Sunday Feb 15, 2026

Sunday Feb 15, 2026

Tuesday, 21 September 2021 00:04 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

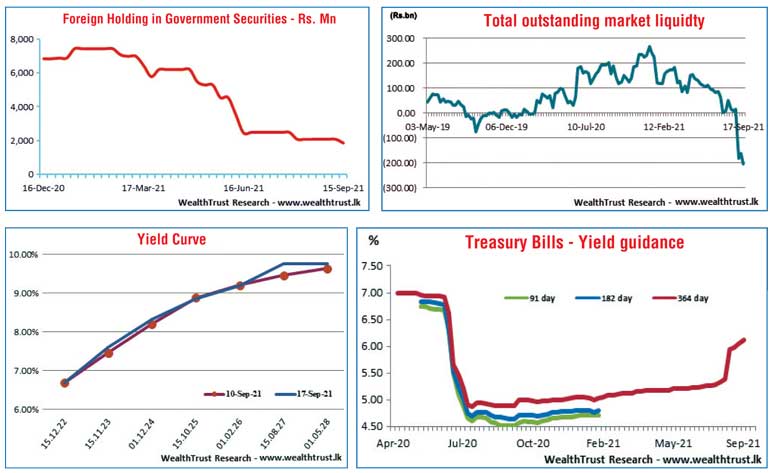

The downward momentum in yields that prevailed in the secondary bond market during the early part of the week reversed towards the later part, as a result of the removal of the yield guidance for the upcoming weekly Treasury bill auction.

At this week’s (22 September) bill auction, a total volume of Rs. 39.5 billion will be on offer, consisting of Rs. 10 billion on the 91 day, Rs. 13 billion on the 182 day and Rs. 16.5 billion on the 364 day maturities.

Last week’s auction went undersubscribed for a ninth consecutive week as only 49.53% was accepted in total while weighted averages increased by seven basis points each on the 91 day and 364 day maturities to 6.08% and 6.12% respectively. The stipulated cut off rate on the 364 day maturity was at 6.12% at last week’s auction.

In the secondary bond market, yields on the liquid maturities of 01.10.22, 15.07.23, 2024s (i.e. 15.09.24 and 01.12.24), 15.01.26, 01.07.28, 15.05.30 and 15.03.31 dipped to weekly lows of 6.25%, 7.00%, 8.00%, 7.98%, 8.90%, 9.50% and 10.00% each respectively while two way quotes on the rest of the yield curve reduced as well.

An increase in the total accepted amount at the T-bond auctions held on 13 September to 83.56% of its total offered amount coupled with the successful outcome of the direct issuance window for the 15.03.2031 maturity were seen as the reasons that led to the positive momentum. Nevertheless, yields were seen increasing once again towards later part of the week to highs of 7.15%, 8.20% and 10.12% on the maturities of 15.07.23, 01.12.24 and 15.05.30 respectively.

The foreign holding in rupee bonds reduced to Rs. 1.86 billion, recording an outflow of Rs. 222 million for the week ending 15 September while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 10.82 billion.

In money markets, the weighted average rates on overnight call money and repo increased further to 5.96% and 5.92% respectively for the week as the net liquidity shortfall at the end of the week increased above Rs. 200 billion to record Rs. 206.60 billion against its previous weeks Rs. 162.78 billion. The CBSL’s holding of Gov. Security’s increased to Rs. 1,330.32 billion against its previous weeks of Rs. 1,290.36 billion.

Rupee trades on spot contracts

In the Forex market, the USD/LKR rate on spot contracts was traded at Rs. 200 during early part of the week while the overall market continued to remain inactive.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 25.76 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, money broking companies)