Monday Mar 23, 2026

Monday Mar 23, 2026

Wednesday, 9 March 2016 00:00 - - {{hitsCtrl.values.hits}}

In a statement made to Parliament yesterday by Prime Minister Ranil Wickremesinghe, proposals were made to change certain taxes in the backdrop of changing global economic climate and large Government debt repayments. Principal among these changes is the reintroduction of income tax on capital gains, increasing the VAT rate, removing certain exemption on VAT and NBT and thereby widening the tax base. Following is a tax alert prepared by Ernst & Young Sri Lanka last evening:

Executive summary

In a statement made to Parliament today by Prime Minister Ranil Wickremesinghe, proposals were made to change certain taxes in the backdrop of changing global economic climate and large Government debt repayments. Principal among these changes is the reintroduction of income tax on capital gains, increasing the rate of Value Added Tax (VAT), removing certain exemption on VAT and Nation Building Tax (NBT) and thereby widening the tax base.

Whilst some of these proposals are altogether new, the other proposals amend certain proposals of Budget 2016.

Capital Gains Tax

It has been proposed to reintroduce tax on capital gains. Tax on capital gains from sale of shares quoted in the Colombo stock exchange was abolished in 1987 and tax on capital gains arising on other assets were abolished in 2002.

The methodology of taxation of capital gains and the rates of tax under such proposal are yet to be announced.

Capital gain was defined in the past to mean the profits or income arising from any of the following:

a) The change of ownership of any property occurring in any manner whatsoever (sale, exchange, transfer, realisation, etc. of movable or immovable property)

b) The surrender or relinquishment of any right in any property (not include the right of ownership of a property, but include annuities, leases, mortgages. etc.)

c) The transfer of some of the rights in any property (It is possible that only some rights are surrendered keeping other rights)

d) The redemption of any share, debenture or other obligation

e) The formation of a company (the profits of the person promoting a company will be treated as capital gains)

f) The dissolution of a business or the liquidation of a company (applicable to the shareholders and not to the company)

g) The amalgamation or merger of two or more businesses or companies

h) Any transaction in connection with the promotion of which any person who is not a party to such transaction receives a commission or reward.

However, any profits or income falling under any other sources enumerated under section 3 of the Inland Revenue Act, in particular, (i) trade, business, profession or vocation, (ii) rents, royalties or premiums, (iii) income from any other source not including profits of a casual and non-recurring nature, do not fall within the meaning of capital gain.

Capital gains are calculated on the basis of realised increases in value at the time the gain is in fact realiSed. Therefore, capital gains do not accrue but arise on a particular date i.e., the date of realisation. As the actual gain accruing over the whole period of ownership is taxed as income of one year, relief has been provided by fixing a lower maximum rate.

In the computation of capital gains certain expenses, such as lawyers’ fees, brokers’ fees or stamp duties involved were generally deductible, depending on situation and circumstances. Any capital loss could be set off against capital gains.

The value, with reference to any property or consideration in the context of the definition of “capital gain” was defined having taken into account the length of ownership of the property. Certain gains, such as from the sale of first house, were exempted and in the case of capital gains that arose (from the change of ownership of a property), tax rates varied based on the period of ownership (for instance, no tax was payable if the period of ownership was not less than 25 years, and if the period of ownership was between 25 – 20 years, the tax rate was 5%).

Corporate income tax rates

In the Budget presented in Parliament in November 2015 it was proposed to introduce a two band income tax rate of 15% and 30 %.Thus, it was proposed that banking and financial services, insurance and whole sale, retail trade will be liable to income tax at the rate of 30% whilst all other sectors such as manufacturing, agriculture, SME and all other services will be liable to income tax at the rate of 15%.

However, according to the proposals read out today by the Hon. Prime Minister corporate income tax rates will be as follows:

a) Tourism, construction, agriculture, exports and SME which were earlier liable at 10% and 12% will increase to 17.5 %.

b) Liquor and tobacco will be at 40%

c) All other sectors will remain at 28%.

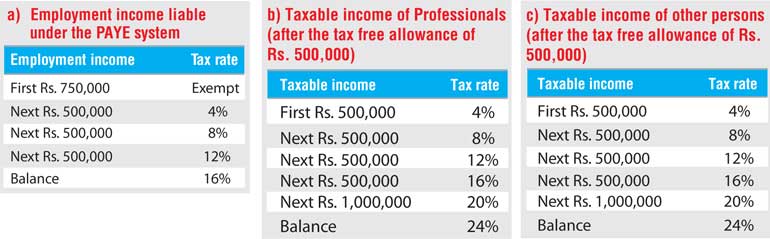

Personal income tax

The proposal as announced in the Budget speech in November 2015 to exempt from income tax individuals income up to Rs. 2.4 million per annum and to tax income above the exempt limit at a flat rate of 15% will not be implemented. Instead, the current rates of income tax will prevail, as follows.

a) Employment income liable under the PAYE system (table a)

b) Taxable income of Professionals (after the tax free allowance of Rs. 500,000) (table b)

c) Taxable income of other persons (after the tax free allowance of Rs. 500,000) (table c)

Further, it is expected that withholding tax on interest income on fixed deposits will continue to be liable at the rate of 2.5% as a final tax.

VAT

The proposal in the 2016 Budget to introduce a two band rate of 8% and 12.5 % will not be implemented. Instead the VAT rate will be increased to 15%. The following exemptions currently available will be removed.

a) Telecommunication services

b) Private education

c) Private health care

In respect of telecommunication services it is expected that the 15% VAT rate will be imposed in addition to the Telecommunication Levy of 25% paid currently.

It has also been proposed to impose VAT on retail and wholesale sector excluding essential items which are currently not liable to VAT. Currently retail and wholesale sector is liable to VAT only where the annual turnover exceeds Rs. 400 million. It is expected that the current threshold will be reduced to a lower level in order to attract a larger segment of wholesale and retail sector to VAT except on certain essential items.

NBT

The increase of NBT rate to 4% in the 2016 Budget will not be implemented and therefore the current rate of 2% will continue. However, the following exemptions will be removed.

a) Electricity

b) Lubricants

c) Telecommunication services

Threshold for NBT will be reduced to Rs. 3 million from Rs. 3.75 million per quarter.

Effective date

At this point of time it is not certain as to when the above proposals will be given legal effect. It is expected however that all of the above proposals will be implemented from 1 April 2016 and the necessary legislation will be presented subsequently to bring legal effect to the above proposals.

It is to be noted that since no reference has been made to other tax proposals in Budget 2016, such proposals will be implemented as proposed. These include the following:

a) Abolishing of Share Transaction Levy, Construction Industry Guarantee Fund Levy, Land Lease Tax, Tourism Development Levy and Stamp Duty on transfer of shares

b) Amendments to Economic Service Charge (ESC)