Monday Feb 16, 2026

Monday Feb 16, 2026

Monday, 10 October 2016 00:01 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

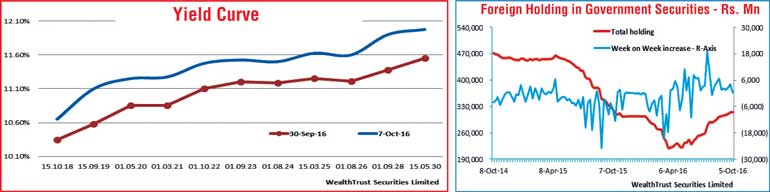

The secondary market bond yields increased across the board during the week ending 7 October, reversing a downward trend witnessed over the previous two weeks on the back of uncertainties creeping into markets.

Yields on the liquid maturities of 15.09.19, 01.10.22, 01.08.24, 01.08.25 and 01.08.26 were seen increasing week on week by 58, 50, 56, 50 and 49 basis points respectively to intra week highs of 11.15%, 11.60%, 11.75% each and 11.70%. In addition, on the long end of the yield curve the 15.05.2030 maturity increased to a high of 12.05% as two way quotes on the rest of the yield curve edged up as well reflecting to a parallel shift upwards week on week.

The slowdown in foreign purchases of Rupee bonds to a nine week low of Rs. 581 million coupled with the weekly bill auction weighted averages holding steady following two weeks of declines contributed to bond yields increasing as well. However, buying interest at these levels curtailed any further upward movement as activity moderated considerably.

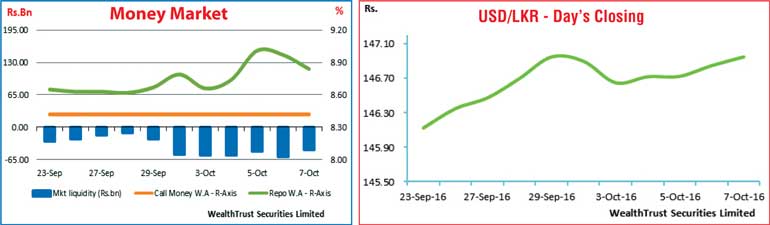

In money markets, the overnight Repo rate increased once again during the week to average 8.84% against its previous week’s average of 8.67% as the net liquidity shortfall in the system increased to Rs. 53.15 billion in average against its previous week’s net shortfall average of Rs. 25.23 billion. However, the overnight call money rate remained stagnant at 8.42% throughout the week. The Open Market Operations (OMO) Department of the Central Bank of Sri Lanka continued to infuse liquidity by way of overnight Reverse repo auctions at weighted average of 8.49%.

Rupee depreciates for a fourth consecutive week

The rupee lost ground marginally for a fourth consecutive week as spot contracts closed the week at Rs. 146.90/00 against its previous weeks closing levels of Rs. 146.85/95 on the back of importer demand and a slowdown in export conversion and foreign buying in Rupee bonds. The active one week and spot next contracts closed at Rs. 147.20/35 and Rs. 147.00/10 respectively as well. The daily USD/LKR average traded volume for the first four days of the week stood at $ 68.07 million.

Some of the forward dollar rates that prevailed in the market were one month – 147.85/95; three months – 149.45/55 and six months – 151.90/00.