Thursday Jun 11, 2026

Thursday Jun 11, 2026

Monday, 22 January 2024 00:43 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

By Wealth Trust Securities

In the secondary bond market, trading commenced the week ending 19 January on a subdued note. However, activity was seen increasing during the latter part of the week as considerable buying interest was observed on the short to medium durations. This in turn saw yields decline quite drastically. This was against the backdrop of an announcement of three auctions by the Domestic Operations Department (DOD) of CBSL for outright purchases of 15.05.26, 01.06.26 and 01.08.2026 maturities, last Friday. However, all offers were rejected by the CBSL at this round of auctions. Despite this development, yields were seen holding below the previous week’s levels. The demand was augmented by positive sentiments shared by the IMF delegation at the conclusion of their recent visit. As such, the yield curve was seen shifting down, week on week while continuing to remain flat across maturities.

Accordingly, the maturities of the three 25’s (15.01.25, 01.06.25, 01.08.25), three 26’s (01.02.26, 15.05.26 and 01.06.26), 15.09.27, two 28’s (15.03.28 and 01.07.28), 15.05.30 were seen trading between the ranges of 13.50% to 13.00%, 13.75% to 13.56%, 14.05% to 13.80%, 14.21% to 13.99% and 14.13% to 13.90% respectively, with considerable volumes being transacted towards the latter part of the week.

At last week’s Treasury bill auction, the weighted averages on the 91 day and 182-day bills were seen dipping below 14.00% for the first time since end March 2022 after hovering within the range of 14.00% to 15.00% for the past 11 weeks. The 91-day bill recorded a steep decline of 36 basis points to 13.91%, its eighth consecutive week of easing, while the 182-day dipped by 26 basis points to 13.83%, keeping in line with the declining trajectory of market interest rates. However, the 364-day bill registered only a marginal reduction of 1 basis point to 12.92%. The total bids received exceeded the total offered amount by 3.01 times. As such, the entire total offered amount of Rs. 95.00 billion was raised at the 1st phase of the auction, while an additional amount of Rs. 21.83 billion was raised only on the 364-day maturity.

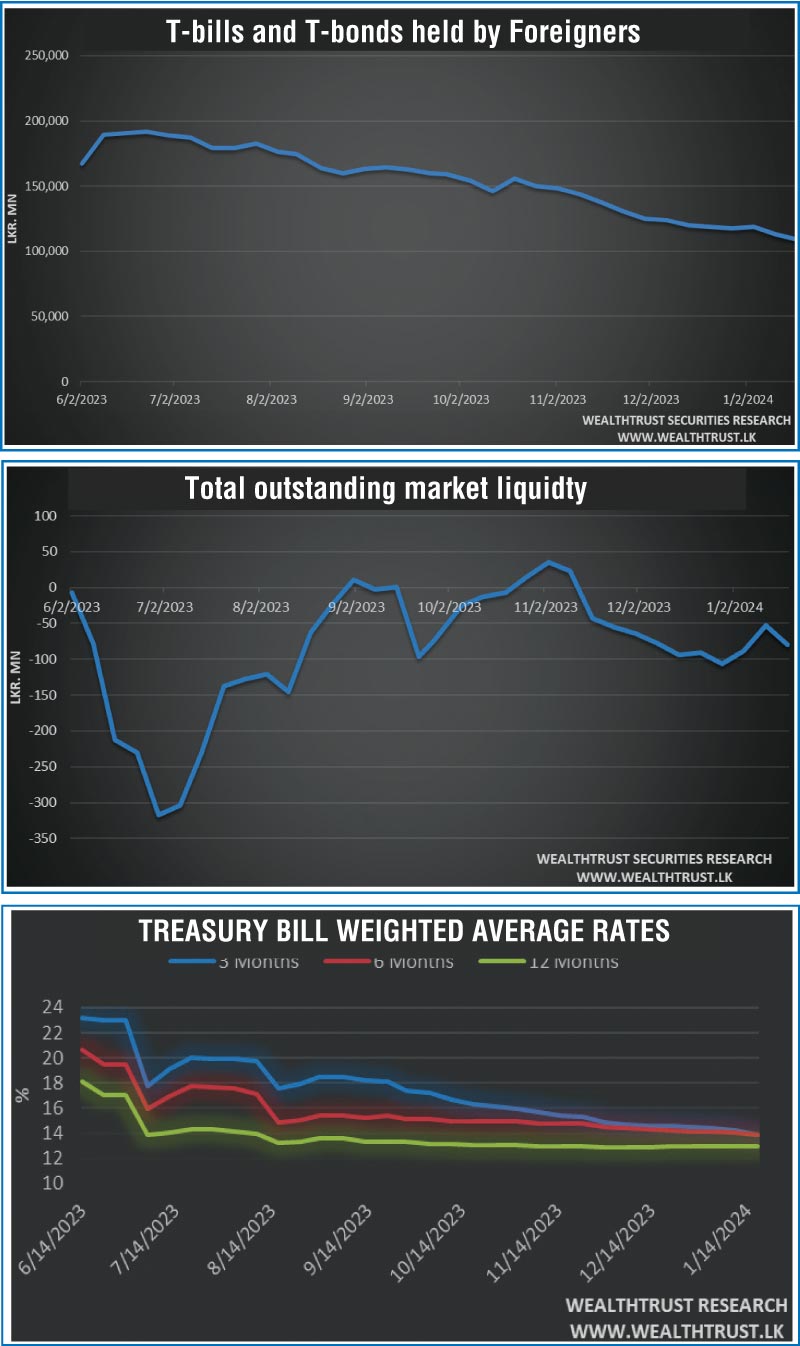

The foreign holding in Rupee bonds and bills recorded a net outflow for a second consecutive week. The week ending 18 January outflow was Rs. 4.06 billion, while the total holding stood at Rs. 108.94 billion.

The daily secondary market Treasury bond/bill transacted volumes for the first three days of the week averaged at Rs. 34.31 billion.

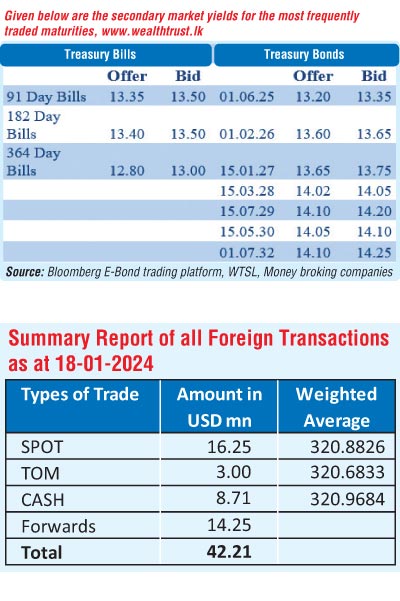

In money markets, the total outstanding liquidity deficit increased to Rs. 79.27 billion by the week ending 19 January from its previous week’s deficit of Rs. 53.29 billion. The Domestic Operations Department (DOD) of Central Bank continued to inject liquidity during the week by way of overnight and term reverse repo auctions at weighted average yields ranging from 9.08% to 10.68%.

The Central Bank of Sri Lanka (CBSL) holding of Gov. Securities was registered at Rs. 2,753.62 billion, unchanged against its previous week’s level.

In the Forex market, the USD/LKR rate on spot contracts was seen appreciating during the week to close at Rs.320.20/320.40. This is as against its previous weeks closing level of Rs. 322.10/322.20 and subsequent to trading at a high of Rs. 322.10 and a low of Rs. 320.35.

The daily USD/LKR average traded volume for the first three trading days of the week stood at $ 75.07 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)