Sunday Feb 15, 2026

Sunday Feb 15, 2026

Wednesday, 19 July 2017 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

By Wealth Trust Securities

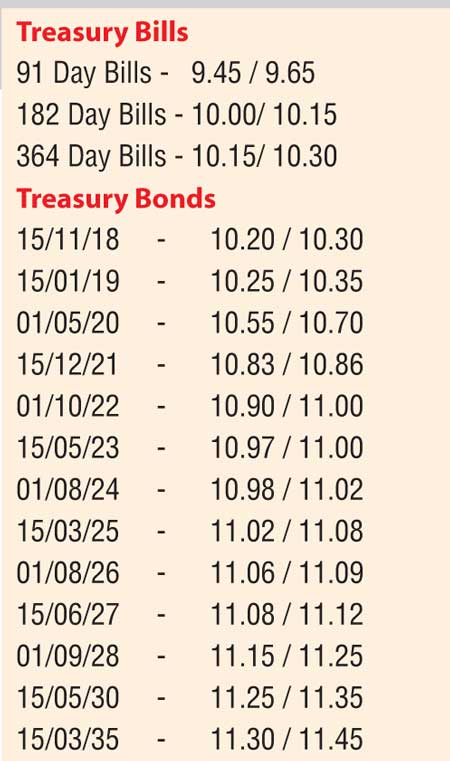

The completion of the second review of the Extended Fund Facility (EFF) arrangement and approval for the disbursement of $ 167.2 Million resulted in the decline of yields in the secondary bond market.

This was ahead of the weekly Treasury bill auction due today. Activity centred on the liquid maturities of 15.12.21, 15.05.23, 01.08.24, 01.08.26 and 15.06.27 with their yields dipping to intraday lows of 10.85%, 11.00% each, 11.06% and 11.10% respectively, when compared against its previous day’s closing levels of 10.98/01, 11.10/12, 11.10/15, 11.18/22 and 11.23/26.

Furthermore, a limited amount of trades took place on the 15.05.30 maturity within the range of 11.30% to 11.40% as well.

At today’s T bill auction, a total amount of Rs. 24.5 billion will be on offer, consisting of Rs. 3 billion, Rs. 12.5 billion and Rs. 9 billion of the 91, 182 and 364 day maturities. At last week’s auction, the weighted average yields of the 182 day and 364 day maturities declined for a second consecutive week to 10.23% and 10.39% respectively while the weighted average yield of the 91 day remained steady at 9.60%.

The total secondary market Treasury bond transacted volume for 17 July 2017 was Rs. 8.7 billion.

In money markets, the Open Market Operations (OMO) Department of the Central Bank of Sri Lanka drained out an amount of Rs. 18.68 billion on an overnight basis at a weighted average of 7.32% by way of a repo auction, as net surplus liquidity in the system increased to Rs. 21.93 billion yesterday. The overnight call money and repo rates averaged 8.75% and 8.82% respectively.

Meanwhile, in the Forex market, the USD/LKR rate on spot contracts dipped marginally to Rs. 153.78/85 on the back of importer demand, in comparison to the previous day’s closing level of Rs. 153.70/78.

The total USD/LKR traded volume for 17 July 2017 was $ 29.85 million.

Some of the forward USD/LKR rates that prevailed in the market were one month - 154.80/90; three months - 156.75/85 and six months - 159.80/90.

Given below are the closing secondary market yields of the most frequently traded T-bills and bonds.