Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Monday, 9 November 2020 02:06 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The activity in the secondary bond market continued at a moderate pace during the week ending 6 November as most market participants continued to be on the sidelines ahead of the scheduled primary Treasury bond auctions due on 12 November.

The activity in the secondary bond market continued at a moderate pace during the week ending 6 November as most market participants continued to be on the sidelines ahead of the scheduled primary Treasury bond auctions due on 12 November.

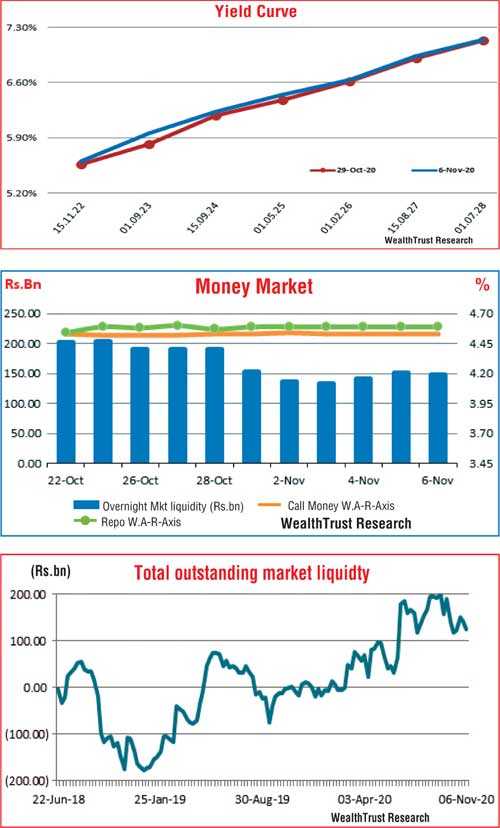

The week witnessed a limited amount of trades on the maturities of 15.12.22, 2023’s (i.e. 15.07.23 and 15.12.23), 2024’s (i.e. 01.08.24 and 15.09.24), 01.05.25, 15.08.27 and 01.07.28 as its yields increased marginally to weekly highs of 5.65%, 5.90%, 5.95%, 6.35%, 6.20%, 6.38%, 6.93% and 7.15%, respectively, against its previous weeks closing levels of 5.58/63, 5.75/90, 5.85/95, 6.20/23, 6.17/18, 6.35/40, 6.87/95 and 7.10/15. In addition, maturities of 01.08.21, 15.03.22 15.11.22, 01.02.26, 15.10.27 and 01.05.28 were traded at levels of 4.80%, 5.40%, 5.58%, 6.57% to 6.60%, 6.97% to 6.99% and 7.16% to 7.18%, respectively, as well. Meanwhile, the weekly Treasury bill auction was undersubscribed for a second consecutive week while January, February, March, April and September 2021 bill maturities changed hands at levels of 4.60%, 4.61%, 4.62%, 4.65% to 4.70% and 4.82%, respectively, in the secondary bill market.

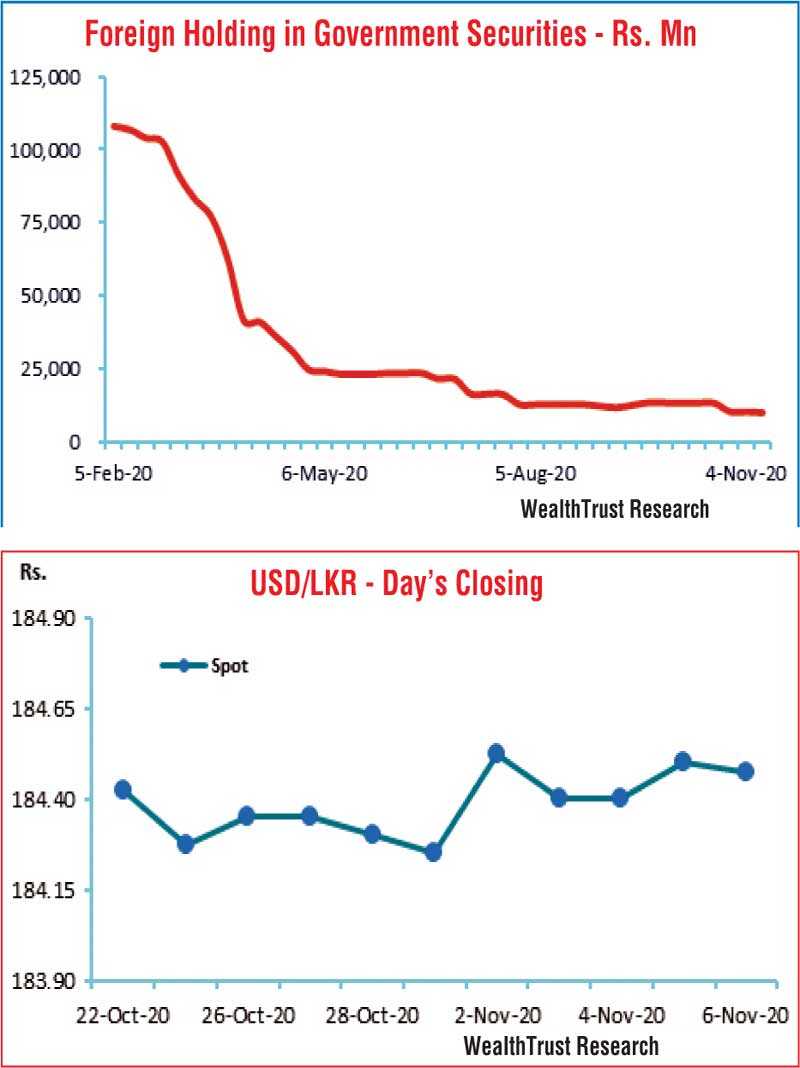

The foreign holding in Rupee bonds recorded a marginal outflow of Rs. 0.3 billion for the week ending 4 November.

The daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 6.57 billion.

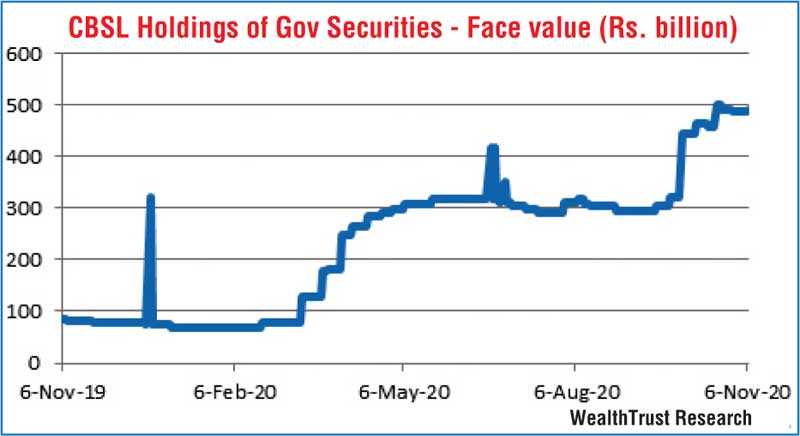

In money markets, the total outstanding market liquidity decreased for a second consecutive week to record a surplus of Rs. 123.80 billion against its previous week of Rs. 140.11 billion. The weighted average rates on overnight call money and repo remained steady at 4.53% and 4.59%, respectively, for the week as the Central Bank Domestic Operations Department (DOD) was seen injecting liquidity during the early part of the week by way of 14-day reverse repo auctions at weighted average yields of 4.54% to 4.55% while the overnight surplus liquidity was seen dipping below Rs. 140 billion. The CBSL’s holding of Government Securities increased marginally to 492.16 billion.

Rupee loses marginally

The USD/LKR rate on spot contracts was seen depreciating marginally during the week to close the week at Rs. 184.45/50 against its previous week’s closing levels of Rs. 184.20/30 subsequent to trading within the range of Rs. 184.35 to Rs. 184.60.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 77.73 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, money broking companies)