Monday Feb 16, 2026

Monday Feb 16, 2026

Friday, 10 January 2025 00:10 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

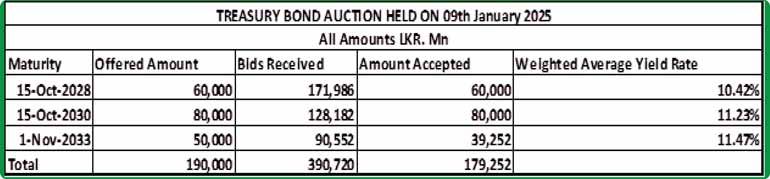

The round of Treasury bond auctions conducted yesterday overall raised 94.34% or Rs. 179.25 billion out of the entire offered amount of Rs. 190.00 billion. This was despite total bids received exceeded the offered amount by 2.06 times.

The round of Treasury bond auctions conducted yesterday overall raised 94.34% or Rs. 179.25 billion out of the entire offered amount of Rs. 190.00 billion. This was despite total bids received exceeded the offered amount by 2.06 times.

In particular, the 15.10.28 maturity (11.00% coupon) recorded a bullish outcome and was issued at a weighted average yield of 10.42%. This was incidentally the same weighted average it was issued at the immediately previous auction on 30 December 2024. This was well below a high of 10.55%. The maturity was seen trading earlier in the week, but in line with the market two-way quote of 10.40%/10.43% seen as sentiment recovered while the auction was ongoing. Maturity-wise the entire Rs 60.00 billion offered was snapped up at the first phase of subscription in competitive bidding.

The 15.10.30 maturity (11.00% coupon) also raised the entire maturity-wise offered amount of Rs. 80.00 billion at the first phase and was issued at the weighted average rate of 11.23%. However, this was slightly above market expectations, with a market two way of 10.10%-10.15% being quoted earlier in the day, prior to the conclusion of the auction.

A 01.11.33 maturity (09.00% coupon) was issued at a weighted average yield of 11.47%. This was in line with market expectations. However, only managing to raise 78.50% or Rs 39.25 billion across both phases.

An issuance window for the 15.10.28 and 15.10.30 maturities is open until close of business day prior to settlement date (i.e., 3 p.m. on 10.01.2025) at its Weighted Average Yield Rate (WAYR), up to 10% of the amount offered.

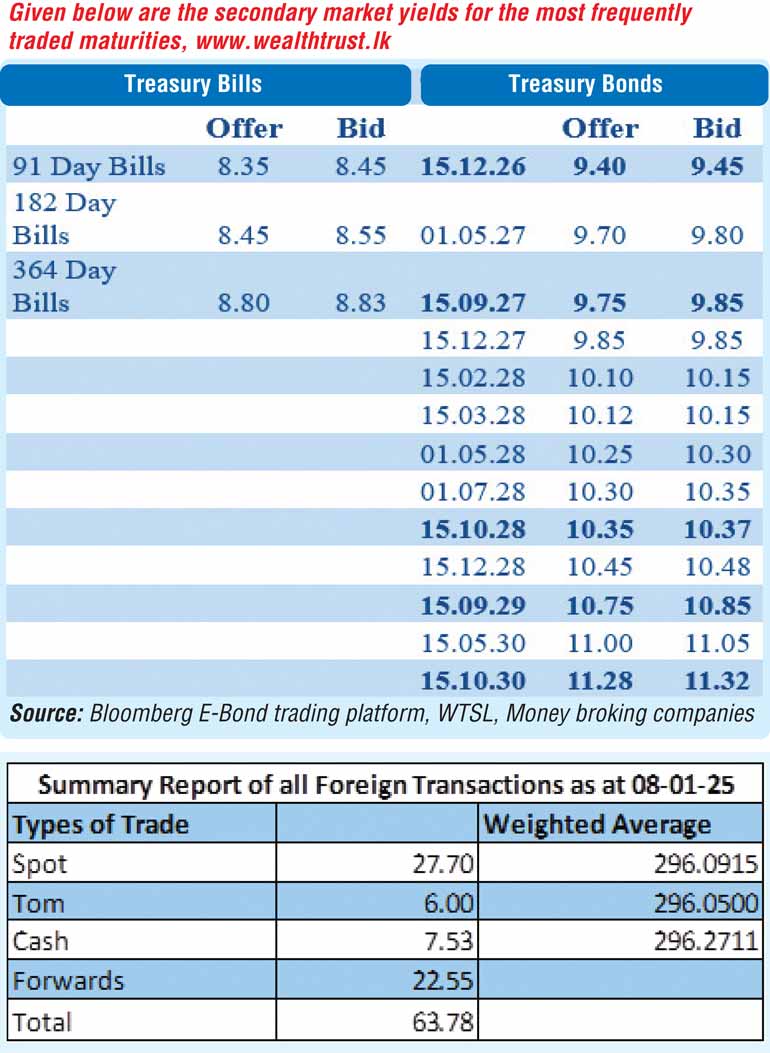

Meanwhile, the secondary Bond market saw yields decline on the back of robust buying interest, both while the auction was underway and after the announcement of the results. Activity and transaction volumes were seen at elevated levels. This carried over the momentum from the Treasury bill Auction the day before, which saw T-Bill rates decline for the ninth consecutive week.

The 01.02.26, 01.08.26 and 15.12.26 maturities were seen trading at the rates of 8.80%, 9.25% and 9.43%-9.40% respectively. The 01.05.28 and 01.07.28 maturities saw yields slide down the ranges of 10.30%-10.23% and 10.45%-10.33% respectively. The 15.10.28 maturity continued to see strong demand post-auction, which saw trades at a low of 10.37% which was even below the weighted average level of 10.42% it was issued at auction. The 15.12.28 maturity saw yields decline from intraday highs to lows of 10.50%-10.45%. The 15.05.30 maturity was seen trading down the range of 11.05%-11.00%.

The total secondary market Treasury bond/bill transacted volume for 8 January was Rs. 90.17 billion.

In money markets, the weighted average rates on overnight call money and Repo stood at 7.99% and 8.06% respectively.

The net liquidity surplus stood at Rs. 142.11 billion yesterday. Rs. 0.44 billion was withdrawn from the Central Banks SLFR (Standing Lending Facility Rate) of 8.50%, while an amount of Rs. 142.54 billion was deposited at Central Banks SDFR (Standard Deposit Facility Rate) of 7.50%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts closed the day appreciating considerably to Rs. 294.95/295.10 as against 296.05/296.15 the previous day.

The total USD/LKR traded volume for 8 January was $ 63.78 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)