Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Thursday, 16 January 2025 02:26 - - {{hitsCtrl.values.hits}}

By WealthTrust Securities

The Secondary Bond market yesterday saw yields move in range bound trading, closing broadly steady, while activity and transaction volumes were seen at healthy levels.

The Secondary Bond market yesterday saw yields move in range bound trading, closing broadly steady, while activity and transaction volumes were seen at healthy levels.

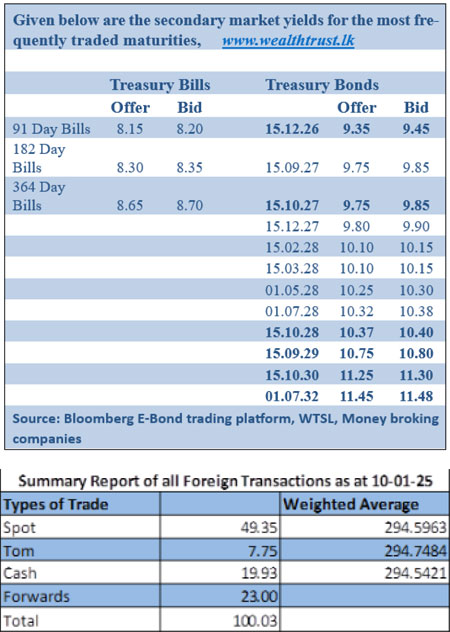

The 2026 tenors of 01.06.26 and 01.08.26 were seen trading at the rates of 9.10% and 9.15% respectively. The 15.09.27 and 15.10.27 maturities were seen trading within the range of 9.87%-9.80%. The early 2028 tenor 15.02.28 and 15.03.28 maturities were seen trading within the range of 10.20%-10.10%. The mid-2028 tenor 01.05.28 and 01.07.28 were seen changing hands within the ranges of 10.32%-10.26% and 10.38%-10.36%, respectively. The late-2028 tenor 15.10.28 and 15.12.28 maturities were seen transacting at the rates of 10.40% and 10.45%, respectively.

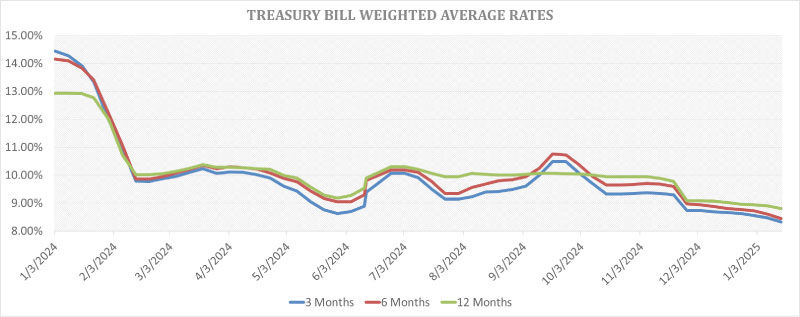

The weighted average rates declined across all three maturities for the sixth consecutive week at its weekly Treasury bill auction conducted yesterday (15 January). Accordingly, the weighted average rates on the 91-day tenor dropped by 14 basis points to 8.33%, the 182-day tenor by 16 basis points to 8.44% and the 364-day tenor by 10 basis points to 8.80%. Total bids received exceeded the offered amount by 2.98 times, and the entire Rs. 107 billion on offer was successfully raised at the first phase in competitive bidding.

The second phase of subscription for the auction will be opened across all three tenors at the weighted average rates until close of business of the day prior to settlement (i.e., 3 p.m. today)

The total secondary market Treasury bond/bill transacted volume for 10 January 2025 was Rs. 18.57 billion.

In money markets, the weighted average rates on overnight call money and repo stood at 8.00% and 8.06% respectively. The DOD injected liquidity amounting to Rs. 15 billion by way of a 6-day term reverse repo auction at the weighted average yield of 8.07%.

The net liquidity surplus stood at Rs. 79.61 billion yesterday. Rs. 0.66 billion was withdrawn from the Central Bank’s SLFR (Standing Lending Facility Rate) of 8.50%, while an amount of Rs. 95.26 billion was deposited at the Central Bank’s SDFR (Standard Deposit Facility Rate) of 7.50%.

Forex market

In the Forex market, the USD/LKR rate on spot contracts closed the day depreciating to Rs. 295.60/296.00 as against its previous day’s closing level of Rs. 294.70/294.95.

The total USD/LKR traded volume for 10 January 2025 was $ 100.03 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)