Tuesday Feb 17, 2026

Tuesday Feb 17, 2026

Wednesday, 12 June 2024 00:26 - - {{hitsCtrl.values.hits}}

Banks are going obsolete

As the new platforms become further integrated into the everyday lives of consumers, traditional brick-and-mortar financial institutions will become increasingly obsolete.

As the new platforms become further integrated into the everyday lives of consumers, traditional brick-and-mortar financial institutions will become increasingly obsolete.

The digital age

While the fundamental principles of banking have not changed – accepting deposits, issuing loans, and providing financial services – the way those services are delivered has changed dramatically. Traditional banks rely on physical branches to conduct transactions and provide advice to consumers. However, with digital financial tools now at the fingertips of consumers, traditional banks must adapt, or risk being left behind. One key factor that will shape the future of banking is the emergence of digital financial services such as mobile payments and online banking. These technologies enable customers to access their accounts anytime, anywhere, eliminating the need for them to physically visit a bank branch or ATM.

Blockchain technology and AI

A blockchain is “a distributed database that maintains a continuously growing list of ordered records, called blocks.” These blocks “are linked using cryptography. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data.

One example of how banks are adapting is by offering digital wallets powered by blockchain technology. These services allow customers to store their funds securely while they easily transfer money between accounts. The use of mobile apps also allows customers to access their accounts anytime, anywhere – eliminating the need to visit a physical branch or wait in line at an ATM. For the people who prefer the convenience of digital banking options over dealing with brick-and-mortar establishments, this is a welcome change.

Another important trend that will shape the future of banking is artificial intelligence (AI). AI allows banks to automate routine tasks such as fraud detection, account management, and customer service, enabling them to save time and money while also providing more accurate results. AI can also be used to provide personalised consumer experiences that are tuned to the needs and interests of everyone. By leveraging data from customers’ past transactions and interactions with the bank, AI can provide more relevant advice on topics such as budgeting and saving for retirement.

Changes in consumer demand

In addition to these technological advancements in banking products and services, customer expectations have shifted as well. Today’s consumers demand faster transaction times, lower fees, individualised attention, and more transparency when it comes to their finances. Many traditional banks have failed to meet these expectations due to outdated technology or outmoded policies that cannot keep up with customer demands. As a result, more consumers are turning to alternative banking solutions that provide the ease they need without sacrificing security or service quality.

The increasing demand for personalised services has spurred a surge in what are known as ‘challenger banks’. These digital-only banks can provide customers with highly tailored products and services due to their lack of physical branches. They are often faster and cheaper than traditional institutions when it comes to transferring money or setting up accounts due to their reliance on smartphone apps rather than physical infrastructure.

It remains unclear whether traditional banking will become extinct soon; however, what is certain is that its role will continue to evolve if it is going to survive in this ever-changing landscape of finance. Banks must continue embracing digital technologies and customer feedback so they can provide innovative products and services tailored for today’s customers’ needs. Doing so may prove integral for them staying competitive in an increasingly tech-driven world.

The US dollar may lose its demand with the advent of new ways of settlements in international trade propelling out of the sanctions against Russia by the west. Introduction of a BRICS currency and bilateral trade settlement using Gold or Chinese Yuan as a common denominator already has started. Use of US Dollar as the base currency for international trade is slowly ending.it used to be Dutch Guilders which gave way to the British Pound and with the ending of the 2nd world war the US Dollar became the base currency used for international trade and that too is about to change. No one would want to hold on to a bunch of Fiat Currency any more.

The Federal Reserve Bank of United States is printing Dollars merrily to service their 32 trillion and counting Public Debt. The Fed can keep doing it hence US Dollar is like most other currencies in the world is a Fiat Currency. Fiat money is a government-issued currency that is not backed by a physical commodity, such as gold or silver, but rather by the government that issued it. The value of fiat money is derived from the relationship between supply and demand and the stability of the issuing government, rather than the worth of a commodity backing it.

The Federal Reserve Bank of United States is printing Dollars merrily to service their 32 trillion and counting Public Debt. The Fed can keep doing it hence US Dollar is like most other currencies in the world is a Fiat Currency. Fiat money is a government-issued currency that is not backed by a physical commodity, such as gold or silver, but rather by the government that issued it. The value of fiat money is derived from the relationship between supply and demand and the stability of the issuing government, rather than the worth of a commodity backing it.

The BRICS currency will be backed by gold or perhaps by crude oil. Inclusion of South Africa and expected expansion of BRICS to other African countries producing valuable minerals and metals makes very evident that the birth of a commodity backed BRICS currency is eminent. With such commodity backed currency in circulation no Fiat currency would keep its head above water for that long and Federal Reserve Bank of America and their close allies, The European Central Bank and The Bank of England knows this and they will not go down without a fight. What is increasingly visible is an introduction of a digital currency by the European Union and North America abolishing all physical notes and coins issued by the respective governments.

With the introduction of the new Digital Currency every Central Bank will establish a Digital Wallet to every citizen of its country created with the Government issued ID number or the Social Security and for businesses with their Tax Identification Number. The Government would find it much easier and cost effective to deduct taxes at source and they will be happy to take all the fees that the banks made out of their customer base for performing transfers and payments.

Today even processing loans unless it is security based and mortgages are involved are done with electronic documents, electronically signed. So many virtual institutions like “cash App” are used by millions of people to transfer money between accounts and payments for utilities. This paints a grim picture of the future of banks. With availability of a digital wallet services offered by the Central Bank of a country no one would want to open a digital wallet with a regular commercial bank. Banks are going obsolete. The banks have additional worries of over exposed public debt portfolios which exponentially expand their risk with even the biggest economies getting their bond ratings slashed by rating organisations.

The recent banking crisis in America is a classic example. Over a period of just two days in March 2023, the Silicon Valley Bank (SVB) went from “solvent” to “broke” as depositors rushed to SVB to withdraw their funds, resulting in federal regulators closing the bank for good on 10 March 2023. SVB’s collapse marked the second largest bank failure in US history after Washington Mutual’s in 2008. Two days after that came the fall of Signature Bank of New York, the nation’s 29th largest bank, suggesting that the banking crisis had spread. In response, the US government took rapid and extraordinary steps to protect the financial system. The domino effect of Silicon Valley Bank collapse quickly expanded to Europe.

In mid-March 2023, Swiss bank UBS Group AG (UBS) bought rival Credit Suisse Group AG for 3 billion CHF (Swiss Francs, about $ 3.3 billion), a move intended to shore up the global banking system and prevent the latter financial institution from collapsing. This goes on to show even what used to be mighty strong Swiss banks too are not fully insulated from the risks of the modern day banks are facing. The readers should now abundantly understand that the banks what used to resemble safety, strength and integrity has lost all their values. Most banks are just trying to survive.

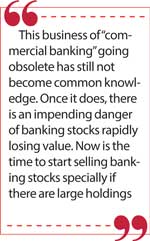

With all the above going on individuals, corporates and funds holding large strategic holdings of banking stocks are contemplating to sell off. Some major funds have already started offloading banking stocks which they held with long term prospects in mind. This business of “commercial banking” going obsolete has still not become common knowledge. Once it does, there is an impending danger of banking stocks rapidly losing value. Now is the time to start selling banking stocks specially if there are large holdings.

(The writer is a former currency strategist, commodity futures trader, technical analyst.)