Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Monday, 8 July 2024 01:22 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

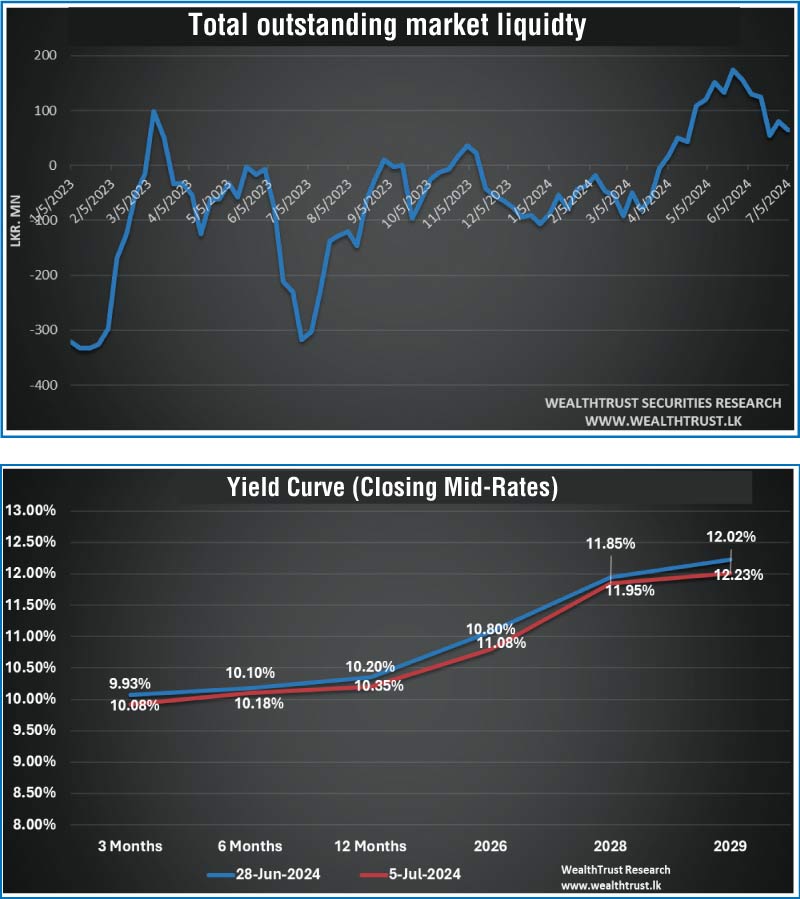

The secondary bond market last week was characterised by renewed buying interest, buoyed by the news that Sri Lanka has reached a debt restructuring deal agreement with its International Sovereign Bondholders. The group holds a significant component of the nation’s external debt commitment. The terms help pave the way to achieving debt sustainability, improving fiscal space and restoring confidence in the international community such as continued IMF support, credit ratings and foreign capital market access. This was augmented by the T-bill auction results, which some market participants were observed reading as a turning point in the recent spike in yields. The market rallied throughout the week, with yields declining on the back of healthy activity and transaction volumes. However, by the end of the week, activity dropped significantly, leading to yields consolidating at the newly established levels. As a result, the yield curve shifted downwards slightly by the close of the week.

The secondary bond market last week was characterised by renewed buying interest, buoyed by the news that Sri Lanka has reached a debt restructuring deal agreement with its International Sovereign Bondholders. The group holds a significant component of the nation’s external debt commitment. The terms help pave the way to achieving debt sustainability, improving fiscal space and restoring confidence in the international community such as continued IMF support, credit ratings and foreign capital market access. This was augmented by the T-bill auction results, which some market participants were observed reading as a turning point in the recent spike in yields. The market rallied throughout the week, with yields declining on the back of healthy activity and transaction volumes. However, by the end of the week, activity dropped significantly, leading to yields consolidating at the newly established levels. As a result, the yield curve shifted downwards slightly by the close of the week.

Accordingly, the 2026 tenors of 01.06.26 and 01.08.26 were seen moving down to intraweek lows of 10.70% from highs of 10.80% at the start of the week. The 2028 tenors followed suit, as the 15.02.28, 15.03.28 and 01.05.28 maturities were seen hitting intraweek lows of 11.82% from intraweek highs of 12.00%. Similarly, the 15.09.29 maturity was observed dropping to a low of 12.00% from highs of 12.15% at the start of the week. Additionally, the medium tenor 15.05.30 and 01.12.31 maturities were seen changing hands at the rate of 12.15%.

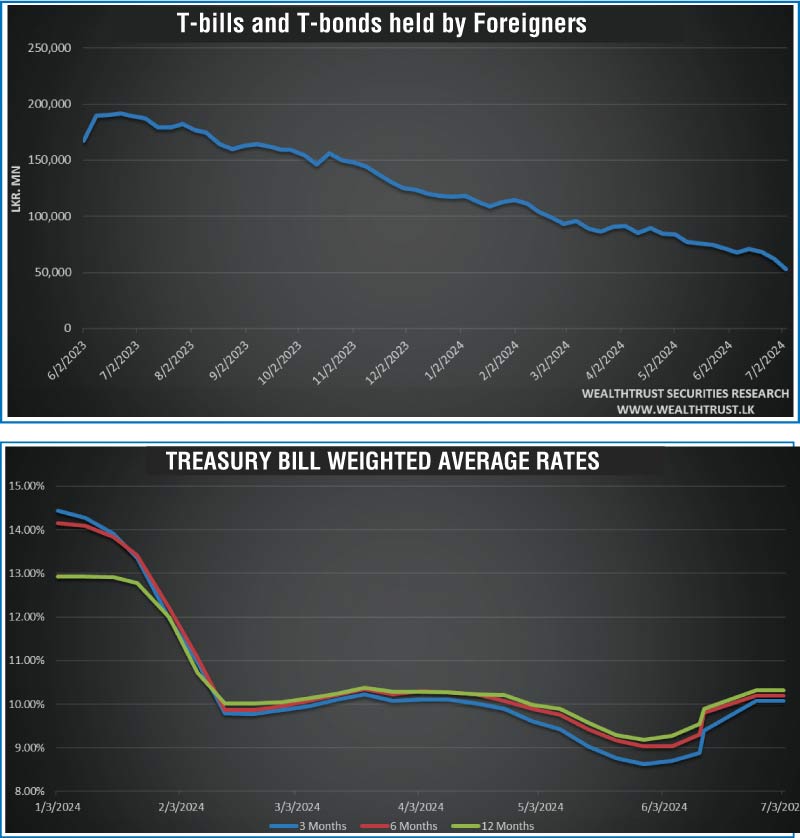

At the weekly Treasury bill auction conducted last Wednesday (3), the weighted average rates remained unchanged, after four consecutive weeks of increases. The yield on the 91-day maturity was recorded at 10.07%, the 182-day maturity at 10.19%, and the 364-day maturity at 10.31%.

The foreign holding in rupee Treasuries for the week ending 4 July 2024, recorded a net outflow for a third consecutive week to the tune of Rs. 8.98 billion. As a result, the overall holding was registered at Rs. 53.07 billion, dropping to the lowest level since a peak of Rs. 191.91 billion in June of 2023 (a reduction of over 70%).

The daily secondary market Treasury bond/bill transacted volumes for the first two days of the week averaged at Rs. 30.34 billion.

In money markets, the total outstanding liquidity surplus decreased to Rs. 64.98 billion by the week ending 28 June from its previous week’s surplus of Rs. 80.39 billion. The Domestic Operations Department (DOD) of Central Bank injected liquidity during the week by way of overnight reverse repo auctions and 7-day term reverse repos at weighted average rates of 8.62% to 8.93%. The weighted average interest rate on call money and repo ranged between 8.75% to 8.78% and 8.97% to 9.14% respectively.

The Central Bank of Sri Lankas (CBSL) holding of Government Securities was registered at Rs. 2,595.62 billion as at 28 June 2024, unchanged from the previous week’s level.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts was seen appreciating during the week to close at Rs. 304.45/304.75, despite some volatility. This is as against its previous week’s closing level of Rs. 306.00/306.20 and subsequent to trading at a high of Rs. 302.20 and a low of Rs. 306.07.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 76.25 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)