Monday Feb 23, 2026

Monday Feb 23, 2026

Monday, 21 September 2020 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The sentiment in the secondary bond market turned sluggish to bearish during the week ending 18 September as activity dried up considerably, bearing a few sporadic trades. The sentiment was further supported by the outcome of the weekly Treasury bill auction, where the total accepted amount was seen falling short of the total offered amount.

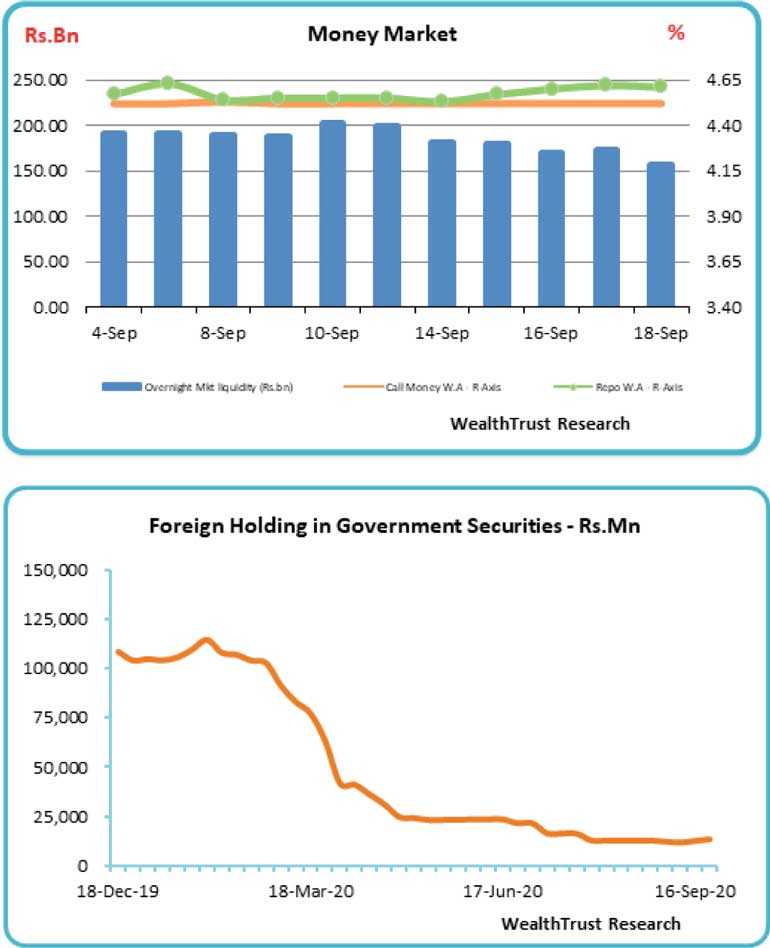

Nevertheless, foreign holding in rupee bonds recorded an increase for a second consecutive week with an inflow of Rs. 858 million for the week ending 16 September.

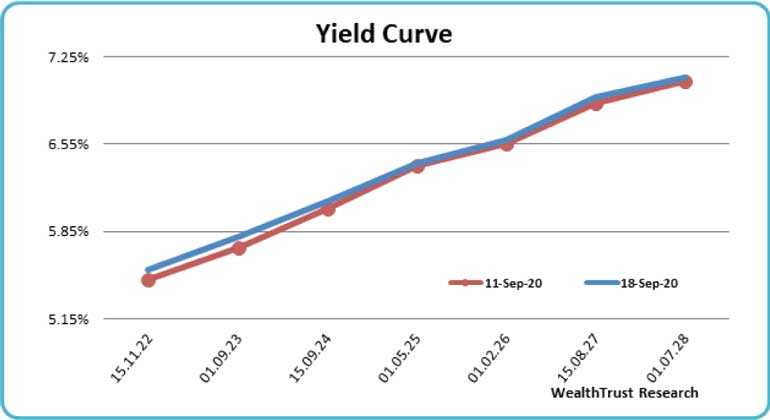

The limited trades seen during the week saw yields fluctuate within a narrow range mainly on the maturities of 2022s (i.e. 15.11.22 & 15.12.22), 2023s (i.e. 15.05.23, 01.09.23 & 01.10.23), 2024s (i.e. 15.06.24 & 15.09.24), 01.05.25, 01.02.26, 15.08.27 and 01.07.28 at levels of 5.53% to 5.57%, 5.70% to 5.80%, 6.08% to 6.10%, 6.37%, 6.56% to 6.59%, 6.88% to 6.95% and 7.05% respectively. This intern reflected a marginal shift upwards of the overall yield curve. In secondary bills, October to December 2020, March 2021 and August 2021 maturities traded at level of 4.52% to 4.57%, 4.65% and 4.80% respectively.

The daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 5.58 billion.

SLFR accessed/liquidity decreases

In the money market, the standing Lending Facility Rate (SLFR) of Central Bank or discount window at 5.50% was accessed during the week for the first time since 18 August. This was despite the average net overnight surplus liquidity in the system registering at Rs. 172.24 billion for the week, below its previous week’s average of Rs. 194.12 billion. However, the weighted average rates on overnight call money and repos remained broadly steady at 4.52% and 4.59% respectively for the week.

Rupee loses

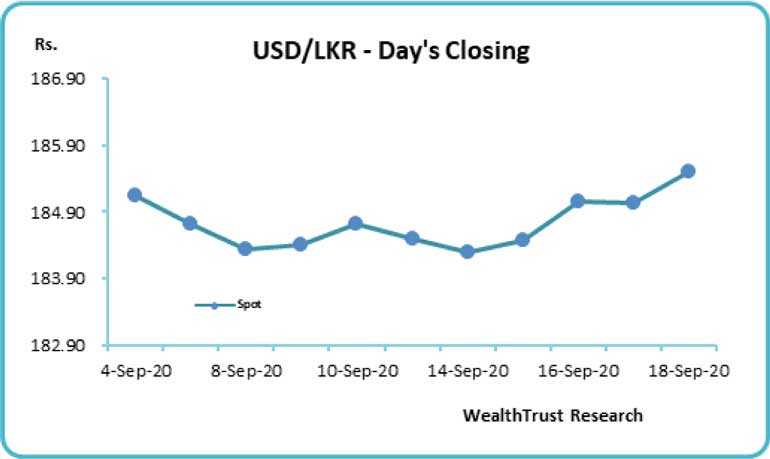

In the Forex market, the Rupee on its spot contacts was seen depreciating during the week to close the week at Rs. 185.45/55 against its previous weeks closing level of Rs. 184.45/55, subsequent to trading within the range of Rs. 184.10 to Rs. 185.50.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 84.74 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)