Saturday Aug 01, 2026

Saturday Aug 01, 2026

Tuesday, 11 April 2017 00:08 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

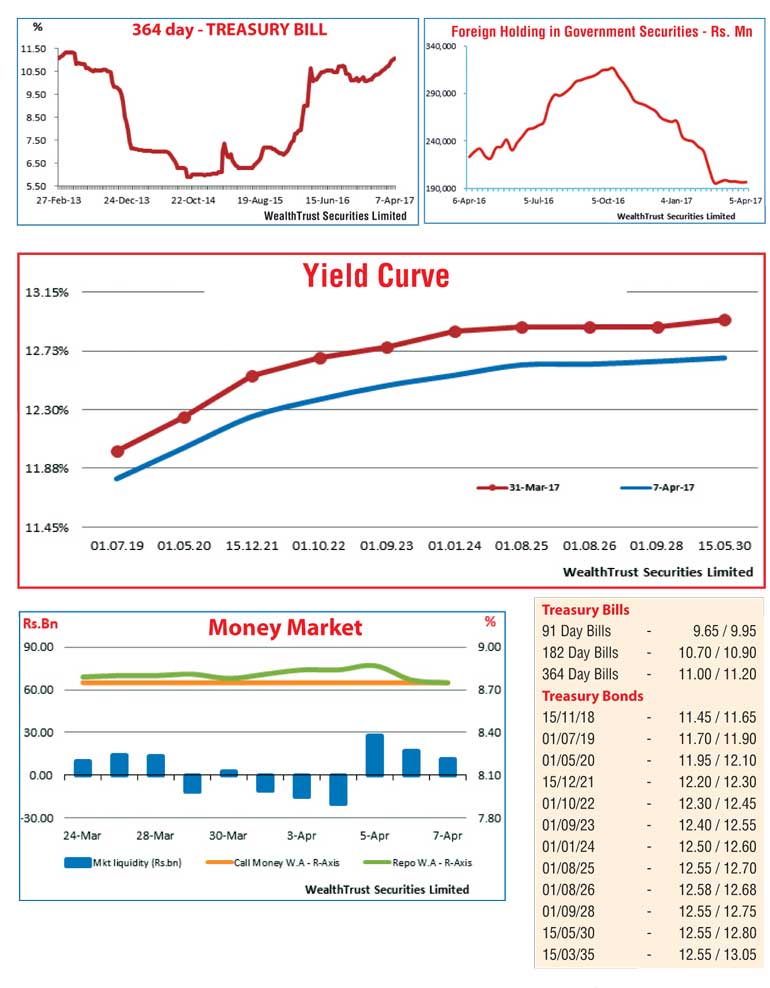

Continues positive sentiment in the bond market, backed by both local and foreign buying resulted in a decline in yields during the week ending 7 April, reflecting a downward shift of the overall yield curve.

This decline in rates was further supported by the outcome of the primary Treasury bond auction where the weighted averages of the 4.08 year maturity of 15.12.2021 dipped by 29 basis points to 12.60% and the 6.09 year maturity of 01.01.2024 recording a yield of 12.92% against the 13.14% recorded on the 01.08.24 maturity previously.

This led to a considerably active secondary market, where yields of the liquid maturities of 15.12.21 and the two 2024’s (i.e. 01.01.24 and 01.08.24) hit weekly lows of 12.17%, 12.50% and 12.52% respectively against its previous weeks closing levels of 12.50/60, 12.80/95 and 12.83/90.

Buying interest was also witnessed of the 01.05.20, 01.05.21 and 01.08.26 maturities with trades taking place at lows of 11.92%, 12.23% and 12.55% respectively.

Meanwhile, foreign buying of Sri Lankan bonds was witnessed during the week ending 05th April with an inflow of Rs.259 million.

However, the upward momentum in rates at the primary Treasury bill auctions was witnessed at Wednesday’s (5) auction as well, where the weighted average yields increased across the boards, with the 364 day bill surpassing the 11.00% psychological level for the first time since 8 May 2013.

This trend continued at the auction held on Friday (7) in lieu of the upcoming short week, where the 91 day, 182 day and 364 day bill maturities increased by 05, 08 and 07 basis points respectively to 9.72%, 10.77% and 11.09%. The total accepted amount of all three maturities stood at Rs.23.09 billion against the total offered amount of Rs.23.00 billion.The daily secondary market Treasury bond transacted volumes for the first four days of the week averaged Rs. 7.73 billion.

In money markets, liquidity was seen increasing towards the latter part of the week as the OMO Department of the Central Bank of Sri Lanka was seen conducting overnight Repo auctions in order to drain out liquidity at a weighted average ranging from 7.65% to 7.71% against overnight Reverse repo auctions conducted during the early part of the week at 8.74%. The overnight call money and repo rates averaged 8.75% and 8.81% respectively.

Rupee losses

The USD/LKR rate on two week forward contracts were seen deprecating mainly towards the later part of the week to close the week at levels of Rs.153.00/10 against its previous weeks closing levels of Rs.152.40/55, while the spot next contracts which become active during the week were seen closing the week at levels of Rs.152.65/80 against its opening levels of Rs.151.96/00.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 67.21 million. Given are some forward dollar rates that prevailed in the market: one month – 153.60/80; three months – 155.30/60; six months – 158.90/00.