Thursday Feb 19, 2026

Thursday Feb 19, 2026

Thursday, 12 January 2023 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

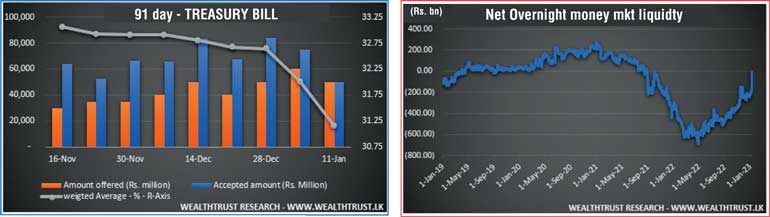

The weekly Treasury bill weighted average rates were seen continuing its bullish momentum, recording considerable dips across all three maturities for a second consecutive week at its auctions held yesterday.

The weekly Treasury bill weighted average rates were seen continuing its bullish momentum, recording considerable dips across all three maturities for a second consecutive week at its auctions held yesterday.

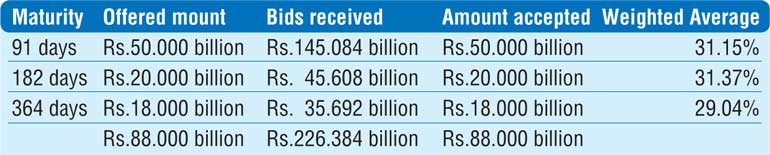

The market favourite 91-day bill maturity recorded the steepest drop of 86 basis points to 31.15% while the 182-day and 364-day bills registered dips of 65 and 12 basis points respectively to 31.37% and 29.04%. The total offered volume was fully accepted at the auction for a fifth consecutive week while the bids to offer ratio stood at 2.57:1.

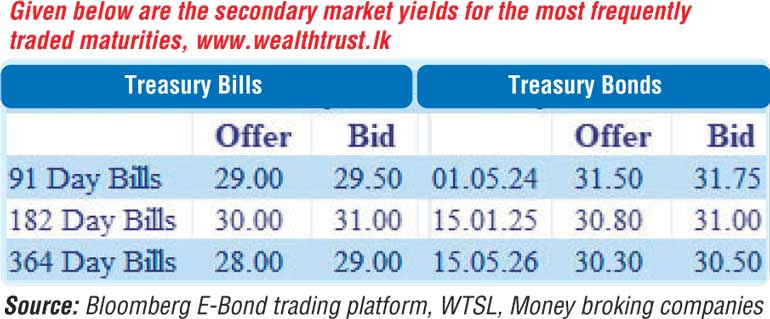

Meanwhile, the secondary bond market remained active yesterday as the maturities of 01.05.24, 15.01.25 and 15.05.26 traded at levels of 31.70% to 31.80%, 30.90% to 31.00% and 30.50% to 30.65% respectively. In secondary bills, the 7 April 2023 maturity traded at levels of 29.00% to 29.50%, post auction.

Today’s Treasury bond auctions, conducted in lieu of a Treasury bond maturity of Rs. 129.55 billion due on 15 January will see a total amount of Rs. 160 billion on offer consisting of Rs. 50 billion on a 15.05.2026 maturity and Rs. 110 billon on a new 15.09.2027 maturity.

At the last bond auctions conducted on 29 December 2022, the 15.05.2026 maturity was issued at a weighted average rate of 31.36% with an amount of Rs. 53.12 billion being accepted against its offered amount of Rs. 60 billion. All bid received on the 15.01.2025 maturity was rejected.

The total secondary market Treasury bond/bill transacted volume for 10 January 2023 was Rs. 6.13 billion.

In money markets, the overnight liquidity deficit was seen bottoming out yesterday to only Rs 9.23 billion against a peak of Rs. 688.29 billion recorded on 27 April 2022. An amount of Rs. 349.29 billion was deposited at Central Banks SDFR (Standard Deposit Facility Rate) of 14.50% against an amount of Rs. 358.52 billion withdrawn from Central Banks SLFR (Standard Lending Facility Rate) of 15.50%. The weighted average rates on overnight Call money and Repo stood at 15.50% each.

The DOD (Domestic Operations Department) of Central Bank injected liquidity by way of 30-day and 90-day reverse repo auctions for a total volume of Rs. 90 billion at weighted average rates of 28.15% and 29.24% respectively.

Forex market

In the forex market, the middle rate for USD/LKR spot contracts registered at Rs. 362.24 yesterday against its previous day’s closing level of Rs. 362.2446.

The total USD/LKR traded volume for 10 January was $ 76.20 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)