Sunday Feb 22, 2026

Sunday Feb 22, 2026

Wednesday, 23 November 2016 00:13 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

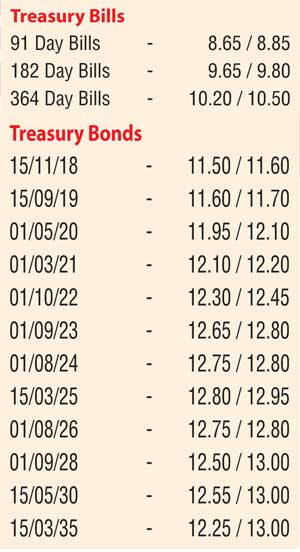

Short tenure Treasury bond yields were seen increasing yesterday ahead of today’s weekly Treasury bills auction on the back of continued foreign selling interest. Yields on the 2018’s (i.e. 01.06.18 and 15.11.18) and the 2019 were seen hitting intraday highs of 11.50% each and 11.70% respectively against its previous day’s closing levels of 11.40/50 and 11.50/70.

In addition, activity was witnessed on the 01.05.20, 01.03.21, 01.10.22, 01.09.23, and 01.08.24 at levels of 12.00%, 12.10% to 12.25%, 12.35% to 12.36%, 12.64% to 12.75% and 12.70% to 12.80% respectively.

A total amount of Rs. 31.5 billion will be on offer at today’s weekly auction in comparison to its previous week’s total offered amount of Rs. 29.50 billion, consisting of Rs. 8.5 billion on the 91 day maturity, Rs. 13 billion on the 182-day maturity and a further Rs. 10 billion on the 364 day maturity. At last week’s auction, weighted averages on the 182 day and 364 day maturities increased by 9 and 6 basis points respectively to 9.65% and 10.20% while the 91 day maturity remained steady at 8.60% as the total accepted amount dipped close to a 12 year low of 1.01 billion.

In money markets, the overnight call money and repo rates remained mostly unchanged to average 8.44% and 8.63% respectively as the Open Market Operations (OMO) department of Central Bank injected an amount of Rs.10.00 billion on an overnight basis by way of a Reverse Repo auction at a W. Avg of 8.50%.

The net deficit in the market stood at Rs. 39.25 billion with a further amount of Rs. 32 billion been accessed from the Standing Leading Facility Rate of 8.50% against a deposit of Rs. 3.62 billion at the Standing Deposit facility Rate of 7.00%. Meanwhile, the OMO department of Central Bank was seen injecting in total an amount of Rs. 2.20 billion by way of two outright purchases of Treasury bills at weighted average rates of 8.65% and 9.05% for 65 and 72 days respectively, valued today.

Rupee dips marginally

Meanwhile, in Forex markets yesterday, the USD/LKR rate on spot next contracts depreciated marginally to close the day at Rs. 148.70/75 against its previous day’s closing levels of Rs. 148.55/65 on the back of foreign selling in Rupee bonds and importer demand. The total USD/LKR traded volume for 21 November 2016 was $ 44.13 million.

Some of the forward USD/LKR rates that prevailed in the market were one month - 149.50/60; three months - 151.40/50 and six months - 153.90/00.