Friday Feb 20, 2026

Friday Feb 20, 2026

Monday, 9 May 2016 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

By Wealth Trust Securities

The week ending 6 May saw secondary market bond yields see saw, decreasing during the early part of the week and increasing once again towards the latter part of the week on the back of considerable volumes changing hands.

Foreign and local buying interest across the yield curve, covering maturities of 01.05.2020, 01.10.2022, 15.03.2025, 01.06.2026, 01.09.2028 and 15.05.2030 saw its yields dip to weekly lows of 11.35%, 11.55%, 11.70%, 11.75%, 12.00% and 12.01% respectively while selling interest following the weekly Treasury bill auction and the announcement of four Treasury bond auctions saw its yields edge up to its weekly highs of 11.47%, 11.67%, 11.80%, 11.95%, 12.12% and 12.25% once again. In addition, on the very short end of the curve, 2018 and 2019 maturities were seen changing hands within the range of 11.00% to 11.15% and 11.25% to 11.30% as well during the week.

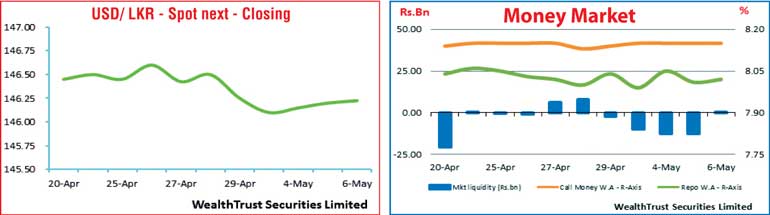

Meanwhile in money markets, the overnight call money and repo rates remained mostly unchanged to average at 8.15% and 8.02% for the week as the Open Market Operations (OMO) department of Central bank injected liquidity during the week on an overnight basis at weighted averages ranging from 7.92% to 7.97%.

Rupee remains mostly unchanged

The USD/LKR rate on the active spot next contract remained mostly unchanged to close the week at Rs. 146.15/25. The daily USD/LKR average traded volume for the first three trading days of the week stood at $ 47.09 million.

Some of the forward dollar rates that prevailed in the market were one month – 146.90/10; three months – 148.70/10 and six months – 151.00/20.