Tuesday Jun 23, 2026

Tuesday Jun 23, 2026

Friday, 9 August 2024 00:45 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

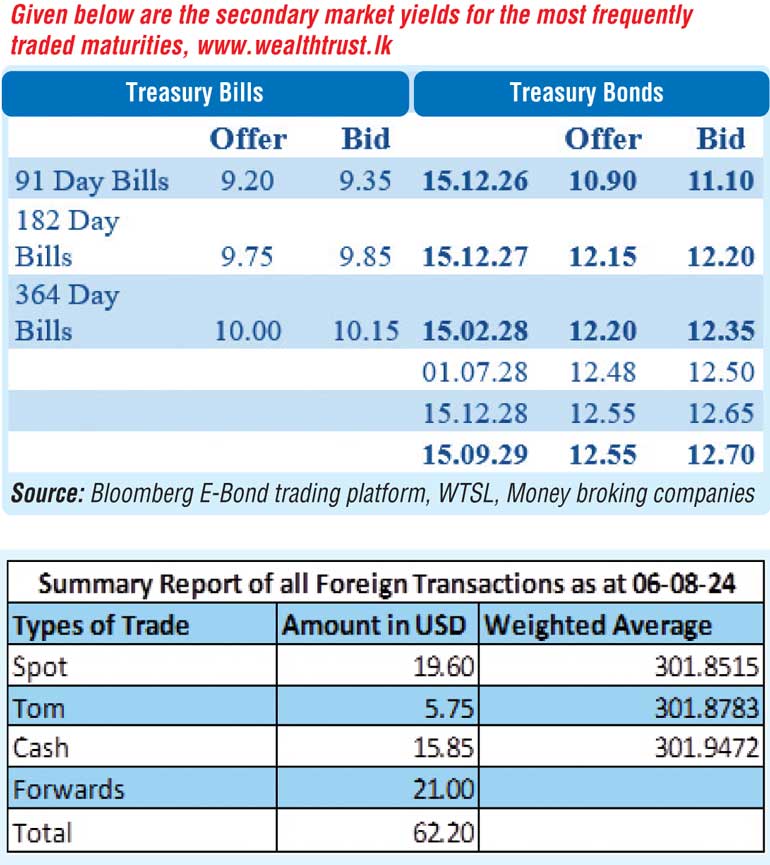

The secondary bond market yesterday continued on a bearish trajectory, with yields overall increasing further. In particular, the shorter tenor bonds (2026-2027 durations) adjusted, experiencing a steep increase. Meanwhile the medium tenor 2028 durations were seen holding stable. However, the longer tenor bonds (durations 2029 and beyond) saw activity at a standstill, as two-way quotes widened. In conclusion, the yield curve was seen flattening at the elevated levels.

The secondary bond market yesterday continued on a bearish trajectory, with yields overall increasing further. In particular, the shorter tenor bonds (2026-2027 durations) adjusted, experiencing a steep increase. Meanwhile the medium tenor 2028 durations were seen holding stable. However, the longer tenor bonds (durations 2029 and beyond) saw activity at a standstill, as two-way quotes widened. In conclusion, the yield curve was seen flattening at the elevated levels.

Accordingly, the yield on the 01.08.26, 15.01.27, 01.05.27 and 15.12.27 maturities were seen increasing to the considerably elevated levels of 10.75% to 10.80%, 11.00% to 11.12%, 11.80% and 12.10% to 12.30% respectively. However, yields on the 2028 tenors were seen holding broadly steady as the 01.07.28 maturity was trading within the range of 12.45% to 12.50%. Overall activity was muted, and transaction volumes were relatively low.

In the secondary bills market, the March (close to six months) and July (close to one year) 2025 maturities were seen transacting at the rate of 9.80% to 9.89% and 10.10% respectively. These levels are above the weighted average rates recorded at this week’s Treasury bill auction.

The details of the upcoming Rs. 60.00 billion Treasury bond auction scheduled for the 13 August (next week) were announced. The auction will comprise of Rs. 45.00 billion from a new 15 June 2029 maturing bond bearing a coupon of 11.75% and Rs. 15.00 billion from the 1 October 2032 maturity bearing a coupon of 9.00%.

The total secondary market Treasury bond/bill transacted volume for 7 August was Rs. 110.90 billion.

In money markets, the weighted average rate on overnight call money was at 8.56% and repo was at 8.80%.

The net liquidity surplus stood at Rs. 80.20 billion yesterday as an amount of Rs. 101.30 billion was deposited at Central Banks SDFR (Standard Deposit Facility Rate) of 8.25% vs an amount of Rs 1.10 billion been withdrawn from the Central Banks SLFR (Standing Lending Facility Rate) of 9.25%.

Further, the DOD (Domestic Operations Department) of the Central Bank injected liquidity by way of an overnight reverse repo auction for Rs. 20.00 billion at a weighted average rate of 8.55%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts appreciated further to close the day at Rs. 300.80/301.05 against its previous day’s closing level of Rs. 301.55/301.65.

The total USD/LKR traded volume for 6 August was $ 62.20 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)