Monday Jul 06, 2026

Monday Jul 06, 2026

Tuesday, 15 August 2017 00:00 - - {{hitsCtrl.values.hits}}

The grace of God, perseverance and hard work for the past three decades are the three key attributes for the newest Chairman of the Colombo Stock Exchange (CSE), Ray Abeywardena, who created capital market history by becoming the first career broker to ascend to the top seat of the Bourse.

The humble yet assertive Ray however admits he didn’t envision to be the Chairman of the Colombo Bourse when he started his career in 1986, a year after the present CSE was established. Though the 10 previous chairmen weren’t career brokers, they were corporate leaders, and Ray says all of them had been inspirational for him during his career.

“In the early years and up until 1980s, the broking industry structure and systems in the established broking firms was very hierarchical. The power distance between us and our bosses was vast. In the early days aspiring to be a director would have been a great achievement, leave alone becoming a director of the Stock Exchange or its chairman,” recalls Ray. In that context he adds: “I consider it as an honour to be able to serve as Chairman of CSE in an industry that nurtured me and provided everything in a career sense for 30 years.”

Share trading in Sri Lanka began 121 years ago under the Colombo Share Brokers Association (CSBA), which in 1904 was renamed Colombo Brokers Association (CBA). In 1984, the country saw the establishment of a Public Trading Floor and inauguration of trading on the “open outcry system” by the Colombo Brokers Association. A year later Colombo saw the commencement of a second trading floor by the Stock Brokers Association, leading to the amalgamation of the Colombo Brokers Association and the Stock Brokers Association trading floors to constitute the Colombo Securities Exchange (GTE) Ltd.

Recalling that in the 1980s when he started, a Rs. 1 million brokerage was applauded, Ray says since then the stock market has gone through many cycles and development phases to become what it is today.

In this interview with the Daily FT, Ray traces various developments of Sri Lanka’s capital market, the challenges faced and those ahead as well as plans and recommendations towards ensuring a robust stock market. During his tenure as Chairman Ray is keen for the industry to remember him as “a doer in getting the right things done and doing the right thing. Someone who walked the talk in terms of implementation and results.”

Following are excerpts:

By Nisthar Cassim

Q: What are the key traits to be a successful professional in the capital market?

A: Unquestionable honesty and integrity to build trust and acceptance by all stakeholders are the most important factors to be successful in the capital markets industry.

Q: What is your assessment of the status of the capital market?

A: Whilst other markets in and around us have grown considerably, the Colombo stock market has had many ups and downs. During 1986-1990 the market was severely constrained due to the 100% tax on foreigners and in 1990 when R. Premadasa was the President it was removed. In my opinion it was one of the boldest moves in capital markets after the privatisation of State-Owned Enterprises. The early promise in the 1990s following these moves, with the entry of foreign brokerage firms and quality of research improving, didn’t materialise because of the escalation of the war and the latter’s impact on the economy. By year 2000, the market and economy were in a perilous state. In early 2000 stability returned and post-war the market took off to become Asia’s best performing and second best in the world.

Having said that, Colombo hasn’t effectively grown as we have remained a homogeneous single equity market. We have not brought in other products such as derivatives, stock borrowing and lending, margining, and short selling, or introduced platforms such as Delivery Versus Payment (DVP) or Central Counter Party, via which could have enabled the entry of new investment products.

DVP is very important to give an assurance of settlement and is a best practice followed in most markets and it will attract foreign investors to invest in our market without fear of settlement failure, whilst CCP will further boosts confidence and credibility in addition to diversify investment opportunities. We desperately need to get DVP and CCP on board as we are already behind our competitors in this aspect. We will launch DVP by mid next year.

Q: Despite challenges such as the 30-year war and policy inconsistency such as a stop to privatisations, the market still progressed?

A: Yes, our market has been very resilient, plus CSE progressed in automation. We were one of the first exchanges from this part of the world to have a Central Depository System in the early 1990s even before India and we were far ahead of the others in introducing automated trading in 1997. However, the other exchanges that went digital thereafter have overtaken us in terms of size, products, and significance in the global arena.

A perennial challenge has been the low or poor liquidity for which Government policy in listing SOEs partially is required. In the past, starting from the listing of United Motors in 1990s when the current Speaker of Parliament Karu Jayasuriya was the Chairman, we had several SOEs listed such as Lanka Milk Foods, Distilleries, Plantation Companies, Kelani Tyres, Sri Lanka Telecom, etc. We need to bring SOEs such as State-owned banks, SriLankan Airlines, Petroleum – even listing a 10% stake if larger stakes are not politically advisable. Token listing of 10% alone will boost market capitalisation phenomenally, which will make the CSE large enough to get higher interest from foreign investors and also enter into the Morgan Stanley Capital International (MSCI) Emerging Market Index, which is widely followed by funds in asset allocation. On the other hand, main drivers of the economy such as larger apparel export firms are not listed. The market does not mirror the key drivers of the economy.

Q: So if the private sector is risk averse to list on the CSE or harness benefits of being listed such as access to low or zero cost capital, how can we expect the Government to be savvy in terms of listing SOEs?

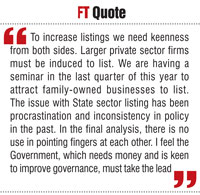

A: Yes, agreed. We need keenness from both sides. Larger private sector firms must be induced to list. We are having a seminar in the last quarter of this year to attract family-owned businesses to list. The issue with State sector listing has been procrastination and inconsistency in policy in the past. In the final analysis, there is no use in pointing fingers at each other. I feel the Government, which needs money and is keen to improve governance, must take the lead.

Q: What will be your immediate priorities as Chairman?

A: In terms of market-centric short-term objectives, firstly increase market turnover. Compared to other frontier and emerging markets, Colombo turnover is very low. There is considerable scope for improvement. The other priority is to help improve profitability of the capital market industry. This will enable more market development as well as investment in quality research by brokers. Third is get the support of all stakeholders to increase listing and liquidity. Simultaneously we will expedite efforts to implement DVP and CCP.

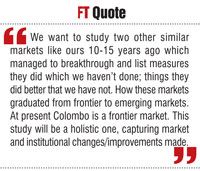

We want to study two other similar markets like ours 10-15 years ago which managed to break through and list measures they did which we haven’t done; things they did better that we have not. How these markets graduated from frontier to emerging markets. At present Colombo is a frontier market. This study will be a holistic one, capturing market and institutional changes/improvements made.

We have made significant progress for the introduction of a ‘Dollar Board’ which will enable dual listings from South Asia. This will offer a common South Asian investment opportunity in Colombo. This will also complement the Government’s broader plans to make Colombo a financial centre in the region. We hope to have this feature on board before the end of the year.

As Chairman I must say that the Board of Directors is fully committed to support the CEO and senior management in their quest to make the CSE a vibrant market that will attract investors.

Q: Why is CCP implementation taking longer and who will handle it?

A: Initially an MOU between CSE, SEC and Central Bank was signed to implement CCP. With the change of Government, the Central Bank opted out so CSE and SEC are jointly working towards implementing CCP. It will be implemented in phases after DVP.

Q: What is the progress of demutualisation? This too has been discussed for a very long time.

A: The Government and the SEC is very keen and the CSE is also supporting the move in discussion with member firms. This means CSE will be eventually listed. The SEC Act has to be amended as well for demutualisation apart from a Demutualisation Act which will spell out the methodology.

Q: How will you improve the ease of listing?

A: It is the obligation of the CSE to encourage listing as well as increase market liquidity and we are very focused on that. We are in consultation with the SEC to improve the ease of listing and fund raising.

Q: There have been issues over capital adequacy of brokers?

A: We are looking at bringing financial stability and strength to the broking firms. We have introduced Capital Adequacy Ratio (CAR) where the volume of business one does daily will be correlated to the strength of capital, which is practiced globally. Regardless of bull or bear runs, this is important. This is a decision in the right direction.

Q: Given the current market conditions, there have been calls for broker consolidation. Your views?

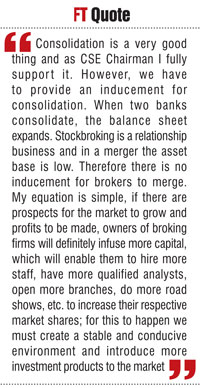

A: Consolidation is a very good thing and as CSE Chairman I fully support it. However, we have to provide an inducement for consolidation. When two banks consolidate, the balance sheet expands. However stockbroking is a relationship business and in a merger the asset base is low. Therefore there is no inducement for brokers to merge. For a larger broker to buy a small broker along with liabilities, there must be inducement. Considering the market and industry challenges, we have also proposed to the SEC to consider for a limited period a freezing of licences of certain brokers who may be facing financial difficulties. This will enable brokers to stay their business for a defined period to be determined by SEC and CSE. Businesses may not be keen to shut down immediately. However, I hope the market activity will continue to improve to sustain business of brokers.

This year, to date we have experienced Rs. 26.1 billion in net foreign buying and the market has been positive after being negative for two years. If this momentum continues and strengthens, broking firms will not want to close shop but look at ways of infusing capital. For shareholders and owners of broking firms, it is a business decision. Usually the tendency is not to put good money when the business is not doing well. If one sees potential to grow, then fresh capital will follow.

My equation is simple, if there are prospects for the market to grow and profits to be made, owners of broking firms will definitely infuse more capital, which will enable them to hire more staff, have more qualified analysts, open more branches, do more road shows, etc. to increase their respective market shares; for this to happen we must create a stable and conducive environment and introduce more investment products to the market.

Q: Is this freeze of license for a predetermined period a means for member firms to survive until demutualisation, at which point there could be opportunities to cash in?

A: Not necessarily, but there may be member firms which are entitled to a share of demutualised stock exchange who may opt to sell-out/exit. But out of 27, only 15 are members and 12 are not. So the interests of these 12 trading members must be considered as well when times are challenging. The proposal to SEC for a freezing period was out of consensus of all members. Support mechanisms when industries are in difficulty is not new and capital markets isn’t alone in this; many other industries in the past have benefitted from incentives or subtle support such as tourism, tea, etc., when the going has been tough. We are not asking for cash or incentives but regulatory support to temporarily suspend the business without losing the license.

Q: How is the industry faring in terms of confidence, credibility and trust? Has confidence returned after some negative developments and alleged pump and dump and other irregularities?

A: Both the SEC and CSE are continuously addressing this issue of building trust, confidence and credibility and investor as well as issuer interests collectively and within respective purviews. In recent times there haven’t been any controversies, which means stability, trust and confidence are returning to the market.

Q: Where do you want the Colombo stock market to be in the medium term?

A: I want to see market turnover improving to Rs. 2 billion per day and market capitalisation increasing to 30-35% of GDP from the current 20% levels. Towards achieving these goals, focus is to expedite the implementation of decisions already made and carry out some of the new measures I highlighted earlier on in the interview.

Q: Is the capital market industry duly recognised nationally?

A: In most countries the stock market is the barometer of the economy. We need all stakeholder inputs to make the stock market dynamic and vibrant, the same way policies, programs and effort are put in for national and economic development. We need to have a very focused and concerted effort by all stakeholders including the Government to make the stock market robust. This is the need of the hour. In a critical sense Sri Lanka’s stock market has been stunted due to a multitude of issues and we need to break out of this status, reach the next level of growth, and be very progressive.

My sincere request is that a high-powered Government ‘doer tank’ is appointed as soon as possible headed by a capable Government official that will include representatives from the SEC, the CSE, broking firms, the unit trust industry, fund management firms and all key stakeholders who will formulate and implement a series of initiatives to make the market vibrant and feasible. We need a joint ‘action plan’ to make this market move to where it ought to be. A vibrant market is a feather in the cap of any government, as strong foreign inflows and the ability to raise capital are key support factors to an economy.

Q: How would you like the industry to remember you during your tenure as Chairman?

A: As a doer in getting the right things done and doing the right thing; someone who walked the talk in terms of implementation and results.