Sunday Feb 22, 2026

Sunday Feb 22, 2026

Wednesday, 2 September 2020 00:28 - - {{hitsCtrl.values.hits}}

India’s economy shrank by nearly a quarter in April-June, much more than forecast and pointing to a longer than previously expected recovery with analysts calling for further stimulus.

India’s economy shrank by nearly a quarter in April-June, much more than forecast and pointing to a longer than previously expected recovery with analysts calling for further stimulus.

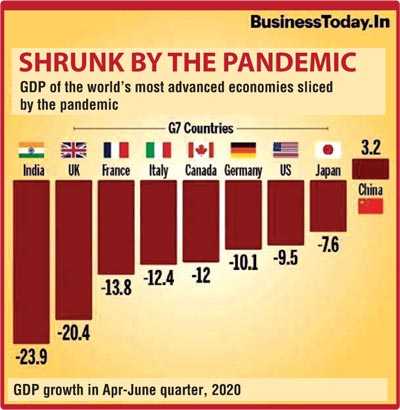

The latest data show that the industry and services sectors shrank 38.1% and 20.6%, respectively. The silver lining was provided by the farm sector, which grew 3.4% during first three months. But agriculture’s share in GDP (Gross Domestic Product) is just 17%, while services and industry account for 54% and 29%, respectively.

According to the data, manufacturing and construction are in deep recession, which means job creation will be affected further.

Consumer spending, private investments and exports all collapsed during the world’s strictest lockdown imposed in late March to combat the COVID-19 pandemic and India – the world’s fastest-growing large economy until a few years ago – now looks to be headed for its first full-year contraction since 1980.

Gross domestic product shrank by a record 23.9% in April-June from a year earlier, official data showed on Monday, against a Reuters poll forecast for an 18.3% contraction.

Krishnamurthy Subramanian, chief economist at the Ministry of Finance, said India’s economy was set for a “V-shaped” recovery and should perform better in the coming quarters as indicated by a pickup in rail freight, power consumption and tax collections.

Some private economists, however, said the fiscal year that began in April could see a contraction of nearly 10%, the worst performance since India won independence from British colonial rule in 1947, and likely to push millions more into poverty.

Consumer spending – the main driver of the economy – dropped 31.2% year-on-year in April-June compared to a 2.6% fall in the previous quarter, data showed, while capital investments were down 47.9% compared to a 2.1% rise in the previous quarter.

Prime Minister Narendra Modi announced a $ 266 billion stimulus package in May, including credit guarantees on bank loans and free food grains for poor people, but consumer demand and manufacturing have yet to recover.

The Reserve Bank of India, which has reduced the benchmark repo rate INREPO=ECI by a total of 115 basis points since February, is expected to cut interest rates to boost growth after keeping them on hold this month amid rising inflation.

The coronavirus has been spreading in India faster than anywhere else in the world, with more than 3.6 million people already infected and a death toll of over 64,400.

Continuing restrictions on transport, educational institutions and restaurants have hit manufacturing, services and retail sales, while keeping millions of workers out of jobs.

Manufacturing has already entered recession as output fell 39.3% in April-June after falling 1.4% in the previous quarter, and construction and trade services plunged by around 50%.

With an annual growth of 3.4% in the April-June quarter, the farm sector, which accounts for 15% of economic output, offered some hope the rural economy will be able to support millions of migrant workers who have returned to their villages.