Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Tuesday, 21 May 2024 00:00 - - {{hitsCtrl.values.hits}}

Rs.160 b on offer on T-bills; Rupee steady

By Wealth Trust Securities

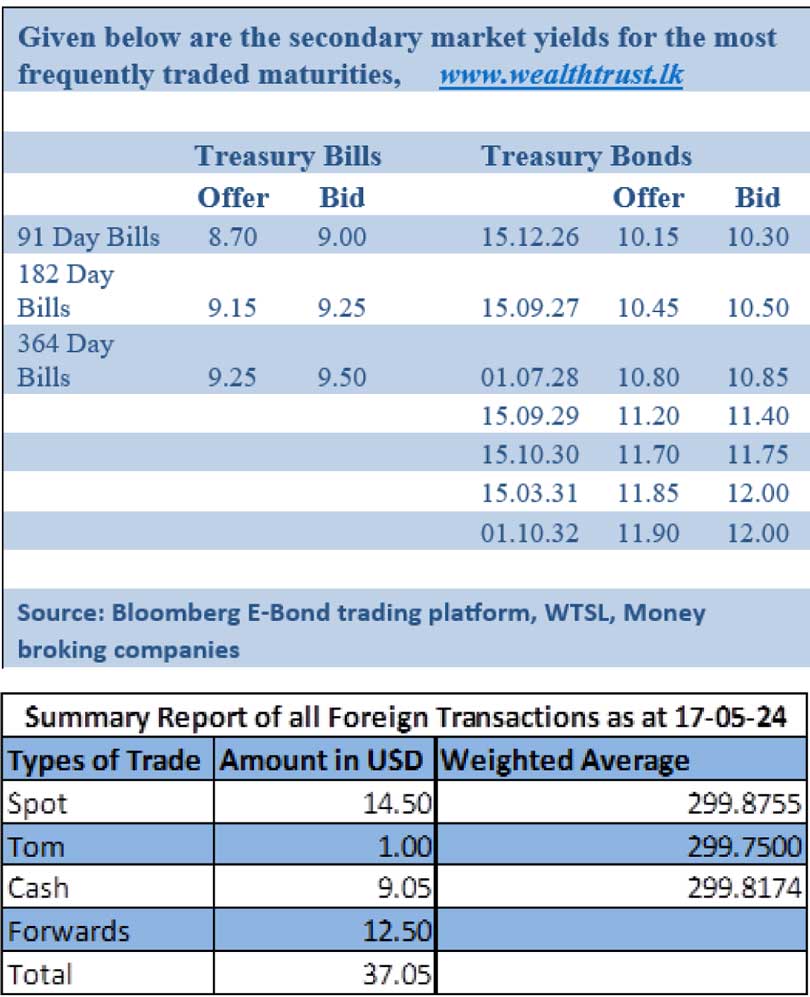

The secondary bond market on 20 May 2024 kicked of the week on a dull note, with moderate transaction volumes and yields edging up on continued selling interest. Trading as usual centred on the short to medium end of the yield curve with a specific emphasis on 2026 to 2032 durations.

In particular the liquid 15.12.26 maturity, saw yields move up to an intraday high of 10.20% against its previous day’s closing level of 10.10/15. While the 01.02.26 and 01.08.26 maturity traded at highs of 10.00% and 10.10% respectively. Similarly, the popular 2028 tenor experienced yields increasing, with the shorter tenor 2028 maturities of 15.03.28 and 01.05.28 trading at 10.75%. While the relatively longer tenor 01.07.28 hit an intraday high of 10.90% as against an opening low of 10.81%. Trades were also observed on the 2027 tenors (i.e. 01.05.27 and 15.09.27), hitting intraday high of 10.49% from intraday low of 10.45%. In addition, trades were seen on the relatively longer tenor bonds of 15.05.30/15.10.30 and 01.10.32 at the rate of 11.61% to 11.70% and 11.90% to 11.95% respectively.

This is ahead of today’s weekly Treasury bill auction, where a total amount of Rs. 160 billion is on offer, a reduction of Rs. 17.5 billion over its previous week. This will consist of Rs. 25 billion on the 91-day maturity, Rs. 65 billion on the 182-day maturity and further Rs. 70 billion on the 364-day maturity. At last week’s auction, weighted average rates decreased across the board for a sixth consecutive week by 39 basis points and 33 basis points each to 9.04%, 9.43% and 9.57% on the three maturities respectively. The total offered amount of Rs. 177.50 billion was accepted at the 1st phase of the auction while a further amount of Rs. 17.75 billion was raised at its phase II.

The total secondary market Treasury bond/bill transacted volume for 17 May was Rs. 23.91 billion.

In money markets, the weighted average rate on overnight call money was at 8.64% and repo was at 8.68%.

The net liquidity surplus stood at Rs. 134.53 billion yesterday as an amount of Rs. 0.20 billion was withdrawn from Central Banks SLFR (Standard Lending Facility Rate) of 9.50% against an amount of Rs. 154.73 billion deposited at Central Banks SDFR (Standard Deposit Facility Rate) of 8.50%.

Further, the DOD (Domestic Operations Department) of Central Bank injected liquidity by way of a 7-day term reverse repo auction for Rs. 20.00 billion at the weighted average rates of 8.84%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts closed the day steady at Rs. 299.60/299.75 against its previous day’s closing level of Rs. 299.60/299.70.

The total USD/LKR traded volume for 17 May was $ 37.05 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)