Monday Feb 16, 2026

Monday Feb 16, 2026

Monday, 19 June 2023 01:51 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

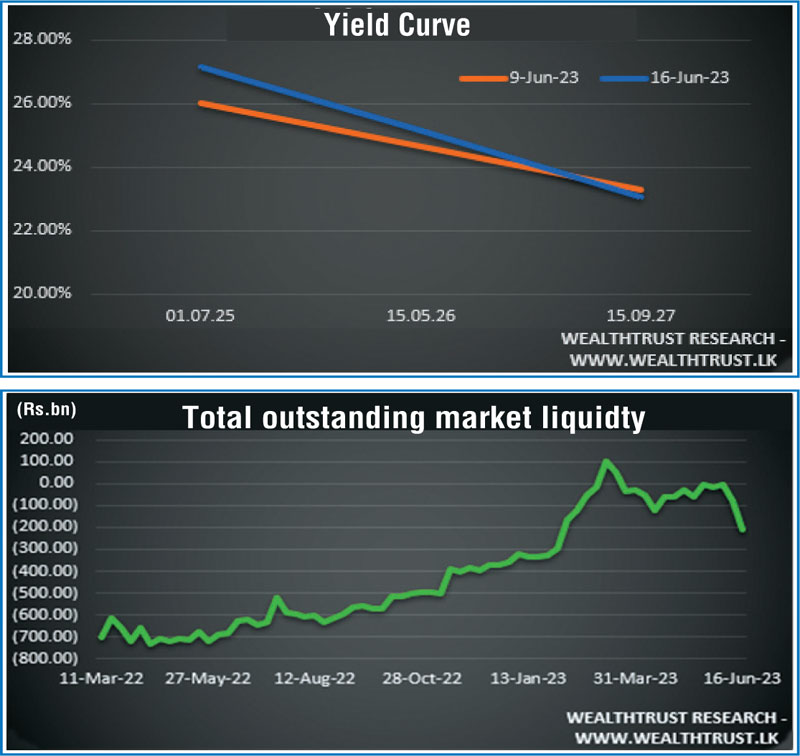

The secondary market bond yield curve was seen steepening during the trading week ending 16 June as yields on the short-dated maturities of 2025’s (01.06.25 and 01.07.25) and 15.05.26 was seen increasing while yields on the maturities of 2027’s (15.05.27 and 15.09.27) and beyond were seen holding broadly steady.

The secondary market bond yield curve was seen steepening during the trading week ending 16 June as yields on the short-dated maturities of 2025’s (01.06.25 and 01.07.25) and 15.05.26 was seen increasing while yields on the maturities of 2027’s (15.05.27 and 15.09.27) and beyond were seen holding broadly steady.

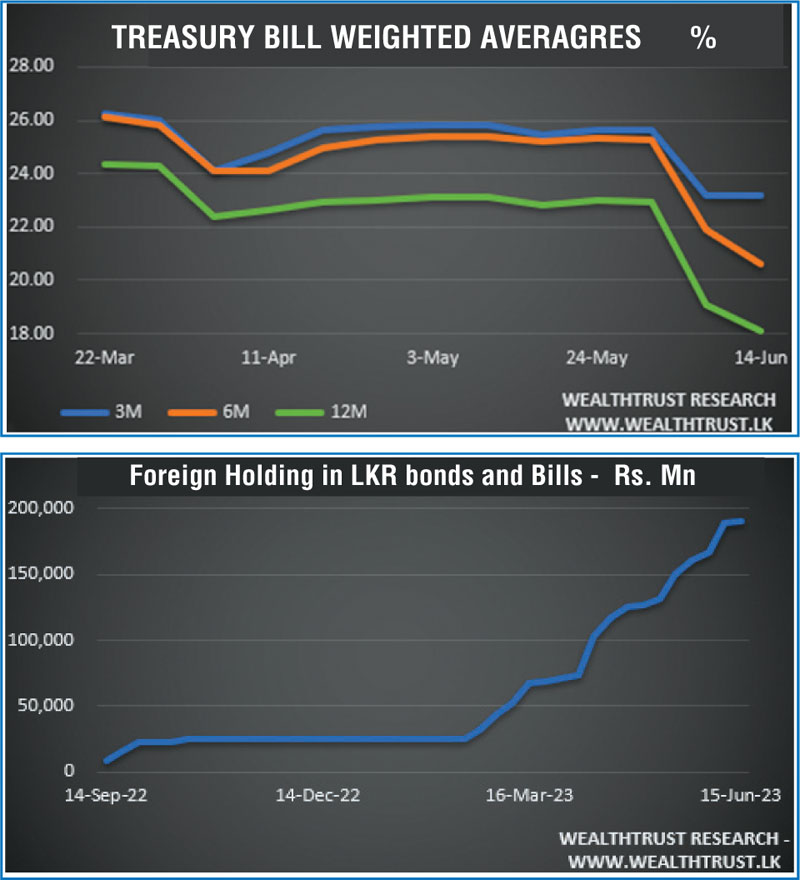

This was despite the weighted averages of the six month and one year Treasury bills tumbling sharply for a second consecutive week.

The total offered amount of Rs. 180 billion at the weekly Treasury bill auction was fully taken up at the 1st Phase of the auction while a further Rs. 45 billion was taken up at the 2nd Phase. The market demanded maturities of six months or 182 days and 1 year or 364 days recorded significant drops 129 basis points and 102 basis points respectively to 20.61% and 18.08%.

Nevertheless, foreign inflows into rupee securities recorded its slowest increase in 12 weeks with Rs. 1 billion for the week ending 15 June.

Furthermore, the total outstanding liquidity deficit was seen increasing sharply during the week to a 19-week high of Rs. 212.12 billion by the end of the week against its previous week’s Rs. 78.85 billion. This intern saw the Domestic Operations Department (DOD) of Central Bank continuing to inject liquidity during the week by way of overnight to 30-day Reverse repo auctions at weighted average yields ranging from 13.47% to 16.80%. The CBSL’s holding of Government Securities decreased to Rs. 2,476.79 billion from its previous week’s Rs. 2,528.03 billion.

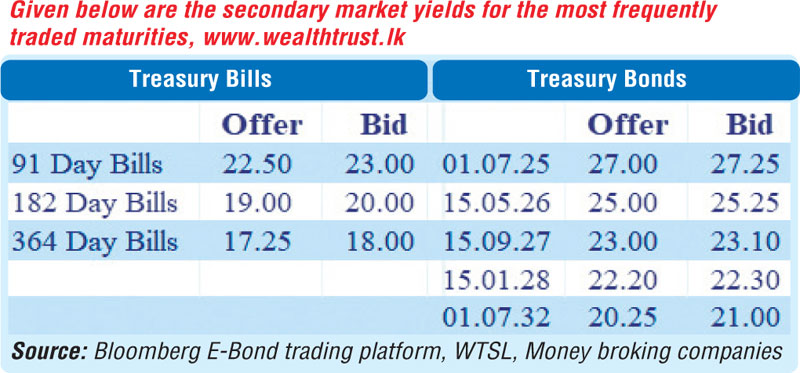

The secondary market bond trades during the week saw yields fluctuate mainly on the maturities of 01.07.25, 15.05.26, two 2027’s (i.e., 01.05.27 and 15.09.27) and 15.01.28 within levels of 25.75% to 27.05%, 23.95% to 25.25%, 22.60% to 23.50% and 21.90% to 22.25% respectively.

The daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 42.26 billion.

In the forex market, demand for the green back saw the USD/LKR rate on spot contracts depreciate further during the week to close the week at Rs. 304.00/306.00 against its previous week of Rs. 297.50/298.00, subsequent to trading at an intra week low of Rs. 320.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 65.60 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)