Tuesday Feb 24, 2026

Tuesday Feb 24, 2026

Wednesday, 11 December 2024 00:12 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

By Wealth Trust Securities

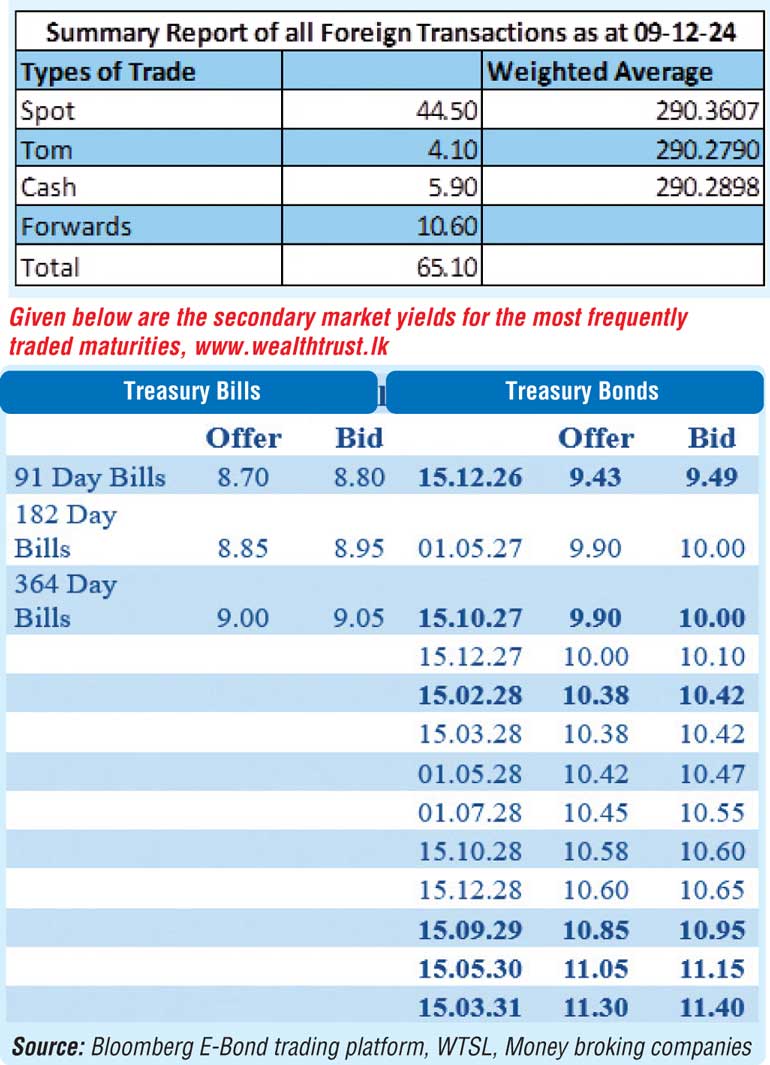

The Secondary Bond Market yesterday saw yields drop on the back of renewed buying interest that was supported by robust trading activity and transaction volumes.

The 2027s saw strong demand that pushed the yields on the 15.10.27 and 15.12.27 maturities from intraday highs to lows of 10.05%-9.94% and 10.10%-10.05% respectively. The 2028 tenors followed suit with the yield on the 15.02.28, 01.05.28 and 15.10.28 maturities declining from intraday highs to lows of 10.45%-10.38%, 10.60%-10.45%, and 10.62%-10.60% respectively. The 15.09.29 maturity traded within the range of 10.90%-10.85%. Additionally, trades were observed on the medium tenor 15.05.30 maturity down the range of 11.17%-11.10%.

This comes ahead of the Treasury bill auction due today, which will have a total amount of Rs. 206.00 billion on offer, an increase of Rs. 13.50 billion over the previous week. This will consist of Rs. 76.00 billion on the 91-day maturity and Rs 90.00 billion on the 182-day and Rs. 40.00 billion on the 364-day maturity.

For reference, at the weekly Treasury bill auction conducted last Wednesday (04 December), weighted average rates were seen holding broadly steady. This followed 3 consecutive weeks of decline on all three maturities prior. Accordingly, the weighted average rates on the 91-day tenor remained unchanged at 8.73% and the 364-day tenor at 9.08%. However, the weighted average yield on the 182-day tenor declined by 03 basis points to 8.94%. Total bids received exceeded the offered amount by 2.09 times, and the entire Rs. 192.50 billion on offer was successfully raised at the 1st phase.

The total secondary market Treasury bond/bill transacted volume for 09 December was Rs. 14.69 billion.

In money markets, the weighted average rates on overnight call money and Repo stood at 8.04% and 8.16% respectively. The DOD (Domestic Operations Department) of the Central Bank injected liquidity by way of an overnight and 7-day term reverse repo auctions for Rs. 5.21 billion and Rs. 36.70 billion at the weighted average rate of 8.05% and 8.12% respectively.

The net liquidity surplus stood at Rs. 188.91 billion yesterday. No funds were withdrawn from the Central Banks SLFR (Standing Lending Facility Rate) of 8.50%, while an amount of

Rs. 230.81 billion was deposited at the Central Banks SDFR (Standard Deposit Facility Rate) of 7.50%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts closed the day appreciating marginally to

Rs. 290.30/290.35 as against 290.30/290.45 the previous day.

The total USD/LKR traded volume for 09 December was

$ 65.10 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)