Monday Feb 23, 2026

Monday Feb 23, 2026

Monday, 21 October 2024 00:28 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

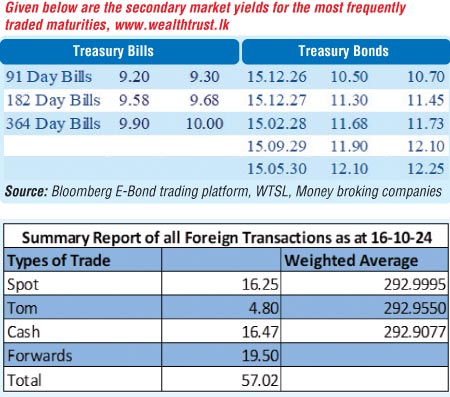

The Secondary bond market during the week ending 18 October, started off bullish with yields initially declining on buying interest. However, as the week progressed, profit-taking pressures caused yields to edge up, erasing earlier gains and ultimately leading to a reversal. As a result, at the close of the week, two-way quotes were seen registering a marginal week-on-week increase.

The Secondary bond market during the week ending 18 October, started off bullish with yields initially declining on buying interest. However, as the week progressed, profit-taking pressures caused yields to edge up, erasing earlier gains and ultimately leading to a reversal. As a result, at the close of the week, two-way quotes were seen registering a marginal week-on-week increase.

The 15.12.27 maturity was seen trading up from an intraweek low of 11.185%, at the start of the week, to an intraweek high of 11.35%. The rest of the yield curve followed suit. The popular and liquid 15.02.28 and 15.03.28 maturities saw yields increase from an intraweek low of 11.43% to a high of 11.75%. The relatively longer 2028 tenors of 01.07.28 and 15.12.28, saw rates move up from 11.50%-11.82% and 11.60%-11.80% respectively. The yield on the 15.09.29 maturity increased to an intraweek high of 11.90% from a low of 11.70%. Additionally, trades were seen on the medium tenor 15.05.30 maturity at the rates of 12.00%-12.15%.

In conclusion, at the close of the week the yield curve registered a slight upward shift.

In contrast, at the weekly Treasury bill auction held last Wednesday: yields were seen declining for the fourth consecutive week, mirroring the downward trajectory in the secondary T-bill market. The weighted average rates across all 3 tenors fell below 10.00%, dropping to levels last seen in late-July this year. Accordingly, the weighted average rate for the 91-day tenor dropped by 37 basis points to 9.32%, while the 182-day tenor decreased by 30 basis points to 9.65%. The 364-day tenor also saw a relatively marginal decline of 5 basis points, bringing the rate to 9.95%. Total bids received exceeded the offered amount by 2.62 times, and the entire Rs. 97.00 billion on offer was successfully raised at the 1st phase.

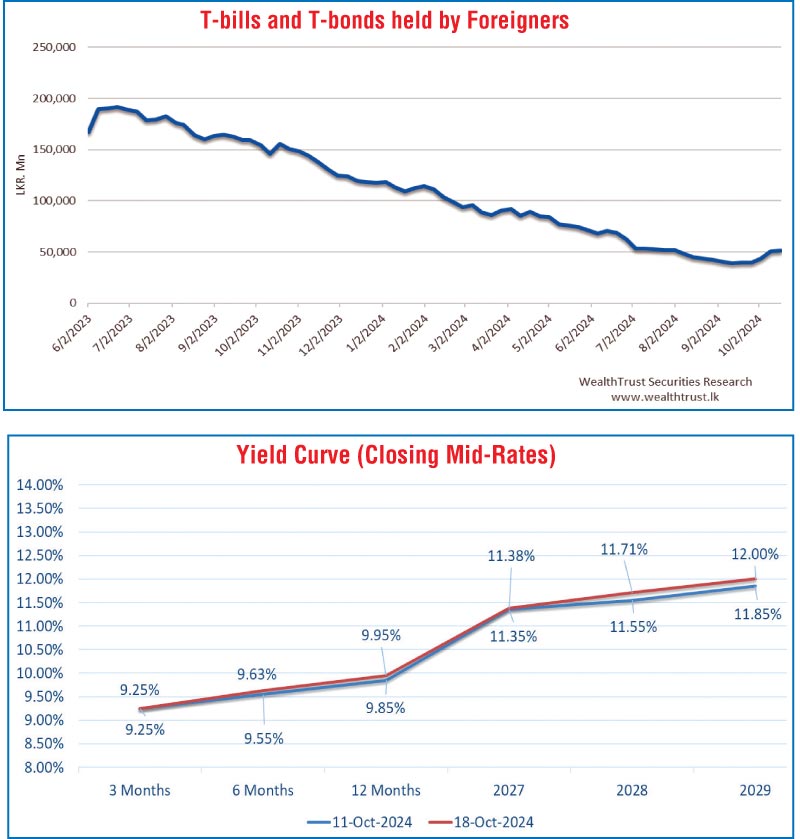

For the week ending 17 October 2024, the foreign holdings in Sri Lankan rupee-denominated Treasury securities saw a net inflow of Rs. 495 million. This marked the fifth consecutive week of positive inflows. As a result, total foreign holdings reached Rs. 51.14 billion – a 0.98% increase compared to the previous week.

The daily secondary market Treasury bond/bill transacted volumes for the first three days of the week averaged at Rs. 16.41 billion.

In money markets, total outstanding liquidity dipped marginally to Rs. 78.10 billion by the end of the week ending 18 October, down from Rs. 81.83 billion recorded the previous week. The Domestic Operations Department (DOD) of Central Bank injected liquidity during the week by way of overnight reverse repo auctions and a 7-day term reverse repo auctions at weighted average rates of 8.41% to 8.61% respectively. The weighted average interest rate on call money and repo ranged between 8.51% to 8.58% and 8.65% to 8.77% respectively.

The Central Bank of Sri Lankas (CBSL) holding of Government Securities was registered at Rs. 2,515.62 billion as at 18 October 2024, unchanged from the previous week’s level.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts was seen depreciating slightly, to close the week at Rs. 293.00/293.20 as against its previous week’s closing level of Rs. 292.75/292.95 and subsequent to trading at a high of Rs. 292.70 and a low of Rs. 294.40.

The daily USD/LKR average traded volume for the first three trading days of the week stood at $ 58.51 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)