Tuesday Feb 10, 2026

Tuesday Feb 10, 2026

Monday, 18 June 2018 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

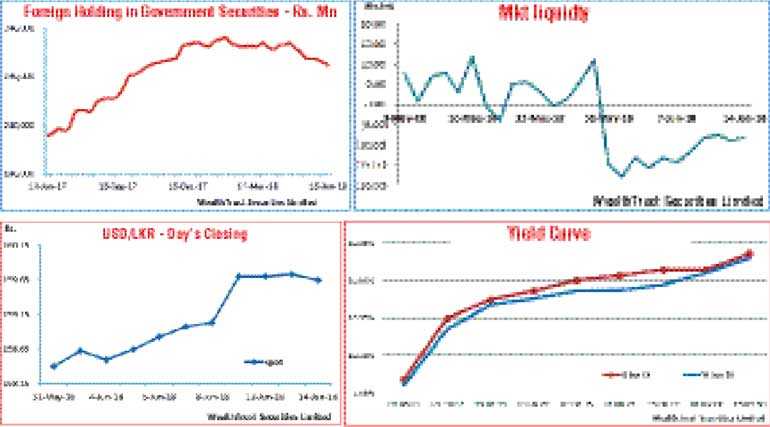

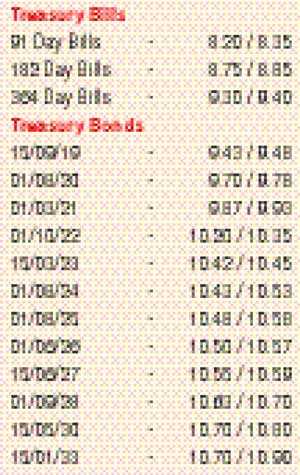

The secondary market bond yields were seen decreasing across the yield curve during the week ending 14 June 2018, driven by the outcome of the weekly Treasury bill auction, which saw the weighted average on the 364 day bill decrease for a third consecutive week to hit a seventeen week low of 9.44%.

On the short end of the curve, the 01.07.19 and 01.03.21 maturities were seen changing hands within weekly highs of 9.55% and 9.95% respectively to lows of 9.37% and 9.88% while on the belly end of the curve, the 15.03.23 changed hands within a high of 10.45% to a low of 10.40%. On the long end of the curve, the 01.09.28 and 15.05.30 maturities were seen dipping to weekly lows of 10.60% and 10.72% respectively against its highs of 10.75% and 10.80%. In the secondary bill market, April, May and June 2019 maturities were traded within the range of 9.25% to 9.37%.

However, foreign investors were seen as net sellers of Rupee bonds for a seventh consecutive week, recording an outflow of Rs. 2.72 billion for the week ending 13 June 2018.

The daily secondary market Treasury bond/bill transacted volumes for the first three days of the week averaged Rs. 10.72 billion.

In money markets, the overnight call money and repo rates increased to average at 8.35% and 8.39% respectively for the week as the average net liquidity shortfall in the system stood at Rs. 8.32 billion for the week. The OMO Department of the Central Bank of Sri Lanka continued to conduct overnight Reverse Repo auctions throughout the week in order to infuse liquidity at weighted averages of 8.49% to 8.50%.

Rupee dips during the week

The value of rupee was seen decreasing considerably during the week to levels of Rs. 159.95/00 on the back of continued importer demand but bounced back marginally to close the week at Rs. 159.60/70 against its previous weeks closing of Rs.158.95/10. The daily USD/LKR average traded volume for the first three days of the week stood at $ 78.85 million.

Some of the forward dollar rates that prevailed in the market were one month – 160.35/55; three months – 161.95/15 and six months – 164.25/45.