Saturday May 02, 2026

Saturday May 02, 2026

Tuesday, 16 January 2024 01:06 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

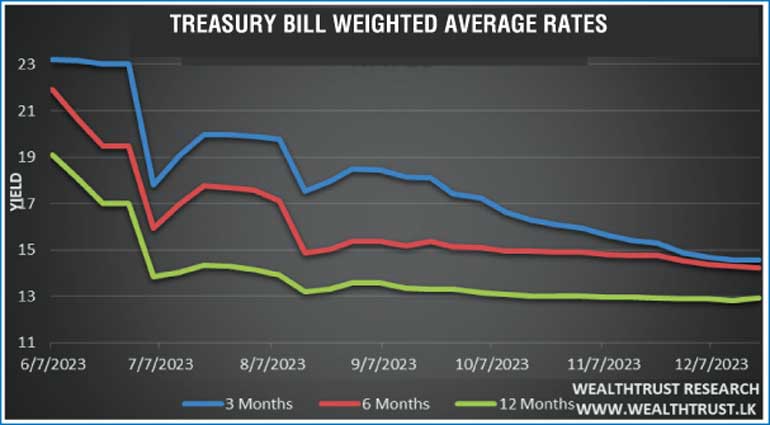

The secondary market yields on the 91-day and 182-day Treasury bills were seen trading below 14.00%, at levels of 13.50% to 13.75% last week for the first time since end March 2022, following its weekly auction.

The secondary market yields on the 91-day and 182-day Treasury bills were seen trading below 14.00%, at levels of 13.50% to 13.75% last week for the first time since end March 2022, following its weekly auction.

At the auction, the weighted average rate on the 91-day maturity declined for a seventh consecutive week, this time around by 18-basis points to 14.27%, while the 182-day maturity followed suit with a 7-basis point drop, while both maturities witnessed continued demand. However, the 364-day maturity remained unchanged at 12.93%, having remained static for three consecutive weeks. The total bids received exceeded the total offered amount by 2.65 times. The entire total offered amount of Rs. 100.00 billion was raised at the 1st phase of the auction, while an additional amount of Rs 3.09 billion was raised at the 2nd phase only on the 364-day maturity.

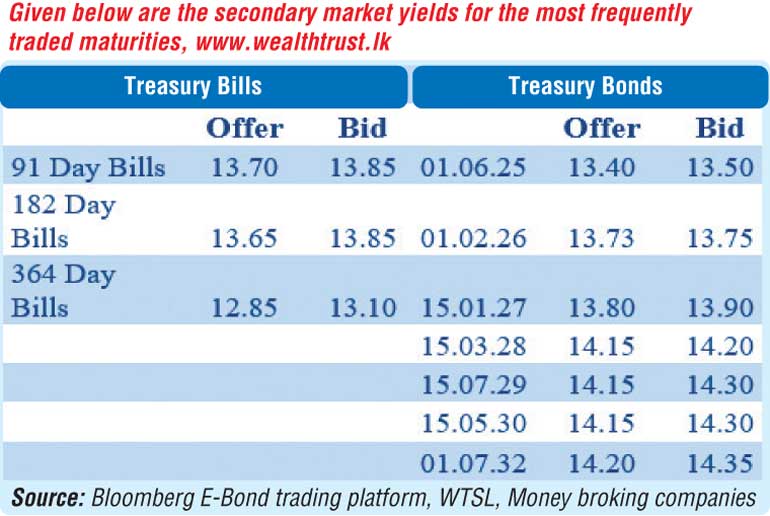

In the secondary bond market, trading commenced the week ending 12 January on a subdued note. However, activity was seen increasing during the latter part of the week as considerable buying interest was observed on the 2026 durations which saw its yields decline post bond auction. However, the rest of the yield curve remained broadly unchanged, as at the close of the week. Accordingly, the yields on the short to medium duration maturities of the two 25’s (15.01.25 and 01.07.25), four 26’s (01.02.26, 15.05.26, 01.06.26 and 01.08.26), 15.09.27 and two 28’s (01.07.28 and 15.03.28) and 15.05.30 were seen trading within the ranges of 13.50% to 13.35%, 13.90% to 13.72%, 14.15% to 14.05%, 14.28% to 14.05% and 14.15% respectively.

At the Treasury bond auctions conducted last Thursday, the outcome was positive, mainly on the short tenors at its 1st and 2nd phases, with the entire offered amount on the 2026 and 2028 durations being fully taken up. The 01.02.2026 maturity recorded a weighted average rate of 13.83%, a decline of 03 basis point since it was previously offered at the 12 December 2023 round of auctions, where the same three maturities were also offered.

At the Treasury bond auctions conducted last Thursday, the outcome was positive, mainly on the short tenors at its 1st and 2nd phases, with the entire offered amount on the 2026 and 2028 durations being fully taken up. The 01.02.2026 maturity recorded a weighted average rate of 13.83%, a decline of 03 basis point since it was previously offered at the 12 December 2023 round of auctions, where the same three maturities were also offered.

The 15.03.2028 recorded a weighted average rate of 14.21%, unchanged from the previous round. The weighted average on the 15.05.30 maturity also remained unchanged at 14.22%, however only Rs. 25.98 billion was raised out of an offered amount of Rs. 30.00 billion. The total bids received exceeded the total offered amount by 2.08 times. However, only Rs. 115.98 billion or 96.65% was accepted in total against a total offered amount of Rs. 120.00 billion.

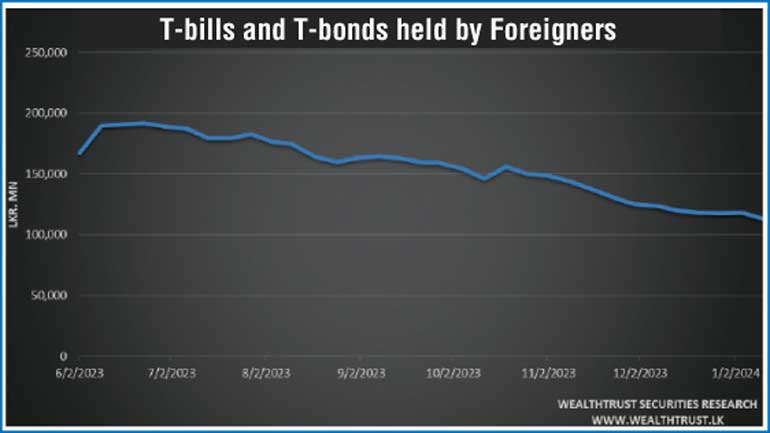

The foreign holding in Rupee bonds and bills recorded a net outflow to the tune of Rs. 5.45 billion for the week ending 11 January 2024 following an inflow last week, while the total holding stood at Rs. 113.00 billion.

The daily secondary market Treasury bond/bill transacted volumes for the first four days of the week averaged at Rs. 39.83 billion.

In money markets, the total outstanding liquidity deficit reduced to Rs. 53.29 billion by the week ending 12 January from its previous week’s deficit of Rs. 88.19 billion. The Domestic Operations Department (DOD) of Central Bank continued to inject liquidity during the week by way of overnight and term reverse repo auctions at weighted average yields ranging from 9.07% to 10.71%.

The Central Bank of Sri Lanka’s (CBSL) holding of Government Securities was registered at Rs. 2,753.62 billion, up against its previous week’s level of Rs. 2,743.62 billion.

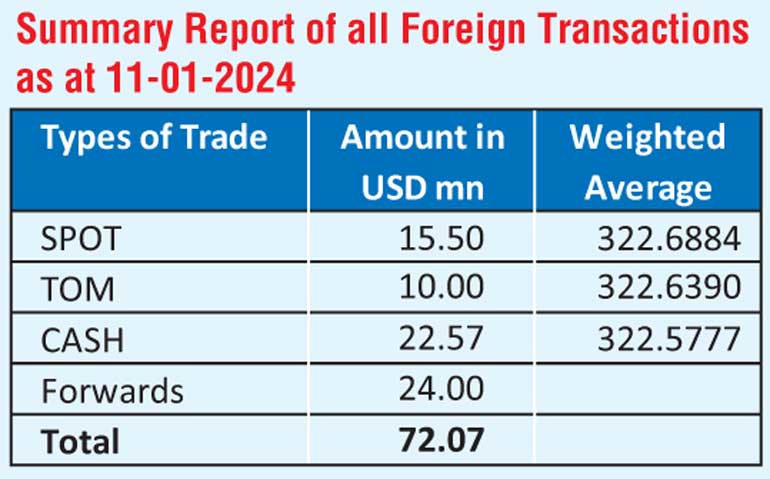

In the forex market, the USD/LKR rate on spot contracts was seen appreciating marginally during the week to close at Rs. 322.10/322.20. This is as against its previous week’s closing level of Rs. 322.45/322.65 and subsequent to trading at a high of Rs. 322.90 and a low of Rs. 322.50.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 53.32 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)