond auctions for today, 29 March.

The trading activity in the secondary bond market remained rather moderate during the week ending 26 March as most market participants persisted to be on the side lines ahead of scheduled Treasury bond auctions for today, 29 March.

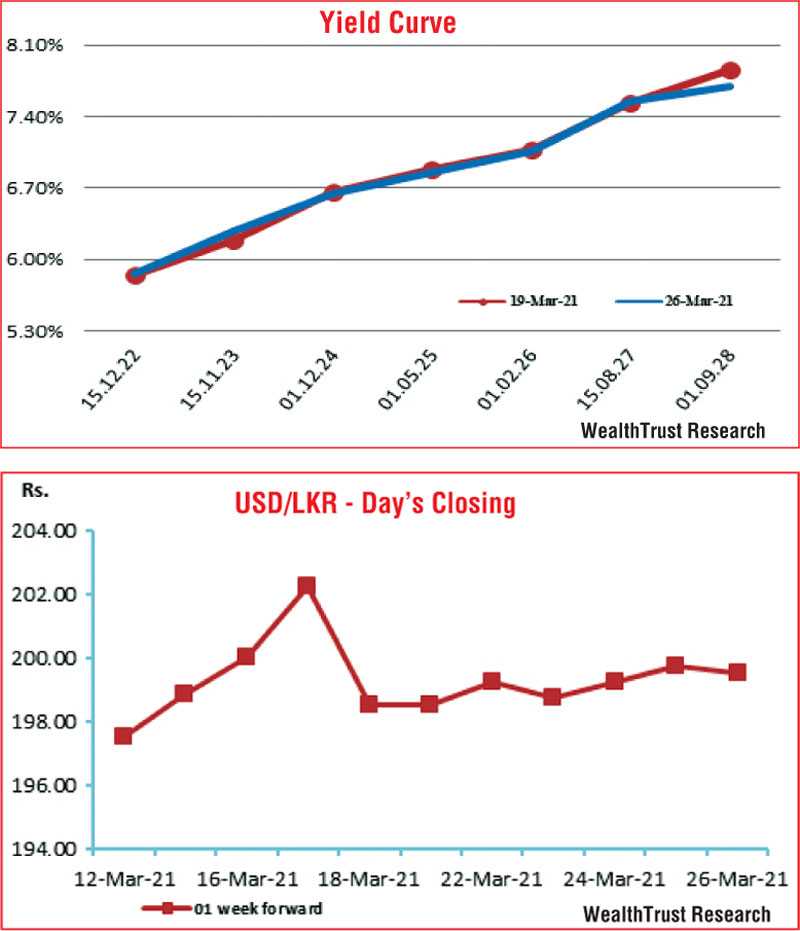

The auction will have on offer a total amount of Rs. 60 billion, consisting of Rs. 25 billion of 15.11.2023, Rs. 20 billion of 15.01.2026 and Rs. 15 billion of 01.05.2028. The maximum yields rate for acceptance for the said maturities was published at 6.30%, 7.05% and 7.60% respectively. The weighted average yields at the bond auctions conducted on 10 March were 6.19%, 7.08% and 7.44% for the maturities of 01.09.2023, 01.02.2026 and 15.08.2027 respectively.

The weekly T-bill auction went undersubscribed for a third consecutive week as only an amount of Rs. 11.55 billion was accepted in total against its total offered amount of Rs. 45 billion.

In secondary bond markets, the limited activity during the week centred on the maturities of 2022’s (i.e. 01.10.22, 15.11.22 and 15.12.22), 15.01.23, other 2023’s (i.e. 15.05.23, 15.07.23 and 01.09.23), 01.01.24, mid 2024’s (i.e. 15.06.24 and 15.09.24) and 01.12.24 within the range of 5.80% to 5.88%, 5.93% to 5.95%, 6.15% to 6.22, 6.40% to 6.42%, 6.55% to 6.60% and 6.60% to 6.68% respectively while in the secondary bill market, May and June maturities and September 2021 maturities traded at levels of 4.80% to 5.04% and 4.95% to 5.09% respectively.

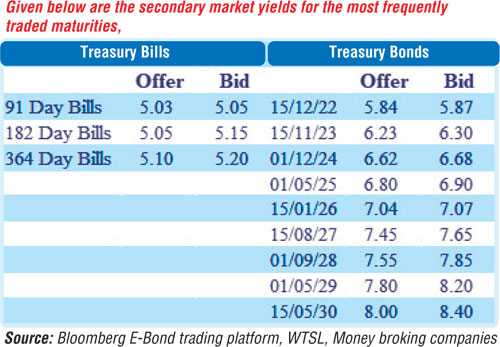

The foreign holding in rupee bonds stood at Rs. 5.78 billion for the week ending 24 March, reflecting a further outflow of Rs. 650 million. The daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 4.70 billion.

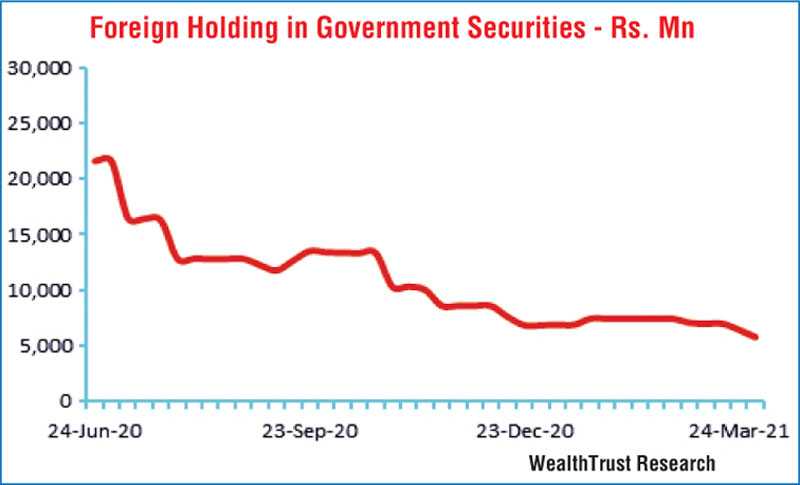

In money markets, the total outstanding market liquidity was seen decreasing further during the week to a low of Rs. 100.67 billion against its previous weeks closing of Rs. 119.18 billion, before increasing once again to close the week at Rs. 127.70 billion. The weighted average rates on overnight call money and repo remained mostly unchanged to average 4.58% and 4.60% respectively for the week while the CBSL’s holding of Gov. Security’s increased further to Rs. 842.25 billion.

USD/LKR

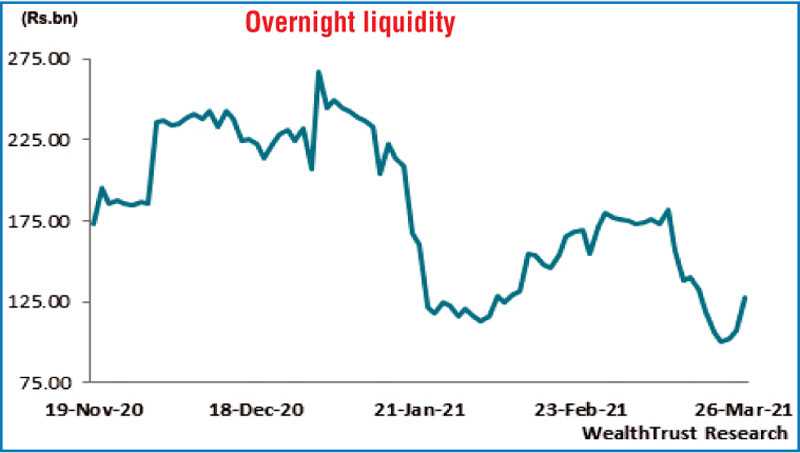

In Forex markets, the USD/LKR rate on the more active one-week forward contracts were seen closing the week at Rs. 199.25/199.75 in comparison to its previous weeks closing level of Rs. 198.00/199.00.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 82.40 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)