Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Monday, 6 November 2023 00:01 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary bond market commenced the trading week ending 3 November with a slight uptick in activity subsequent to the bond auction while yields were seen closing the week broadly steady.

The secondary bond market commenced the trading week ending 3 November with a slight uptick in activity subsequent to the bond auction while yields were seen closing the week broadly steady.

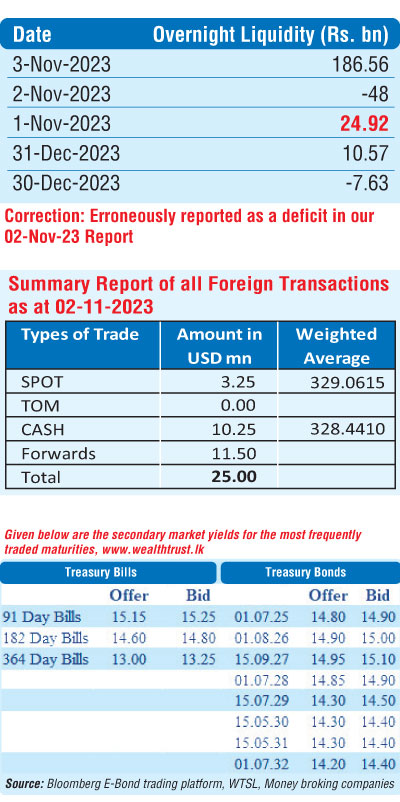

On Tuesday however, yields declined marginally with an increase in activity across the yield curve on the back of sizeable volumes changing hands with a particular emphasis on the short tenures. For instance, the 15.09.27 and 01.07.28 maturities were seen hitting intraweek lows of 14.85% and 14.80% respectively from its intraweek highs of 15.00% and 15.10%. Similarly, Wednesday also continued to see heavy trading activity but yields held steady and edged up once again by the end of the week while activity moderated. Trading was seen on the other liquid maturities of the two 25’s (01.06.25 and 01.07.25), two 26’s (01.06.26 and 01.08.26), 15.07.29 and 15.05.30 within the ranges of 15.05% to 14.80%, 15.00% to 14.90%, 15.00% to 14.40% and 14.40% to 14.25% respectively as well.

The Treasury bond auctions conducted last Monday, 30 October, saw all bids rejected for the first time in over 19 months, or since the round of auctions conducted on 29 March 2022. This was despite the auction receiving total bids amounting to Rs. 91.99 billion as against an offered amount of Rs. 45.00 billion.

At last week’s Treasury bill auction, continued demand for the 91-day bill saw its weighted average drop by a further 17 basis points to 15.93% while the 182-day bill and 364-day bill weighted average rates remained unchanged at 14.93% and 13.02% respectively. An amount of Rs. 138.58 billion or 95.57% was raised of the total offered amount of Rs. 145 billion at the 1st phase of the auction while a further 42.67 billion was raised at the 2nd phase of the auction on the 91-day and 364-day maturities at their respective weighted averages determined at the 1st phase.

Meanwhile, in secondary market bills, November/December 2023 maturities were seen traded within the range of 15.00% to 14.10%, whereas, January, February/March and May 2024 maturities changed hands at 15.30% to 15.17%, 15.70% to 15.25% and 14.90% levels respectively.

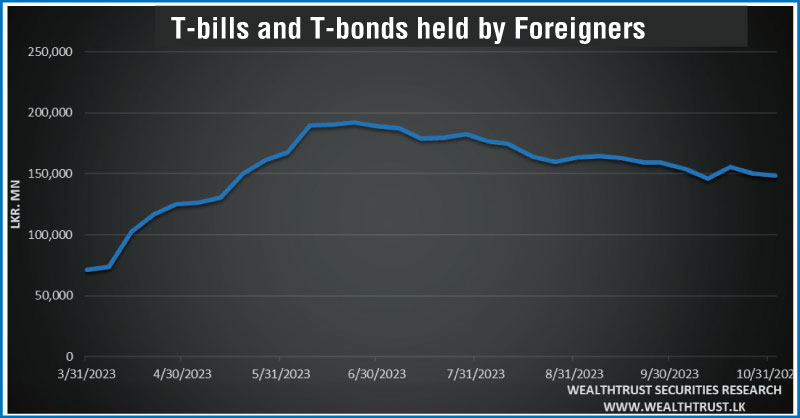

The foreign holding in Rupee bonds and bills continued to decline for a second consecutive week, with a net outflow of Rs. 1.89 billion, bringing the total holding to stand at Rs. 148.36 billion as at 2 November 2023.

The daily secondary market Treasury bond/bill transacted volumes for the first four days of the week averaged at Rs. 32.96 billion.

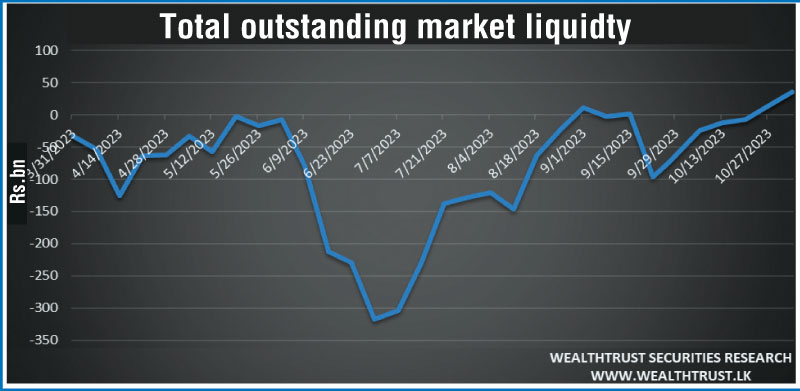

In money markets, the total outstanding liquidity recorded a surplus of Rs. 35.51 billion by the week ending 3 November from its previous week’s surplus of Rs. 15.33 billion. The Domestic Operations Department (DOD) of Central Bank continued to inject liquidity during the week by way of overnight Reverse repo auctions at weighted average yields ranging from 10.08% to 10.16%.

The Central Bank of Sri Lanka’s (CBSL) holding of Government Securities was registered at Rs. 2,839.35 billion, unchanged against its previous week’s level.

In the forex market, the USD/LKR rate on spot contracts was seen depreciating during the week to close the week at Rs. 329.00/330.00 against its previous weeks closing level of Rs. 327.20/327.40, subsequent to trading at a high of Rs. 327.34 and a low of Rs. 329.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 62.02 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)