Tuesday Feb 17, 2026

Tuesday Feb 17, 2026

Wednesday, 15 January 2025 00:13 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

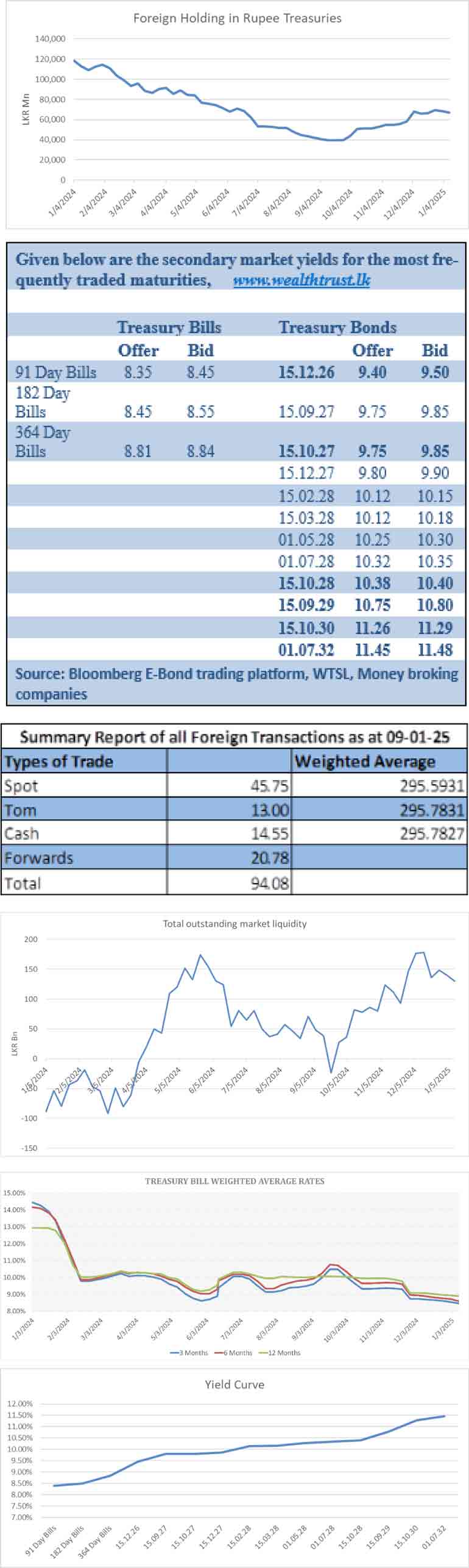

The Secondary Bond market began the week with yields initially moving upwards. However, towards mid-week, a recovery on the back of renewed buying interest drove rates back down. The recovery was spurred by the bullish outcome at the Treasury Bill auction. As a result, on a week-on-week basis, two-way quotes were seen holding broadly steady and as such the T-Bond section of the yield curve closed the week mostly unchanged.

The notable exception were the 2026 tenors that bucked the trend and saw yields consistently decline during the week with the 01.02.26, and 01.08.26 maturities seen trading at the rates of 8.95%-8.80% and 9.30%-9.20% respectively. However, the rest of the yield curve followed an inverted-U shaped trading pattern. The market favourite 2028 tenors experienced the most activity. The 15.02.28, 01.05.28 01.07.28, 15.10.28 and were seen trading at the elevated rates of 10.20%, 10.40%, 10.45% and 10.55% before recovering to move back down to trade at lows of 10.15%, 10.23%, 10.33%, 10.37% respectively. The 15.10.30 maturity which hit an intraweek high of 11.35% post-auction was seen declining to a low of 11.26% at the tail end of the week.

At the weekly Treasury Bill auction conducted last Wednesday (08/01/2025), weighted average rates declined across all three maturities for the fifth consecutive week. Accordingly, the weighted average rates on the 91-day tenor dropped by 8 basis points to 8.47%, the 182-day tenor by 12 basis points to 8.60% and the 364-day tenor by 4 basis point to 8.9%. Total bids received exceeded the offered amount by 2.87 times, and the entire Rs. 102 billion on offer was successfully raised at the first phase in competitive bidding. In addition, an amount of Rs. 10.20 billion, being the maximum amount offered, was raised at the second phase out of a total market subscription of a staggering Rs. 108.97 billion.

The Treasury Bond auctions held on 9 January raised Rs. 179.25 billion, or 94.34% of the Rs. 190.00 billion offered, despite bids exceeding the offering by 2.06 times. Maturity-wise:The 15.10.28 maturity (11.00% coupon) saw strong demand, raising Rs. 60 billion at a weighted average yield of 10.42%. This was below the highs of 10.55% the bond was seen trading at earlier in the week but aligned with the market quote of 10.40%/10.43% just prior to the auction.

The 15.10.30 maturity (11.00% coupon) raised Rs. 80 billion at a weighted average yield of 11.23%, slightly above market expectations as the Bond was quoted at the two-way rate of 10.10%/10.15% just prior to the auction.

The 01.11.33 maturity (9.00% coupon) achieved a weighted average yield of 11.47%, in line with market expectations, but raised only 78.50% or Rs. 39.25 billion across both phases.

For the week ending 9 January 2025, the foreign holdings in Sri Lankan rupee-denominated Treasury securities saw a net outflow for the second consecutive week amounting to Rs. 1.30 billion. As a result, total foreign holdings were seen decreasing to Rs. 67.23 billion.

The daily secondary market Treasury Bond/Bill transacted volumes for the first four days of the week averaged at Rs. 55.20 billion.

In money markets, the total outstanding liquidity surplus decreased to Rs. 130.26 billion as at the week ending 10 January, from Rs. 140.16 billion recorded the previous week. The Domestic Operations Department (DOD) of Central Bank injected liquidity during the week by way of overnight and three-day term reverse repo auctions at weighted average rates of 8.14% and 8.06% respectively. The weighted average interest rate on call money and repo ranged between 7.98% to 8.00% and 8.00% to 8.06% respectively.

The Central Bank of Sri Lanka’s (CBSL) holding of Government Securities was registered at Rs. 2,515.62 billion as at 10 January 2025, unchanged from the previous week’s level.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts was seen depreciating, to close the week at Rs. 294.70/294.95 as against its previous week’s closing level of Rs. 293.95/294.15 and subsequent to trading at a high of Rs. 294.30 and a low of Rs. 296.50.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 80.05 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)