Wednesday Feb 25, 2026

Wednesday Feb 25, 2026

Monday, 19 February 2024 01:59 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary bond market commenced the trading week ending 16 February on a bullish note with yields edging downwards to fresh lows on selected maturities, on the back of robust buying interest and substantial volumes.

The secondary bond market commenced the trading week ending 16 February on a bullish note with yields edging downwards to fresh lows on selected maturities, on the back of robust buying interest and substantial volumes.

The bullish momentum was carried over from the previous week and was spurred by the impressive outcomes at the Treasury bond and bill auctions. However, subsequent to this at the latter part of the week profit-taking saw yields edge upwards. Nevertheless, a fresh wave of buying was seen kicking in at those elevated levels, curtailing the upward momentum. In conclusion, yields were seen closing the week broadly unchanged compared to the week prior, with active trading continuing to be predominantly on the short-medium end of the yield curve. In particular 2025 to 2028 durations continued to be popular.

The yield on 2028 tenors (15.03.28, 01.05.28, 01.07.28, and 15.12.28) were seen hitting intraweek high levels of 12.15% against intraweek lows of 11.75%, before settling at a closing two-way quote of 11.95%/12.05% (offer/bid). Similarly, the liquid 01.08.26 maturity was seen ascending to an intraweek high of 11.30% as against lows of 10.60%, settling at a closing two way of 10.90/11.00. Additionally, trades were also seen on the maturities of 2025’s (01.06.25 and 01.07.25), 15.09.27 and 01.07.32 within intraweek lows and highs of 10.23% to 10.25%, 11.35% to 11.70% and 12.50% to 12.73% respectively.

The Treasury bond auctions conducted last Tuesday (13 February 2024) recorded a bullish outcome, with the entire offered amount of Rs. 55 billion on the 2026 and 2028 durations being fully taken up. The total bids received exceeded the total offered amount by an impressive 2.74 times. The 15.12.2026 maturity recorded a weighted average rate of 10.81%, while the 15.12.2028 recorded a weighted average rate of 11.90%. For reference, during the last Treasury bond auctions held on the 30 January, the same two maturities were issued at the weighted averages of 13.08% and 13.65% respectively. A further Rs. 11 billion, being the maximum amount offered, was raised out of a total market subscription of Rs. 53.61 billion via a Direct Issuance Window across both maturities.

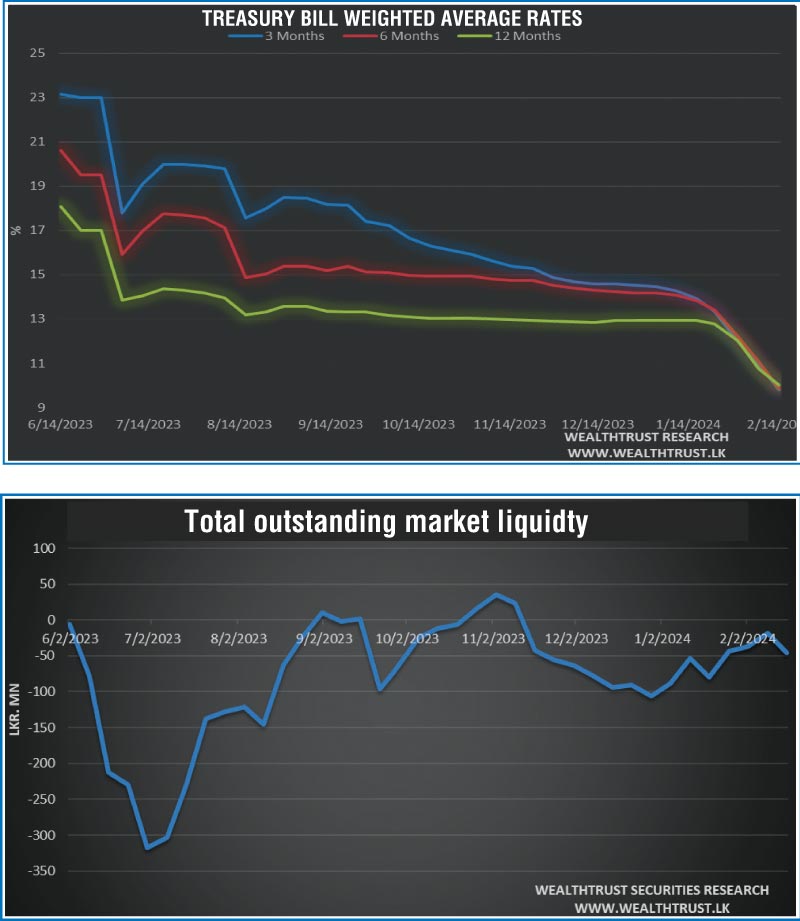

At the weekly Treasury bill auction last Wednesday (14 February 2024), the weighted average yields dropped dramatically across the board, for a fifth consecutive week. In particular, the weighted average yields on the 91-day and 182-day maturities declined to 9.79% and 9.86% respectively, reflecting drops of 117 and 121 basis points against its previous week and as a result, falling below the Standing Lending Facility Rate (SLFR) of 10.00%. The 364-day maturity too plunged by 71 basis points to 10.02%. The strong demand saw the total offered amount of Rs. 135 billion raised at the 1st phase of the auction, with the total bids received exceeding the offered amount by over 2 times.

A further Rs. 33.75 billion was raised at the 2nd phase, being the maximum aggregate amount offered, only on the 182-day and 364-day maturities. The 2nd phase also went heavily oversubscribed with bids exceeding Rs. 75 billion.

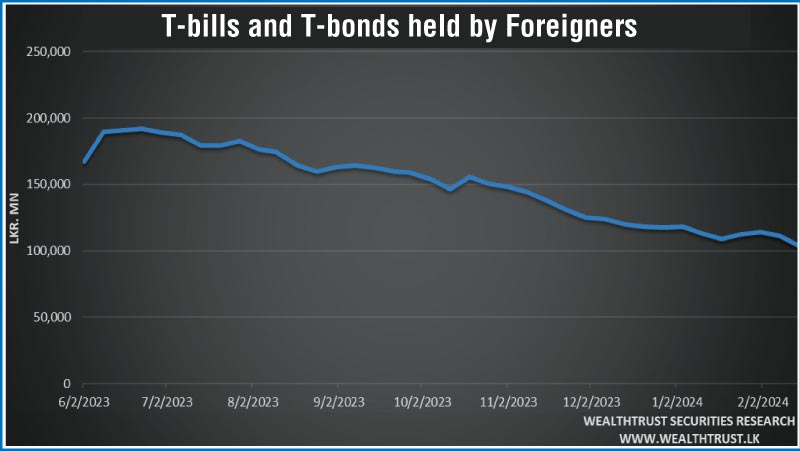

The foreign holding in Rupee bonds and bills for the week ending 15 February 2024 recorded a net outflow for a second consecutive week, amounting to Rs. 7.54 billion. As a result, the total holding decreased to Rs. 103.61 billion.

The daily secondary market Treasury bond/bill transacted volumes for the first four days of the week averaged at Rs. 32.15 billion.

In money markets, the total outstanding liquidity deficit increased to Rs. 46.20 billion by the week ending 9 February from its previous week’s deficit of Rs. 18.68 billion. The Domestic Operations Department (DOD) of the Central Bank continued to inject liquidity during the week by way of overnight and term reverse repo auctions at weighted average yields ranging from 9.17% to 10.00%.

The Central Bank of Sri Lanka’s (CBSL) holding of Government Securities was registered at Rs. 2,735.62 billion as at 16 February 2024, unchanged from its previous week’s level.

In the forex market, the USD/LKR rate on spot contracts was seen appreciating slightly during the week to close at Rs. 312.20/312.35. This is as against its previous week’s closing level of Rs. 313.00/313.10 and subsequent to trading at a high of Rs. 315.40 and a low of Rs. 313.80.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 50.45 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)