Saturday Feb 21, 2026

Saturday Feb 21, 2026

Monday, 11 December 2017 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary market bond yield curve, witnessed different movements during the week ending 8 December, as the yields on the shorter to belly end of the curve decreased, and yields on the longer end of the curve remained steady.

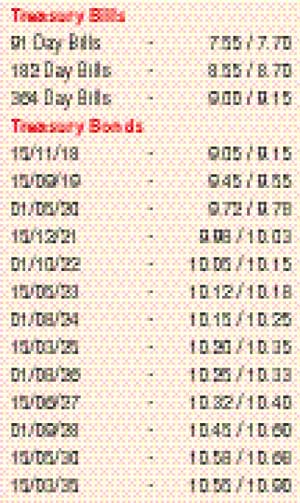

Buying interest witnessed during the latter part of the week resulted in yields of the shorter maturities of 15.11.18, 15.01.19, 01.07.19, 01.05.20, 01.03.21, 01.05.21, 15.12.21 and 15.05.23 decreasing to intraweek lows of 9.13%, 9.35%, 9.42%, 9.75%, 9.95%, 9.98%, 10.00% and 10.13% respectively. The outcome of the weekly Treasury bill auction, as well as the OMO outright bill auctions, contributed to this trend, with the weighted averages reflecting considerable drops.

Furthermore, considerable buying interest was witnessed in the secondary bill market, resulting in yields of the March, May and November 2018 maturities declining to weekly lows of 7.70%, 8.65% and 9.05% respectively. On the longer end of the curve, the 15.06.27 maturity continued to change hands at levels of 10.33% to 10.35% as trading remained dull.

Meanwhile, the foreign holding in Rupee bonds continued to increase, recording a 10 week high inflow of Rs. 11.21 billion for the week ending 6 December 2017 with its total outstanding increasing to Rs. 321.02 billion.

The daily secondary market Treasury bond/bill transacted volume for the first four days of the week averaged Rs. 4.11 billion.

In the money market, overnight call money and repo rates remained mostly unchanged to average at 8.13% and 7.54% respectively, with the average net surplus liquidity in the system standing at Rs. 29.47 billion. The Open Market Operations (OMO) Department was seen draining out liquidity throughout the week on an overnight basis at a weighted average of 7.25%.

Furthermore, it also drained out a further Rs. 20 billion, by way of outright sales of 84 and 91 day Treasury bills and a 7 day repo auction, at weighted average rates of 7.78%, 7.84% and 7.32% respectively. The Central Bank of Sri Lanka’s Treasury bill holding decreased further to a low of Rs. 9.53 billion as at the end of the week.

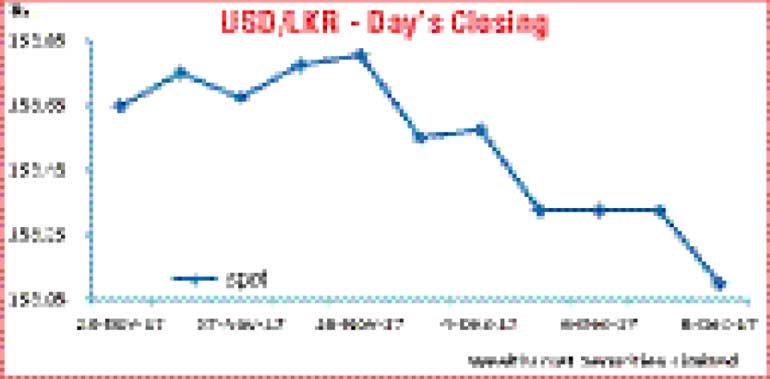

Rupee appreciates during the week

The rupee on spot contracts appreciated considerably during the week to close the week at Rs. 153.00/10 against its previous weeks closing level of Rs. 153.50/60 on the back of export conversions and seasonal inward remittances.

The daily USD/LKR average traded volume for the three days of the week stood at $ 54.88 million.

Some of the forward dollar rates that prevailed in the market were one month – 153.90/05; three months – 155.65/80 and six months – 158.30/50.