Thursday Feb 19, 2026

Thursday Feb 19, 2026

Thursday, 14 March 2024 04:34 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

By Wealth Trust Securities

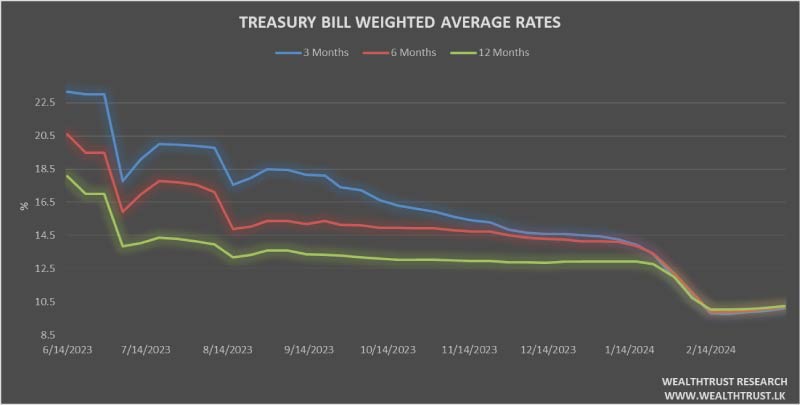

At the weekly Treasury bill auction conducted yesterday, the weighted average yields were seen increasing across all three maturities, for a third consecutive week. The 91-day maturity increased by 14 basis points to 10.10%, the 182-day maturity increased by 13 basis points to 10.21%, while the 364-day maturity also went up by 10 basis points to stand at 10.24%. This was on the heels of the bond auction conducted the day before, which also saw yields move up considerably on the short tenor 15.12.2026 bond.

Accordingly, rates across all three maturities were seen moving above the Central Bank’s Standing Lending Facility Rate of 10.00%, for the first time in 5 weeks. The auction went undersubscribed with 92.94% or Rs. 167.30 billion out of the Rs. 180.00 billion offered raised at the 1st phase of the auction.

The 2nd phase of subscription, across all three maturities will be opened until 4:00 p.m. on the day before the settlement date (i.e., 14.03.2024) at the respective weighted averages determined at the 1st phase of the auction. Given below are the details of the auction;

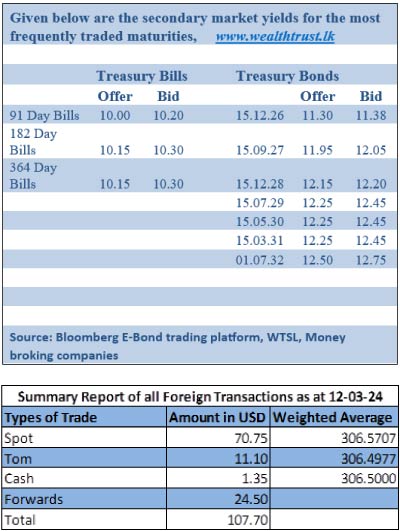

Meanwhile, the secondary bond market yesterday was dull with limited activity and slim volumes transacted. While yields held broadly steady compared to the previous day’s levels, established after the Treasury bond auction. Accordingly limited trades were observed on the maturities of 01.05.24, 01.05.27 and 15.12.28 within the ranges of 10.30% to 10.15%, 11.90% and 12.18% respectively.

In secondary market bills, May 2024 maturities were seen trading within the range of 10.20% on the back of considerable volumes prior to the auction announcement. Similarly, September 2024 maturities were seen changing hands at 10.10% also on the back of substantial volumes. While March 2025 maturities were seen changing hands at levels of 10.15% on the back of considerable volumes prior to the auction announcement.

The total secondary market Treasury bond/bill transacted volume for 12 March was Rs. 36.62 billion. In money markets, the weighted average rates on overnight call money and Repo stood at 9.19% and 9.27% respectively while the net liquidity deficit stood at Rs. 13.20 billion yesterday.

An amount of Rs. 0.99 billion was withdrawn from Central Banks SLFR (Standard Lending Facility Rate) of 10.00% against an amount of Rs. 47.79 billion deposited at Central Banks SDFR (Standard Deposit Facility Rate) of 9.00%. The DOD (Domestic Operations Department) of Central Bank injected liquidity by way of an overnight repo auction for Rs. 60.00 billion at the weighted average rate of 9.17%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts closed the day appreciating to Rs. 306.10/306.20 against its previous day’s closing level of Rs. 306.50/306.60.

The total USD/LKR traded volume for 12 March was

$ 107.70 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)