Sunday Jun 07, 2026

Sunday Jun 07, 2026

Monday, 14 June 2021 00:03 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

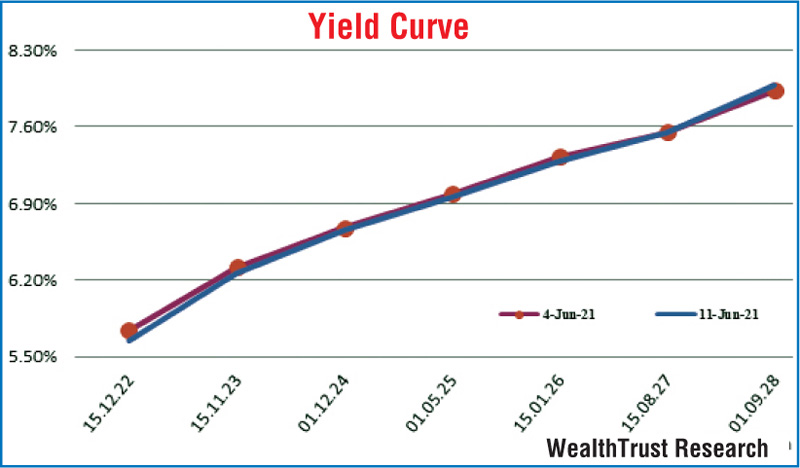

The renewed buying interest along with an improvement to money market liquidity led to secondary market bond yields decreasing during the week ending 11 June, reflecting a marginal downward shift of the yield curve.

The renewed buying interest along with an improvement to money market liquidity led to secondary market bond yields decreasing during the week ending 11 June, reflecting a marginal downward shift of the yield curve.

At the weekly Treasury bill auction, the total accepted volume remained mostly unchanged at 61.91% of its total offered amount while the two Treasury bond auctions conducted on Friday recorded impressive outcomes, as the total offered amount of Rs. 25 billion was successfully accepted at its 1st phase of the auctions. The maturity of 15.01.2026 recorded a weighted average rate of 7.31%, equal to its pre-auction market rate and marginally below its stipulated cut off rate of 7.33% while the 01.05.28 maturity fetched a weighted average rate of 8.02%, below its stipulated cut off rate of 8.05% as well. The bids to offer ratio stood at 2.21:1.

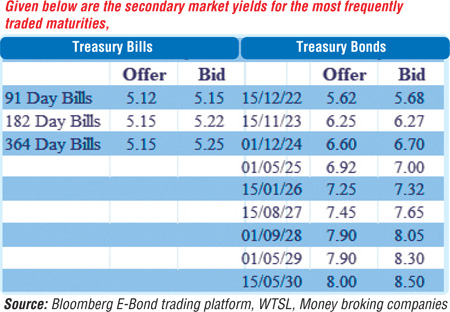

In the secondary bond market, yields on the liquid maturities of 15.12.22 and 15.11.23 were seen decreasing to weekly lows of 5.67% and 6.26%, respectively, against its previous weeks closing levels of 5.70/77 and 6.30/33 while additional 2022’s (i.e. 01.10.22 & 15.11.22) and 2023’s (i.e. 15.01.23, 15.03.23, 15.07.23 and 01.09.23), too, were seen decreasing to lows of 5.65% each, 5.70%, 5.96%, 6.10% and 6.17%, respectively. In addition, maturities of 2024’s (i.e. 15.09.24 & 01.12.24), 01.05.25 and 2026’s (i.e. 15.01.26, 01.02.26 & 01.08.26) were seen changing hands at levels of 6.61%, 6.72%, 7.00% to 7.01%, 7.31% to 7.32%, 7.30% and 7.39% to 7.45%, respectively, as well. In the secondary bill market, August, September and October 2021 maturities were traded within the range of 5.10% to 5.18%.

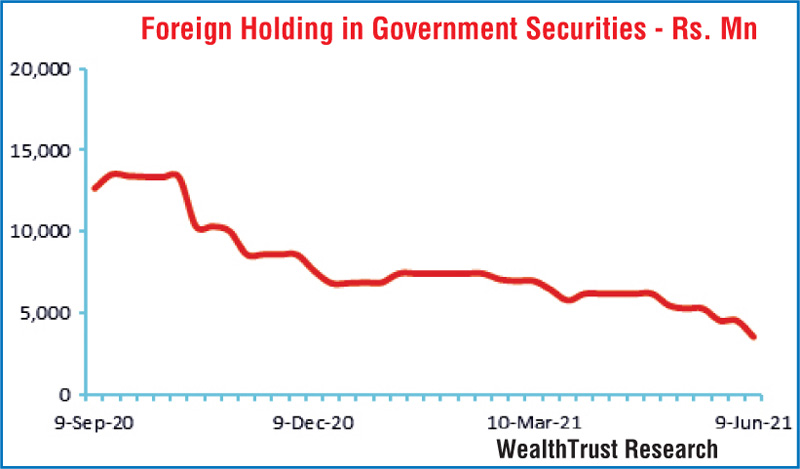

Meanwhile, the foreign holding in rupee bonds decreased with an outflow of Rs. 1 billion for the week ending 9 June while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 6.57 billion.

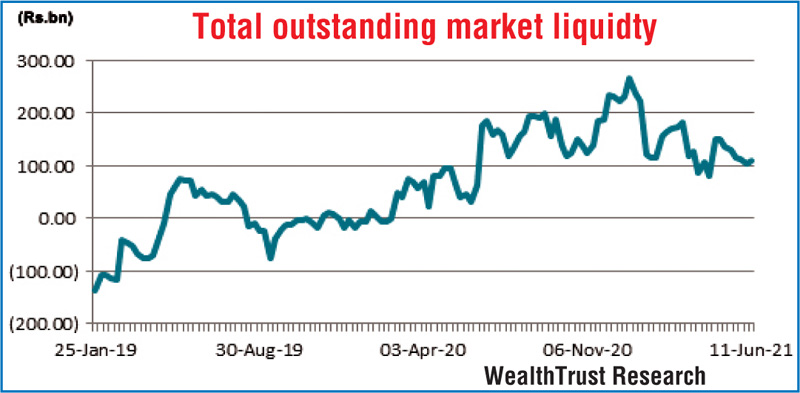

In money markets, the total outstanding liquidity surplus increased to Rs. 110 billion against its previous week’s Rs. 104.80 billion while CBSL’s holding of government securities, too, increased to Rs. 874.34 billion against its previous week’s of Rs. 868.57 billion. The weighted average rates on overnight call money and repo increased marginally to average 4.76% and 4.78%, respectively, for the week.

USD/LKR

The forex market continued to remain inactive during the week. The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 50.49 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, money broking companies)